Editor’s note:

Since 2007, the amount of assets in IRA accounts has exceeded the amount of assets in 401(k) plans. IRA accounts now hold $6.6 trillion of the $23 trillion in retirement assets in the U.S as of first quarter 2014. This trend will continue as boomers retire and move their employer-sponsored retirement savings into rollover IRAs. That being said, the need and urgency for retirement professionals to have an in-depth understanding of these rules has never been greater.

The following transcript of a recent live professional development webinar provides tremendously practical tips for advisors and their clients to help navigate traditional IRA distributions. This presentation was delivered in live webinar format in 2014. Denise’s comments have been edited for clarity and length.

You can view brief YouTube clips of the original presentation here.

You may also choose to take the full length course and earn 1 CRC®, CFP®, ASPPA, and/or American College CE credit.

By Denise Appleby, CISP, CRC®, CRPS, CRSP, APA, President of Appleby Retirement Consulting, Inc.

We’re going to be looking at traditional IRA distributions at a very high level, and we’ll talk about Roth IRA distributions as well. I thought this would be an important topic to address because I’ve been receiving so many questions from my clients about the IRA distributions, in particular, when distributions are taxable, and when penalties apply.

I find that taxpayers are usually surprised when they get a tax bill from the IRS for a penalty that they didn’t think about, to the extent that some of you have challenged the IRS and taken the IRS to court. Of course, they usually lose because they’re required to include these amounts in income, and sometimes they overlook taxes and penalties that apply.

For instance, are there instances when distributions are in fact not taxable? If so, how do you work with your clients to make sure that they do not pay income tax on those distributions that should be tax free? We’re also going to be looking at the required minimum distributions briefly, when the 10 percent early distribution penalty applies, and some of the tax-withholding rules and tax-withholding requirements that apply.

An Overview of Distributions from IRAs

Now generally, when distributions are taken from IRA, they can be done at any time. Up until age 70½, an individual can take any amount from their IRA that they want to.

However, if those distributions are taken before age 59½, they’re considered early distributions, and early distributions are subject to a 10 percent additional tax, commonly referred to as a 10 percent early distribution penalty. I purposefully used “additional tax” here because if income tax does not apply to a distribution, then this 10 percent penalty does not apply because, as the term suggests, it’s an additional tax, in addition to what already applies. So if you’re talking with a client, and you’re discussing the idea of the 10 percent penalty to determine whether or not it applies, you want to look at the client’s age, and you also want to look at whether or not the distribution is taxable.

When an individual reaches age 70½, they’re required to start taking distributions at that point. For the year in which an individual reaches age 70½, they must start taking required minimum distribution for that year, and continue for every year after.

We’re going to provide a high-level overview of the RMD requirements, but I want to take a minute to remind you that Roth IRA owners are not subject to required minimum distribution rules, and I’m emphasizing “owners” here.

From my experience, when I discuss the RMD rules with my clients, there’s a tendency to forget that beneficiaries are subject to the required minimum distribution rules, and for Roth IRAs, because it is a known fact that Roth IRA owners are not subject to the RMD rules, some people do forget that the beneficiaries though are subject to the required minimum distribution rules. So if you have clients who inherit Roth IRAs, you want to make sure that you remind them that they may need to take required minimum distributions from those Roth IRAs because if they don’t, they are going to be subject to the excess accumulation penalty, which we will review as well.

Distributions that Include Basis Amounts

Now typically when an individual takes a distribution from an IRA, the custodian reports it on IRS Form 1099R, which is a distribution statement. But the custodian, in most cases, reports a distribution as fully taxable. However, there are exceptions that will treat some amounts as nontaxable. For instance, if a distribution includes basis amounts, if it’s a return of excess contribution, if a distribution is properly rolled over, and for Roth IRAs, if distributions are qualified, then they’re completely tax and penalty free.

Let’s look at the first exception, which is basis. I find that in my practice, almost 90 percent of the time when I acquire a new client, and we talk about basis, the topic is foreign to them. What this tells me is that there are many clients out there who are paying income taxes on a balance that should be tax free. So the question becomes, how do you identify basis? How do you track basis? And how do you make sure your client does not pay income tax on basis? Because as I said before, basis should be tax free. If your client makes a nondeductible contribution to a traditional IRA, that creates basis.

Now a client can elect to treat a contribution that is deductible as nondeductible, or the client may not be eligible to claim a deduction because that client is covered under an employer sponsored retirement plan, such as a 401(k), and their income is above a certain amount. Now if you have a client who’s making a contribution to a traditional IRA, and that contribution is not deductible because of their income and their active participation status, or because they choose not to claim a deduction, and you want to make sure the client files Form 8606 to notify the IRS and their tax preparer that the contribution is not deductible. Basis also comes from rollovers of after-tax amounts from 401(k) plans.

In 401(k) plans, an individual could accrue after-tax amounts in certain instances. The plan administrator is required to issue a statement to anyone taking a distribution from a qualified plan to indicate how much of that amount is attributed to after-tax contributions. Any time that a nondeductible contribution is made to an IRA, or if an individual has basis in an IRA and takes a distribution or does a conversion from that IRA, then IRS Form 8606 must be filed.

Form 8606 helps to keep track of the basis in an individual’s IRA, and it tells the IRS that, for instance, if someone’s taking a distribution of $100,000 and $10,000 is not taxable because it’s attributed to basis, then Form 8606 is the form that is used to communicate that information to the IRS so the IRS doesn’t come knocking to say, “Your 1099R says you took a distribution of $100,000, but you’re only paying income tax on $90,000. Why is that?”

IRS instruction says if someone rolls over after-tax amounts from a 401(k), for instance, to an IRA, then Form 8606 is not required to be filed. That seems to me to leave a gap for purposes of tracking the after-tax amount, however you track it then. My recommendation, and of course deferring to a tax professional, is to complete the form anyway, and if needed, file the form with the IRS, even though they are saying it’s not required because that’s the only way to test if they’re keeping track of the basis amounts. Some people mistakenly believe that IRA custodians keep track of basis, and that’s not the case. One of the most common questions I get about this issue from tax professionals is, “The IRA custodian issued a 1099R to my client saying that the amount is fully taxable, when I know it’s not. What do I do then?” In that case, you want to file IRS Form 8606 to communicate to the IRS that only a portion of the distribution is taxable.

If someone has basis in their IRA, a distribution will always include a prorated amount of pre-tax and after-tax assets, and for this purpose, all of an individual’s traditional SEP and simple IRAs are treated as one. One of the questions I usually get is, “My client maintains two traditional IRAs, one which is basis, and one with the pretax amount. If my client takes a distribution from the IRA that has only basis, is that distribution completely tax free?” The answer is no. All of an individual’s traditional SEP and simple IRAs are treated as one for this purpose. So all of those balances will be aggregated to determine how much of that distribution is taxable and how much is not.

Excess Contributions

Excess contribution is a distribution that is not taxable. An excess contribution occurs when an individual contributes more than the amount for which he or she is eligible. Excess contributions should be removed from an IRA by the individual’s tax-filing due date plus extension. If someone made an excess contribution for the current tax year and filed their tax return by April 15 the next year, they still have until October 15th of the next year to correct that excess contribution by removing the amount, along with any net income attributable to the excess, which is NIA for short.

NIA can be earnings or losses. So as you meet with your client over these last few months and do your IRA checkup, if you do that in the last quarter of the year, I recommend checking to see whether or not they made excess contributions so that those can be corrected by the deadline. Because if they’re not corrected, the client will owe the IRS a 6 percent excise tax for every year it remains in the IRA.

In addition, if the excess contribution is in excess of the contribution, then it could also be subject to income tax if it’s not corrected by the deadline. Here is an example of Tim, who made an excess contribution of $5,000 to his traditional IRA in June. He corrected the excess by removing it in September at an earnings of $200. If Tim removes it properly, removes it by the deadline, and we’re assuming here that he corrects it in 2014, $5,000 is nontaxable, but the earnings is taxable in 2014 because it was corrected in 2014. As I said before, if excess contributions are not corrected by the deadline, the penalty is pretty stiff. Six percent may not sound like a lot, but if you’re thinking of an ineligible rollover, because those too can create excess contributions, think about a 6 percent penalty on $100,000 that accrues every year. It can be pretty costly in the long run.

IRA Rollover Distributions

Rollovers is another type of distribution that is not taxable, but it should be reported on the tax return. I get pushback from taxpayers and financial advisors on this transaction quite often because they’re thinking; you told me that if someone rolls over a distribution, it’s not taxable. Why is the IRS coming back to say, “How come it’s not reported on the tax return?” The requirement is it’s reportable, but it’s not taxable; therefore, it should be reported on the tax return as a nontaxable transaction.

We have to be reminded though that not all distributions can be rolled over. So if you’re meeting with a client and you’re discussing the idea of rolling over an amount to an IRA, you first want to make sure that your amount is in fact eligible to be rolled over. Ineligible rollovers include rollovers that miss the 60-day deadline, rollovers that violate the one per 12-month rule, and rollovers of ineligible amounts.

Ineligible rollovers will create excess contributions. In addition, the amount will no longer be eligible for tax-deferred treatment. Much of the assets that are in IRAs now are rolled over from qualified plans. So in order to help clients protect the tax-deferred nature of these assets, we want to make sure that when the rollovers are done, they’re done timely and they’re done properly.

Let’s talk about the 60-day rollover rule. Under the 60-day rollover rule, an individual that takes a distribution and wants to roll it back in, must complete that rollover within 60 days of receipt, unless an exception applies. Exception includes the first-time homebuyer exception or if the IRS waives the rollover. For IRS purposes, there’s an automatic waiver to the 60-day requirement.

For the first-time home-buyer exception, an individual can withdraw up to $10,000, which is a lifetime limit, for a first-time home-buyer exception, and this can be used to buy, build or rebuild a first-time home for an eligible person. But you know, sometimes you plan to build or rebuild a home and things happen, and the deal falls through. What if that happens after the 60th day? Well, there’s a provision that says the 60-day period is extended to 120 days under those circumstances. So if you’re meeting with a client who missed the 60-day, I would recommend you try to find out the circumstances of the distribution, and find out why the 60-day period was not met, to see if they qualify for the exception.

IRS Waiver of the 60-Day Rollover Rule

What if someone takes a distribution and they intended to roll it over, but they missed the 60-day deadline? Are there any exceptions that would allow that rollover to still be made? The answer is yes. Now there’s a provision that allows the IRS to waive the 60-day requirement if failure to do so was caused by an event of a casualty, disaster or other event beyond the participant’s reasonable control. When I get questions from clients about this automatic rollover, this 60-day rollover exception, one of the first things I try to do is to find out whether or not they qualify for the automatic waiver. Because, as you’re going to find out in a second, going to the IRS to ask for a waiver can be a costly process. So the first thing to do is to find out if the client qualifies for an automatic waiver.

Under the automatic waiver provision, if the client comes to your office, hands you a check for a rollover, and did everything that is required by your financial institution, and met those requirements within the 60-day period, then there’s no need to go to the IRS, as long as you can correct an error by redepositing the amount in the IRA within a year. So when clients ask you, for instance – and I had a conversation with a financial advisor recently, and he couldn’t believe that this type of thing happens – where someone walks into a bank and hands the bank a check to say, “Deposit this,” and someone either keeps it in their drawer, never makes the deposit, or it goes into a different type of account. For example, it goes into a checking account instead of an IRA. Now in situations like that, if you discover the error, and it’s just within a year, then the IRS says and the Tax Code says that you can book in that rollover, and it’s perfectly fine.

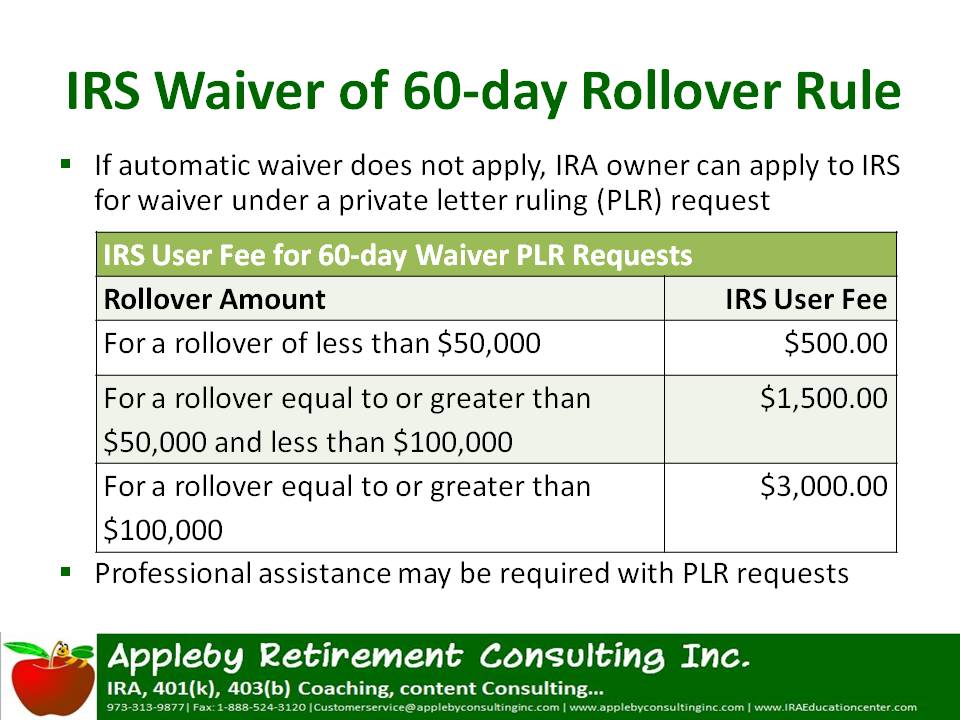

Now the question becomes what if it’s after this one-year period? What happens then? Then as a financial professional, your hands are tied. In that case, the client would then need to apply to the IRS for a waiver under the private letter ruling request process. The challenge though is that there’s no guarantee that the IRS will approve the waiver request. In addition to that, the professional, if the client uses one to work with the IRS to apply for a waiver, may charge a fee, and the IRS also charges a fee, depending on the amount. In this fee schedule here, I’m showing how much the IRS will charge, depending on how much the client wants the exception to be approved for.

Now when determining whether or not to approve a waiver request, the IRS looks at certain things. For instance, whether or not the error was made by a financial institution, if the individual was very ill or in prison and couldn’t complete the rollover, how much time has passed, and whether or not the funds were used.

For instance, the IRS may not approve a waiver if, during the 60-day period, the individual was using the money for something else, and couldn’t have completed the rollover anyway because the funds were in use. But my recommendation is, as a financial professional, never to make that decision on behalf of the IRS, but to recommend that a client work with a tax professional, who would in turn work with the IRS, who’s going to determine if the exception can be made.

One-per-12-Month Rule

The one-per-year rollover rule is another instance where, if this rule is broken, a rollover then cannot be made.

This is very important here because the rules are going to change come January 1 of next year. Now as I’m sure all of you know, if someone takes a distribution from an IRA – and as I just explained, that distribution can be rolled over within 60 days; however, there is some confusion as to how this worked because IRS Publication 590, issued by the IRS, did not agree with the Tax Code, or their explanation was different from what was in the Tax Code. So for many taxpayers, they understood, as was provided in the IRS Publication 590, that an individual could do one rollover per 12-month period, per IRA.

So if you had two IRAs, for instance, you could take a distribution from IRA No. 1 and roll it over to IRA No. 1, and within the next 12 months, or whenever you wanted to, take a distribution from IRA No. 2 and roll over that distribution to IRA No. 2. Now a tax attorney, following IRS Publication 590, felt it was okay to do this, and did just that. Someone at the IRS was reviewing his tax return and said, “Something looks funny here, as is evidenced by the multiple 1099Rs and multiple 5498s, which is what he used to report rollover contributions. This individual did more than one IRA to IRA rollover during a 12-month period.”

So they determined that the second rollover was ineligible. He’s thinking, “My rollover is nontaxable because it was done in 60 days,” and the IRS is saying, “No, it’s not. You not only owe income taxes, but you owe penalties for failure to pay income tax on the amount that should have been taxed.” Of course, knowing that the IRS provided instructions in Publication 590, he disagreed with them, and he took them to court. But he lost the case because the Tax Code agreed with the person who reviewed his tax return. Now the question becomes, what will you do when there’s a discrepancy between the Tax Code and IRS publications?

The IRS will tell you that you cannot rely on publications such as Publication 590. You have to go to the Tax Code if you want something to rely on. So they denied his second rollover and he owed the IRS income tax on that amount. The question in front of the IRS was, what happens to the millions of people who have been doing just what he was doing? They decided that, up until December 31, 2014, they’re going to allow the rules to stand, as it is explained in Publication 590, until January 1, 2015, when they’ll start to follow the Tax Board interpretation of the Tax Code.

So come January ’15, if you’re discussing rollovers with a client, it’s important to remind them that if they take a distribution from an IRA and roll it over within 60 days, they are locked up for the next 12 months because no longer can they do multiple IRA to IRA rollovers during a 12-month period. What is unclear, though, is whether or not this limitation applies to traditional or Roth IRAs as an aggregate basis. So we’re waiting on the IRS for guidance on that.

I also want to remind you because this is a question I get often too. This does not apply to rollovers from IRAs to 401(k)s, or from 401(k)s to IRAs. It only applies to rollovers between two IRAs. So from a traditional IRA to a traditional IRA, yes, this limitation takes effect January 1, 2015.

Rollovers of Ineligible Amounts

This is a big one, and I see this a lot. If you’re meeting with a client who wants to make a rollover contribution, I recommend making sure that the amount is eligible to roll over. The biggest one I see is rollover of required minimum distributions. Someone will take a distribution from a 401(k) for instance, rolls it over to the IRA, and it includes an RMD.

Here’s why I think this mistake is usually made. The regulations say that for any year an individual is required to take an RMD. The first distribution always includes that RMD. Many people forget that. So let’s assume that an individual’s RMD for this year is $10,000. They’ll take a distribution of $100,000, roll it over and plan to take the $10,000 later. But that is not permitted because, as I said before, the first distribution always includes your RMD. So if you meet a client who’s taking a distribution, of course you want to check their age to see whether or not they’re subject to the RMD rules. Sometimes if they have assets in a qualified plan and they’re still working, the plan may allow them to defer RMD past age 70½.

But whatever the case is, you want to find out if they’re subject to an RMD for that year, and if they are, make sure they take the RMD before they perform any rollover. Otherwise, the rollover will include RMD amount, which is an ineligible rollover, and ineligible rollovers will create excess contributions in IRAs. Distributions that miss the 60-day deadlines are also ineligible unless an exception applies, and distributions that violate the one per 12-month rule also create ineligible rollovers and excess contributions in IRAs. In some cases when these amounts were distributed, they could also be taxable if the amount is in excess of the contribution limit for the year, which is usually the case if someone’s rolling over large 401(k) balances to their IRAs.

Early Distributions

Early distributions are subject to a 10 percent early distribution penalty, unless an exception applies. I like to keep a checklist of the exceptions to find out whether or not clients are eligible for exceptions.

Here’s why I think it’s important to keep a checklist. The exceptions that apply to an IRA may not apply to a 401(k), and the exceptions that apply to a 401(k) may not apply to an IRA. So if you’re meeting with a client who’s taking a distribution from a retirement account, and the client is on age 59½, you want to check to see whether or not they qualify for an exception based on the type of retirement plan. Of course, there are some exceptions that apply to both types of retirement accounts. [Editor’s note: Please visit Denise’s website for a checklist of the exceptions that apply to IRAs.]

I want to tell you about a particular case that I reviewed a few months ago. This gentleman had assets in a 401(k) account, and he was no longer working for the employer. When he separated from service with the employer, he was past age 55, but under the age 59½.

There’s a rule that says if you separate from service in the year in which you reach age 55 or later, and you take a distribution after you separate from service, that distribution is not subject to the 10 percent early distribution penalty. He knew that. He rolled over that distribution from the 401(k) to his IRA, and then he took the distribution from the IRA.

Here’s what he did wrong or what he was not aware of. That exception that I just explained applies only to 401(k) qualified plans and 403(b)s. It does not apply to IRAs. So when he filed his tax return, he did not pay the 10 percent penalty. Of course, the IRS wrote him asking for the penalty amount. He didn’t think it applied, and he took the IRS to court, and of course, he lost. The reason I’m telling you this story is it’s important to check with clients to make sure that they’re not giving up an exception by moving assets from one retirement account to another.

For instance, if you have a client who’s rolling over assets from a 401(k) to an IRA, check to see whether or not they will lose any of the exceptions that apply to the 401(k) when those assets are moved to the IRA. If that’s the case and they want to make a withdrawal, it’s best to make a withdrawal from the 401(k) directly to themselves, and then roll over the balance so that they are not subject to the 10 percent early distribution penalty, when they could have been eligible for a waiver.

Required Minimum Distributions for Traditional IRAs

This is important now because it’s coming to year end, when most individuals who are age 70½ or older, will be required to take a required minimum distribution. IRA custodians are required to either calculate the RMD amount or offer to calculate the RMD amount upon request. But if you’re meeting with a client who just turned age 70½ this year, that client has until April 1 of next year to take their first RMD. That extension only applies to the first year. The question becomes should that client take advantage of that exception?

The answer is, “It depends.” If someone does not take their first RMD this year and waits until next year, they will be required to take two RMDs next year. The reason is, RMDs for every other year must be taken by December 31 of that year. For someone who’s taking two RMDs in a year, it could put them in a higher tax bracket, which could cause them to pay more income tax. That’s not always the case though. So my recommendation is, if you’re meeting with a client and the issue comes up as to whether or not they should defer taking their first RMD until next year, have the tax preparer do an analysis to determine which option is better from a tax perspective.

Ultimately it really comes down to income taxes because that’s going to determine how much the individual is left with in the end. Calculating the RMD seems pretty easy, right? You use the market value for the previous year end, and the individual’s life expectancy. But mistakes are usually made, and one of the most common mistakes is using the wrong fair market value. If the fair market value that is used is less than what it should be, then the individual will have an RMD shortfall, and could cause them to be subject to a 50 percent excess accumulation penalty.

If you’re helping a client calculate an RMD, find out whether or not they have outstanding transactions because these should be added back to the fair market value. IRA custodians are required to calculate the RMD, but they’re not required to check for outstanding transactions. So as the financial professional who’s advising the client, you want to ask them, “Do you have an outstanding rollover, an outstanding recharacterization, or an outstanding transfer?”

An outstanding rollover occurs if someone takes a distribution one year, and the amount is rolled over in another year. This could happen if someone takes a distribution in December, for instance, and rolls it over in January. A common one is someone who does a conversion, moves money from a traditional to a Roth, for instance, and reverses that amount by recharacterization in the following year. These amounts should be added back to the fair market value just to make sure that the RMD calculation is correct. IRA custodians are required to provide an RMD notice by January 31 of the year for which the RMD is due, and that notification must include an offer to calculate the amount upon request, or include the calculated amount. But even if the custodian does provide a calculation, I still recommend that you double check it anyway, just to make sure it’s correct. Ultimately it’s the client who’s going to be responsible for paying any penalty that’s due.

Typically, the uniform lifetime table is used, and this assumes that the beneficiary is ten years younger than the retirement account owner. There’s an exception to using the uniform lifetime table though; this exception applies to a spouse beneficiary, who’s more than ten years younger than the retirement account owner. In that case, the joint life table can be used, which produces a lower RMD amount, which can be beneficial for those clients because I find that in many cases, individuals, especially if they’re still working, they don’t want to take RMDs. So if you can find a way to have them take less than the amount that they think they should take, they’ll probably appreciate that.

Other RMD rules that you should bear in mind is the RMD aggregation rule. If an individual has multiple IRAs, the RMDs must be calculated separately for those IRAs, but can be aggregated and taken from one or more of those IRAs. You cannot aggregate RMDs for 401(k)s and IRAs, or for IRAs and 403(b)s. Another mistake that I see happening quite often, the aggregation has to be done only between multiple traditional IRAs.

If you’re meeting with a client who’s in an RMD year, make sure that the RMD is taken before any rollover is made. If they’re doing a trustee to trustee transfer between two IRAs, it’s not necessary to take the RMD before the transfer is done, as long as the RMD is taken from the receiving IRA by December 31 of the year for which the RMD is due.

In the case where someone took a distribution, thinking they’re going to roll over their full distribution because I’ll take my RMDs later: I just want to repeat here for emphasis, you cannot leave the RMD behind to take it later. It’s always included in the first distribution, and therefore is not rollover eligible.

RMD for year of death: This is an important one too. If you’re meeting with a client who just inherited a retirement account, and then the decedent was subject to the RMD rules, but didn’t take the RMD for the year of death, the question is, who is going to take the RMD then? Well, when an IRA owner dies, the IRA immediately becomes the property of the beneficiary, so you can no longer report distributions to that decedent.

For the RMD for the year of death, this means that if it was not taken by the decedent, it must be taken by the beneficiary, and you will probably get a lot of pushback from clients about this because they’re thinking, “It’s not my RMD! Why should I be responsible for taking it? Why should I be paying income taxes on it when it’s not mine?” Well, that’s what the Tax Code says. The beneficiary gets the distribution; it’s reported on their 1099R and on their Social Security number. So they’re responsible for including it in income, and this cannot be rolled over.

If you have a spouse beneficiary who’s eligible to roll over the amounts that she inherits from her deceased spouse, that RMD must be taken before rollover, and must be reported on the name and Social Security number of the beneficiary. So what happens if someone doesn’t take their RMD by the deadline? Well, the penalty is very severe. It’s a 50 percent excess accumulation penalty. Imagine someone who’s RMD is $8,000, and he didn’t take the RMD by the deadline. He’s going to owe the IRS, a 50 percent excess accumulation penalty, which is $4,000.

I’m sure you’ll agree that that’s a pretty stiff penalty. However, if you meet with a client who missed their RMD deadline, my recommendation is have them talk to their tax preparer about asking IRS for a waiver. Because the IRS will waive this penalty if the deadline was missed due to reasonable cause, however they haven’t defined what reasonable cause is. But let’s say, for instance, they didn’t get an RMD notification or something else happened that prevented them from taking the RMD that was beyond their control. Then the process is to withdraw the RMD as soon as possible, file IRS Form 5329 to ask for a waiver, and include proof that steps have been taken to remedy the shortfall.

Qualified Roth IRA Distributions

Qualified Roth IRA distributions are also tax and penalty free. This is one of those areas that I like to review by itself because I get so many questions, and it seems to be confusing, one of the more confusing topics. An approach that I like to take is if you’re trying to find out whether or not a Roth IRA distribution is tax-free, first find out if it’s qualified. That’s the easiest approach.

A qualified distribution occurs if it has been at least five years since the individual funded his or her first Roth IRA, and the individual is at least age 59½, is deceased, in which case it’s taken by the beneficiary, is disabled, or if the amount is being used for a first-time home-buyer purchase. If those requirements are met, then the distribution is tax and penalty free. If not, then we need to use what is referred to as the ordering rules, so as to determine if the distribution is subject to income tax and/or a 10 percent early distribution penalty.

In that case, you will use what is referred to as “ordering rules”. Under the ordering rules, regular Roth IRA contributions are distributed first. Those are always tax and penalty free. Roth conversions are distributed next, on a first-in first-out basis. These are tax free, but they’re subject to a 10 percent penalty if the individual is under age 59½ unless an exception applies. The earnings are distributed last. Those are taxable, and they’re subject to a 10 percent early distribution penalty if withdrawn before age 59½ unless an exception applies.

Beneficiary Distributions

Beneficiary distributions is another area that we need to focus on, especially since it’s coming on to year end because beneficiaries too are subject to the required minimum distribution rules.

The options that are available to a beneficiary is determined by whether or not the beneficiary is a designated beneficiary, and whether or not the retirement account owner died before the required beginning date or on or after the required beginning date. The required beginning date is April 1 of the year following the year in which the individual reaches age 70½.

The distribution options for spouses are different from those that apply to a non-spouse beneficiary. A spouse beneficiary does have the option to treat an inherited IRA as her own, by rolling over or transferring their amount of her own retirement account. Or the spouse beneficiary can choose distributions under the life expectancy method. Under the life expectancy method, distributions must usually begin by December 31 of the year following the year of death. But if the individual dies before the required beginning date, then distributions need not begin until December 31 of the year in which the decedent would have reached age 70½.

In a case that I came across again recently, this lady inherited an IRA from her husband, and she knew that because it was an inherited IRA distributions from the inherited IRA are not subject to the 10 percent early distribution penalty. However, here’s where she made a mistake. She transferred those amounts to her own IRA, which she had the right to do as a spouse beneficiary. The issue is, once she transferred it to her own IRA, she lost the benefit of the exception from an inherited IRA.

The lesson here is, if you’re meeting with a spouse beneficiary who is asking what to do with an IRA that she inherited from her spouse, find out first if she’s under age 59½, and if so, whether or not she needs to take distributions. If that’s the case, then she may want to leave it in an inherited IRA, take distributions from the inherited IRA where the 10 percent penalty would not apply, and once she reaches age 59½, then she can move the amount to her own IRA where the 10 percent early distribution penalty would not apply.

The non-spouse beneficiary option too depends on the age at which the retirement account owner died. If the owner died before the required beginning date, the five-year rule is an option, or the life-expectancy option. If the owner dies on or after the required beginning date, the life-expectancy payment is the only option. In that case, distributions can be taken over the longer of the remaining life expectancy of the decedent or the life expectancy of the beneficiary. The question I get most about the five-year rule is whether or not it always applies, and the answer is no. It only applies if the retirement account owner died before the required beginning date.

Now here’s a tip for you. If you’re meeting with a client who inherits a retirement account and they’re subject to the five-year rule because the document does not allow life expectancy option, and you want the client to get around that, that can be accomplished by transferring the assets to an inherited IRA that allows a life expectancy payment, as long as the transfer is done by December 31 of the year following the year of death. This can also be done with assets that are rolled over from a qualified plan, where the qualified plan only allows the five-year rule as an option. This is very important if you want to allow for extensive distribution planning, such as stretch IRA distributions with your client.

For a non-spouse beneficiary, the options are more limited. If the owner dies before the required beginning date, the five-year option is the only option. If the owner dies on or after the required beginning date, then distributions can be taken over the remaining life expectancy of the decedent. Of course, taking a lump-sum distribution is always an option.

Tax Withholding

Now tax withholding is another area that is often overlooked. If someone need to take a required distribution, they can choose whether or not to have taxes withheld. If they do not make an election, then the custodian is required to withhold 10 percent. If they want to make an election, it has to be 10 percent or more. It can’t be 1 or 5 percent; it’s a provision of the Tax Code. An IRA custodian must withhold either 0, 10 percent or more.

Of course, the amount that is withheld is treated as part of the distribution, so that’s going to be reported on the 1099R as a distribution as well.

Tax Reporting

Distributions are reported on 1099R by the custodian. I think that is known by most everyone. What I find that most people forget though, is how to report a distribution on a 1040 if the amount is rolled over. You’ll probably get pushback from accountants on that because I do get that a lot. I work with them through the instructions for filing 1040, and it’s very clear if someone takes a distribution and rolls it over, it’s reported on Line 15 of 1040.

If the distribution is from a 401(k), it’s Line 16. I’m just mentioning the line number here, but you don’t need to remember that because it’s the tax preparer’s job to know what line it’s reported on. But what I want to highlight here is the fact that it must be reported. So if someone challenges you on a 1099R that was issued, then you have something on which to stand on, the instructions for 1040, which confirms that it should be reported.

Remind clients that Form 8606 should be filed to keep track of basis. This is the responsibility of the IRA owner, or whoever they hire to prepare their tax return. Form 5329 is also filed by the retirement account owner or the tax preparer, and this is used to report penalties, such as the excess accumulation penalty if the RMD deadline is missed. It can also be used to request a waiver of that penalty. Form 5329 is also used to correct early distribution reporting. If the custodian issues a 1099R saying that an amount is subject to the 10 percent penalty when it’s not, or vice versa, then this 5329 can be used to correct that tax reporting.

Takeaways

- The 10 percent early distribution penalty. Check to make sure that the client is eligible for the exception and check by plan type. The example I gave, the age 55 exception, applies to qualified plans. It does not apply to IRAs. Another example is distributions under a divorce from a qualified domestic relations order. Exceptions apply if the amount is from a 401(k). Once the amount is rolled over to an IRA, it loses that exception. The first-time home-buyer exception and higher education expenses, those apply to IRAs. They don’t apply to qualified plans. So before a client rolls over assets between different plan types, check to see if they are giving up any exceptions for which they are eligible.

- Remind clients that not all distributions can be rolled over. When you’re doing your annual IRA checkups, or however often you do it, check for ineligible contributions and make sure that they are corrected by the deadline. Send out a reminder to clients if they want to do the new IRA to IRA rollover.

- Remind clients to take their RMDs by the deadline because if they don’t, it’s going to be subject to a 50 percent excess accumulation penalty. But if the penalty applies, all is not lost because a waiver can be requested from the IRS. In my experience, and I’ve come across many cases in which the waiver has been requested, the IRS has not said no yet. It’s very likely that if your client is subject to this penalty, they could get a waiver of the amount, as long as the proper procedures are followed.

- Remind clients that they’re responsible for keeping track of basis. There are too many people out there who are paying income tax on IRA distributions that should be tax free. Keep track of Form 8606. This is especially important as they move from one tax preparer to another, and when beneficiaries inherit a retirement account, in a lot of cases, beneficiaries who inherit these retirement accounts do not have the tax filing information of the retirement account owner, so they’re unaware of the fact that this $100,000 IRA that they inherited, maybe 20 percent of it should be tax free, so they end up paying income tax on amounts that shouldn’t be taxable.

- When clients want to move assets from one IRA to another, encourage them to use the transfer method. They can do as many transfers as they want, as often as they want to, as opposed to a rollover that can only be done once during a 12-month period. Unless the client really needs to use the funds on a short-term basis, encourage them to use transfers instead. In my experience, I’ve never seen a transfer in which a mistake occurs unless it went into a wrong account, and that’s usually an easy fix. If you’re talking about rollovers, you have the 60-day deadline. Things could happen that cause them to miss the 60-day deadline, such as violating the one per 12-month rule, or rolling over ineligible amounts.

About the author:

Denise Appleby, CISP, CRC®, CRPS, CRSP, APA, President of Appleby Retirement Consulting, Inc., provides technical consulting, coaching and marketing-content to financial, tax and legal professionals. She has more than 15 years’ experience in the IRA and defined contribution plans fields. She has held several senior retirement plans related positions with Pershing LLC and has written over 400 articles for many newsletters, newspapers and website.

Denise has co-authored the following three books on retirement accounts:

– Roth IRA Answer Book

– Quick Reference to IRAs

– Adviser’s Guide to Retirement Plans for Small Businesses

She has also provided technical editing to several other retirement plan-related books.

Her expertise and knack of explaining complex retirement plans rules and regulations so that they are easily understood, led her to create several professional and client Quick Reference and other aides which we’ll share more about with you at the end of this session.

Denise is a Rutgers State University graduate, holds the following professional certifications:

- Certified IRA Services Professional (CISP), Institute Of Certified Bankers, Washington DC

- Certified Retirement Counselor® (CRC®), International Foundation for Retirement Education (InFRE)

- Accredited Pension Administrator (APA), National Institute of Pension Administrators, Chicago IL, among others

Are you looking for a retirement speaker for your next conference, consumer event or internal professional development program? Visit the Retirement Speakers Bureau to find leading retirement industry speakers, authors, trainers and professional development experts who can address your audience’s needs and budget.

©2014, Denise Appleby, APA, CISP, CRPS, CRC®, CRSP, Founder and Owner of Appleby Retirement Consulting, Inc. All rights reserved. Used with permission.