David Armes, CFP®, Principal of Dover Healthcare Planning, LLC

Editor’s note: This article is an adaptation of the live webinar delivered by David Armes, CFP® in 2017. His comments have been edited for clarity and length.

You can read the summary article here as part of the 1st Qtr 2017 Retirement InSight and Trends Newsletter, worth 1.0 CE when read in its entirety (after passing the online quiz.

You may also choose to take the full length course Three Steps to Helping Clients Manage Health Care Costs in Retirement – David Armes for 1.0 hour continuing education (CE) credit.

By David Armes, CFP®, Principal of Dover Healthcare Planning, LLC

How are healthcare costs different? They increase at faster rates than other kinds of retirement spending. Over the last 20 years, healthcare inflation has risen at an average annual rate of about 2 percent more than other types of consumer inflation. Over time, for retirees who have fixed incomes, as you can imagine, this starts to crowd out other types of spending.

Healthcare costs are also more complex. Probably the most frequent complaint about Medicare is, “What do you do with all of these parts?” Parts A, B, C, and D have different enrollment timelines and rules. Depending on when you enroll, you can put Part A, Part B, and Part D in a Part C plan, which is an Advantage Plan, except that some Advantage Plans don’t include Part D, so you have to enroll in a standalone drug plan, and on and on, and after about 20 seconds of that, most people’s eyes start to glaze over. Even if it’s explained clearly and they understand it for the moment, if they don’t deal with it, then they forget what they’re supposed to do.

That’s different, I think, from other kinds of retirement spending. Housing costs, which is the largest spending category in retirement, are not complicated for most people. They know their options. If they need to cut costs, they can downsize or take out a reverse mortgage. They’ve been dealing with those issues their whole lives. Medicare and healthcare terminology, though, baffles them, so they don’t know what to do.

Costs are unpredictable. They bounce around more than other types of retirement spending, some types substantially so. I recall a conversation a few months ago, during Open Enrollment, with a woman had been tracking her healthcare costs. She was in her early 70s. It had risen about 4 percent a year. Her doctor had just prescribed a brand-name drug for a condition she had. It wasn’t a serious condition, but he wanted her to take it. Her costs were going to jump about 40 percent in one year because of that drug. There was nothing she could do, and she was, if not distraught, at least seriously concerned.

The final factor, and we’ll talk more about this on subsequent slides, is that, in retirement, the costs are heavily tilted toward later years, in part because they’re increasing at faster rates, but also because people are using more medical services.

I think you can start to understand some of retirees’ concerns when healthcare comes up in surveys because they have no control at all over the first three of these: healthcare inflation, the complexity of Medicare’s rules, and the unpredictability of their own health. They can do some things about the tilt toward later years, but there are also many things they can’t do. So, they feel, among other things, very little control over the things that they need to do.

Out of Pocket Healthcare Costs are the Culprit

Just about everybody is aware that costs go up as you grow older, but the incline is more significant than many people are aware of. A planning assumption is that an 85-year-old is going to spend two times as much out-of-pocket as a 65-year-old in the same year. Using future dollars, if a 65-year-old woman lived to be 95, then she would pay one-fourth of her total retirement healthcare costs after her 90th birthday.

It’s not healthcare inflation that’s at work here. It’s the increased use of medical services. Roughly 80 percent of people with Medicare are in some form of group plan – Medicare Advantage Plans, employer plans, or community-rated Medigap policies – and as we know, all group plans have the same premiums for people regardless of their age or health status, so a premium for a 95-year-old and 65-year-old is the same.

Most people in Medicare are in some form of a group plan, so the reason for this increased spending is not the premiums. It’s that they’re going to their doctors more often. They’re taking more prescription drugs. They’re taking more brand-name drugs. They’re more likely to use services that are not covered by Medicare for which they have to pay the full out-of-pocket cost.

When I was a Medicare counselor, this is what surprised me. I saw executives of companies, who I knew had to have substantial pensions, coming and saying, “I need to do something about my health costs. They’re really starting to hurt.” More often than not, it was prescription drug costs. They were in the wrong plan or, in some cases, a Medigap policy.

Any strategy that’s effective in controlling healthcare costs is going to have to deal with this latter half of retirement because that’s where most of the costs are going to be spent. However, while costs are going up, people are increasingly less likely to do the things necessary to manage those costs. In some cases, it’s mental incapacity. In some cases, they’re just not as willing to spend the time and effort necessary to do it. So, while the financial stakes are increasing, the likelihood of people trying to manage their healthcare is decreasing.

The Medicare Payment Advisory Commission has done quite a bit of research on this. The overall switching rate among plans for all Medicare beneficiaries is about 13 percent. For people in their 60s, it’s 15 percent, but by the time they get to their 80s, it’s below 10 percent.

Most clients are concerned about healthcare costs and they want some advice. The Gallup organization, last year, wrote a paper saying that in the 15 years since they started, in 2001, interviewing retirees about their top-two concerns in retirement, the top-two concerns had not changed in any of those 15 years. No. 1 is that most retirees are concerned about not having enough money or about running out of money. No. 2 is healthcare costs, and that’s been consistent over 15 years.

At the same time, other surveys show that most financial planners do not try to help their clients manage these costs, maybe because there are so many kinds of coverage, but there’s just a lack of information here on the part of financial planners as a whole. When I’ve spoken at Financial Planning Association (FPA) meetings seen maybe a third to 40 percent of the people say they actively try to help. Other surveys show much lower participation.

The First Step: Make One-Time Estimates of Spending

We’re going to talk briefly about three fairly simple ways, I think, to help clients. In most of these steps, the clients are going to do much of the work. They’re the ones who have to manage their healthcare costs.

The first way is to make one-time estimates of how much a client may spend on retirement healthcare. Estimates are going to be imprecise by their very nature. I’ve learned that it’s good to come up with a bunch of them. They’re going to be different, but there are two possible benefits to doing this. If it’s done accurately, it’s going to result in a large number.

When people see a large number and can grasp the potential magnitude of the spending, it may motivate some of them to try to manage their spending better as they go through retirement, and it may cause some of them to change their coverage. In early retirement, people tend to be too optimistic and choose expensive coverage. So, there’s some value to this, not as a predictive device but just as something to raise consciousness. A few years ago, Fidelity took a survey of over 1,000 pre-retirees, and nearly half of them said that they thought their retirement healthcare would cost about $50,000, on average, which is much too low.

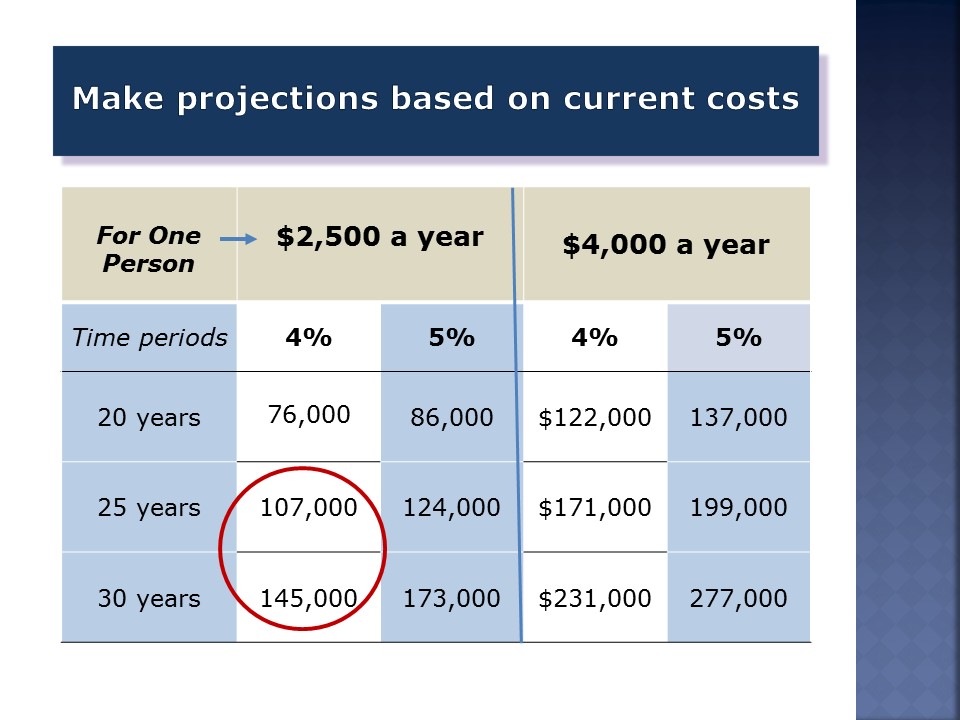

One way to do it, if someone is already 65 or older and using Medicare, is by asking them, “Would you like to do some projections of your costs under different scenarios over different time periods?” If they say yes, you would respond by saying, “Could you give me an estimate, then, of how much you spend?” “$2,500 a year,” says somebody with an Advantage Plan. This year, Part B premiums for incoming enrollees are going to be over $1,600. So, that’s somebody who’s an Advantage Plan and who takes one or two generic drugs, a pretty low number. $4,000 is for somebody who takes one or two generic drugs and has a Medigap policy. You just project them straight line.

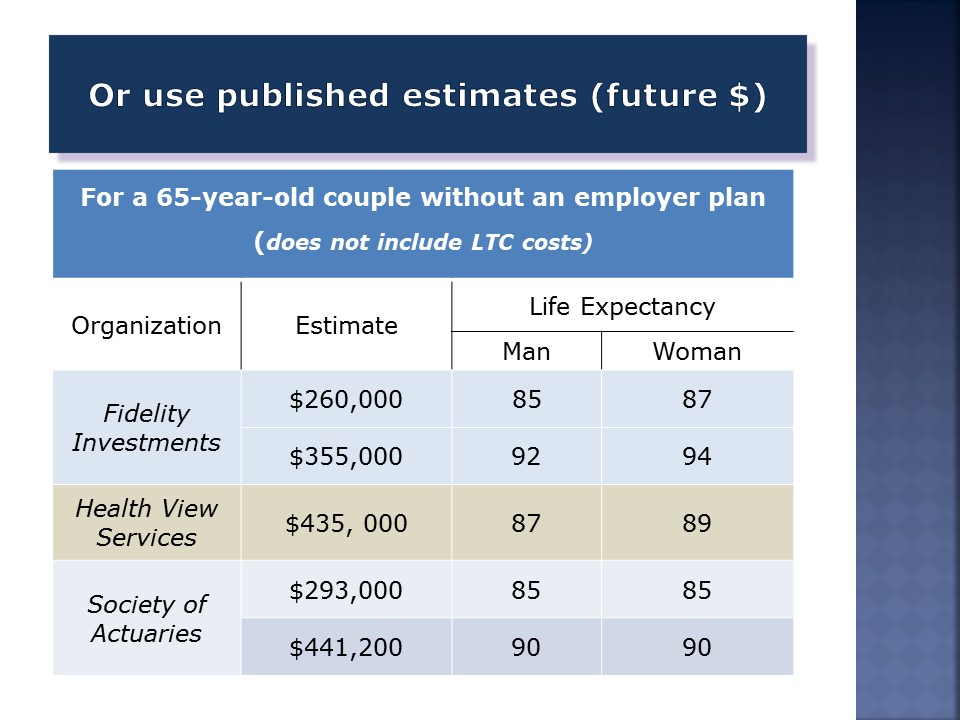

You can also use published estimates for people who have not yet started Medicare. The current-cost would not be a good starting point for projections. None of these include long-term care costs. The costs on the prior slide were for an individual. These are for a 65-year-old couple.

The first two, published in these estimates here by Fidelity (and Health View, were both done in the last year. The Society of Actuaries did theirs three years ago. These are after-tax estimates, in most cases. It’s probably a mistake to focus on any of these numbers. There is tremendous variance here; almost 2-to-1. Using different assumptions of healthcare inflation, life expectancy, and healthcare costs, there’s that element of unpredictability that we’ve talked about.

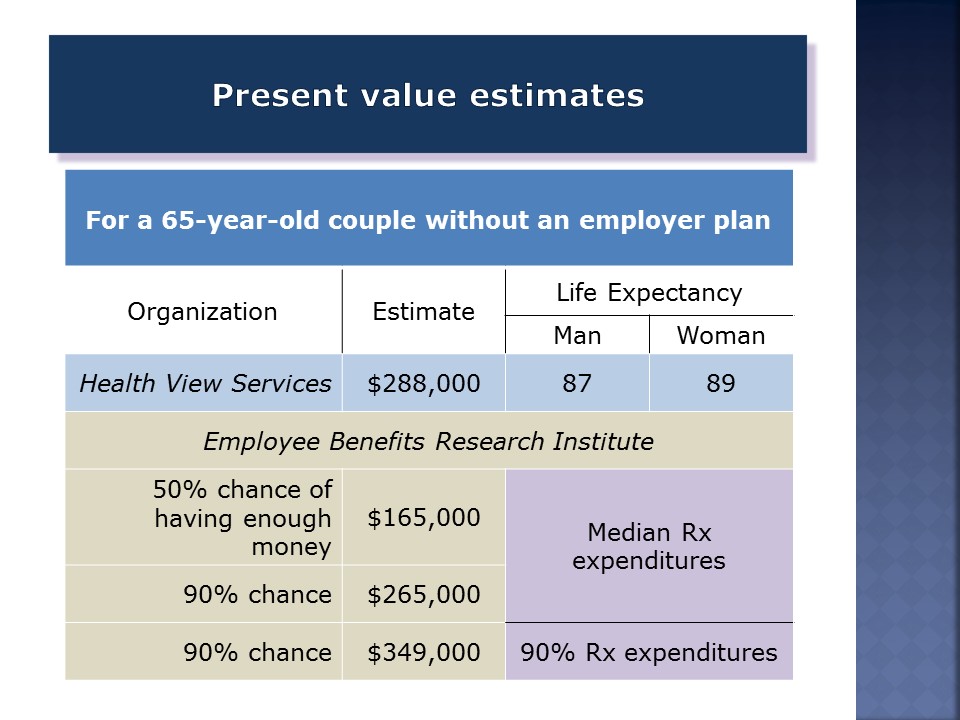

The Employee Benefits Research Institute has the most gravitas here. They’ve been doing this for 25 years. They do 100,000 Monte Carlo simulations for each of these outcomes, and then they assume that the savings are set aside at the start of retirement. They earn a 7.3 percent after-tax return, which is probably optimistic for a balanced portfolio.

Look at the variance depending on the level of prescription drug expenses and the probability that you will have enough. If you want a 90 percent probability and you’re in the 90 percentile range of prescription drug expenses, you’re going to spend twice as much as if you were in the median Rx drug expenditures and only want a 50 percent chance.

The Second Step: Suggest Clients Choose the Coverage that Best Matches Their Needs

Now we’ve come to the meat of what maybe retirees need to do and what planners can advise them about: suggest to them that they choose the coverage that matches their needs. Recommend that they reevaluate their coverage each year during Open Enrollment.

Study after study shows that this just does not happen, and that many retirees waste tens of thousands of dollars during the course of their retirement because they never look at their coverage. It’s like they had an investment portfolio that they started when they were 65, they never rebalanced it, and they never went back to review it. They just left it alone. Unfortunately, that happens.

Two kinds of coverage: Very comprehensive and less comprehensive

Although it’s an oversimplification, we might just say that there are two kinds of coverage: very comprehensive and less comprehensive.

Who should get comprehensive coverage? It’s going to be more expensive. People in poor health should get it, and the reason is that they are going to use a lot of medical services, and they’re going to use their benefits. Unlike property and casualty insurance, their premiums are not going to go up any more than anybody else’s in their rate class because they have excessive claims, so they’re going to save money.

There have been studies on this. People who are on disability, or are under 65 and have SSDI, and then who get a one-time enrollment period when they turn 65 to buy a Medigap policy almost always will buy it because they know they will come out financially ahead if they can afford it. Medigap plans here are the proxy that I’m using for comprehensive coverage because most of the Medigap plans – there are ten of them – are very comprehensive, and they’re great coverage if you can afford them. The most comprehensive of the Medigap policies, which is Plan F, is the one that’s most commonly sold because it generates the highest commissions.

The other people who, if you’re matching needs to coverage, probably should get it are affluent people who say, “I can afford it, and I want the best coverage.” Medigap plans have no network restrictions. You never have to get prior approvals. You can go to the Mayo Clinic this week and Johns Hopkins next week, and they both will probably be covered. The insurance company never makes its coverage decision in these policies.

How much does a Medigap policy cost? It varies quite a bit, but I would say $100,000 for someone over a 25-year period. A 65-year-old who lives to 90 will pay $100,000 in premiums. The average starting premium in the United States today is just under $2,400. If you push that out at 4 percent, you’re going to come up to about $100,000 at age 90. There are very few medical copayments in that. It would only be for things that Medicare doesn’t cover, and you will still have prescription drug costs and Part B premiums. Your entire cost is in the premium, but it’s a high cost. If you happen to live to be 95, a 65-year-old buying a comprehensive Medigap Plan F policy will probably pay about $130,000.

The other people who are more or less forced to get comprehensive coverage are people who don’t have any good Advantage Plans in their area. The Plains states – North Dakota, Kansas, Wyoming, and South Dakota – all have 50 percent Medigap penetration rates, and that’s just because there are not any Advantage Plans there that have their doctors in network. The closest network doctor might be 75 miles away. They are rural areas, and even though you can get in a regional PPO and go to an out-of-network doctor, you may pay 40 percent of cost, and it just makes more sense, for many of those people, to get the Medigap policies.

Who should not comprehensive coverage? It’s just the reverse side of the coin.

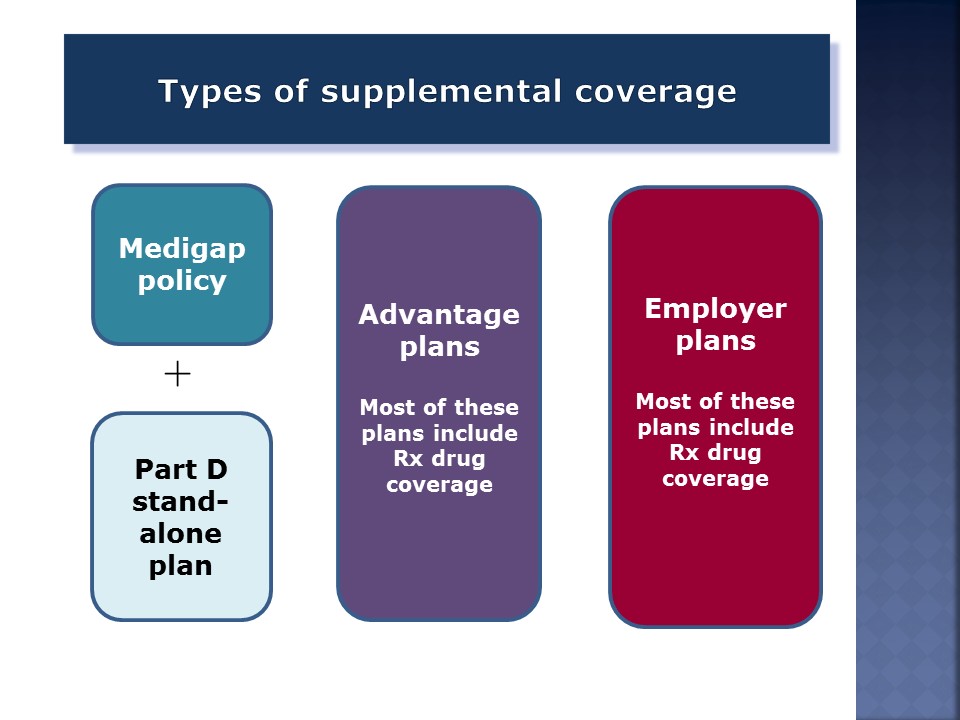

Type of supplemental coverage

Your clients will have one of these three types of coverage.

One is a Medigap policy which does not cover prescription drugs, so you have to get a Part B standalone plan. These policies, because they are expensive, have shrunk as a percentage of the Medicare population. The penetration rate is smaller than it used to be. It’s probably about 17 percent today.

Advantage Plans have more than taken up the slack. By the end of this year, probably one-third of everybody in Medicare will be in an Advantage Plan. These are managed care plans. They are HMOs, for the most part, and some PPOs. Most of them include drug coverage. If you enroll in a plan that does not, then you have to enroll in a Part B standalone plan as well.

Employer plans are the best kind of coverage, from a cost perspective, because the employer is paying a portion of the premium. Most plans include prescription drug coverage that’s uniform across all plan options. Employer plans can include Medigap policies; they’ll take a Medigap policy and subsidize it. They might add benefits to it. They can also include Advantage Plans.

As people age, they’re less inclined to do the things necessary to see if they’re still in a good policy. If their Medigap policy premiums have been increasing at 3, 4, or 5 percent rates, that’s to be expected. If they have been seeing larger-than-usual increases, they might want to see if they can switch to a different insurance company that has lower premiums. They may not be able to do that if they have health problems. They’re going to have to undergo underwriting. Medigap still has that provision in most states.

There are eight states that have some protections for people who want to switch insurance companies, but in the other 42 states, they will have to answer health questions or usually a series of yes-or-no questions about their health. They’ll also check their drugs to see what drugs they’re taking, and then they’ll either charge them higher premiums or, in some unusual cases, may decline coverage.

The dilemma in choosing coverage for many people is, “Do I take a very expensive Medigap policy that I know is going to cost me $100,000 or so if I live to be 90, or do I take an Advantage Plan now, which will cut my costs, but then run the risk later, in these 42 states, of not being able to get a policy while, at the same time, starting to see a lot of doctors and needing more treatments? I have to remain in a managed care plan where it’s very hard to find networks that include my doctors, and the prior approvals are a burden.”

What to look for to match coverage to needs

What every person with a Medigap policy should do is check their Part B standalone plan every year. These plans change formularies year to year. It’s just amazing. This is the most volatile type of coverage, not only in the Medicare universe but maybe in all of this country’s healthcare system. It’s just unbelievable.

The Kaiser Family Foundation has done a lot of research on this. 80 percent of the plans that are the lowest-cost plans for a given set of drugs in one year will not be the lowest cost plans the next year, and the average cost difference is several hundred dollars.

This is easily measured in terms of seeing if you’re in the lowest drug plan because you can list your drugs, dosages, and frequencies, and say, “What’s the lowest-cost plan?” and see if you’re in it. 85 to 90 percent of the people in Part B standalone plans are paying too much because they don’t reevaluate their coverage, but it only takes a phone call.

When you find the lowest-cost plan, there are a couple of other things you might look for which will perhaps save some money. There are two refill schedules: monthly refills at the local pharmacy, and mail order. Sometimes, and it varies a lot by plan, one or the other turns out to be much less expensive.

Then, the other thing that can sometimes save money is that some plans, not all, have what they call “preferred pharmacies.” If you are getting local retail refills, then you might want to ask your plan, and you don’t have to wait until Open Enrollment to do this, if your plan has preferred pharmacies. I saw a case just last month whereby walking across the street from a CVS to a Walgreens, somebody could save about $250 a year because the Walgreens was a preferred pharmacy in that particular plan and CVS was not.

So, the bottom line is that if you had to check one thing here, it would be Part D coverage.

With Advantage Plans or managed care plans, you’re really turning over your entire care when you join one of these plans. Now, the plans have to follow Medicare’s basic coverage rules, but what that means is that your benefits are assigned to the Advantage Plan and they take control of your coverage. You live by their plan rules. They have to meet Medicare’s certain requirements, but you want to be fairly careful in choosing an Advantage Plan that you’ve looked at several things.

It’s not feasible, though, for retirees to go in and look at a long list of things to see if this is the best Advantage Plan. It just won’t happen. So, if you looked at two things, the first would be our friend, prescription drug costs, and the second would be out-of-network costs. Even in PPOs where there’s some coverage out of network, it’s not like most employer PPOs where the out-of-network costs are 20 or 25 percent. Many Advantage PPO plans have 40 percent, and I’ve seen 50 percent costs when you go out of network. So, this can be a big cost driver.

The other thing you might look at is Medicare’s overall quality rating for the plan. Medicare has a five-star quality rating. Plans are rated on about 50 criteria; the number changes a little from year to year. Plans that have four stars are better and get bonuses, and a plan with a lot of members can get tens of millions of dollars in bonuses in a year. By law, those bonuses must be reinvested in benefits for plan participants. So, it’s a virtuous circle in the sense that plan get better by doing better, and as they get better ratings, they get more money, which they reinvest in better benefits, which in turn attracts more enrollees. If you can find a four-star-or-higher plan, you probably are going to get additional benefits in that plan, like maybe some dental and vision.

Employer plans come in all shapes and sizes. It’s kind of hard to generalize on these. The good thing about employer plans is that they are group plans that you can move about from year to year. I’m retired. I have eight options in my retiree plan, ranging from very comprehensive to managed care plans that are not comprehensive at all. Premiums are much higher for the comprehensive plan, understandably. The drug coverage is the same for all of them, so I don’t need to check that in my plan; that may not be the case in all employer plans, since there are so many different kinds.

The nicest feature, I think, of these plans is that you can move about without going through underwriting. So, you’d look and say, “Does my coverage match my need?” If you’re in good health, as we said earlier, consider a less comprehensive option. You can always move up the ladder, maybe during the next enrollment period.

There’s a subset of employer plans which is a fast-growing trend, and the rules don’t apply quite as much here. They’re called Medicare private exchanges, and instead of administering the plan, the employer gives an amount to the exchange to be invested on your behalf. It’s a health reimbursement arrangement, so there’s no tax consequence for you, but you have to buy your coverage through the private exchange. The average, one survey showed, was about $175 a month. So, your former employer contributes $175 a month to a private exchange, and you can spend that, and then you pay the difference, depending on the coverage.

In these plans, you will have to undergo underwriting for Medigap policies. They have Medigap policies in them, but when your employer transfers you to the private exchange, you get a one-time special enrollment period to get a Medigap policy without underwriting. This is the emerging trend, and it’s still better than not having an employer plan.

Private exchanges don’t always offer as many options as a regular Medicare menu would. Also, they’re not administered by the employer. They’re administered by the exchange, and the exchange makes its money on commissions. The employer does not pay the exchange. They just transfer the employees to them and say, “You make your money on commissions as you place people in Medigap policies, Part B plans, and Advantage Plans.” The good news is that you can call them every year during Open Enrollment, and they have to do an evaluation of your lowest-cost options for drug coverage and others.

Where can our clients get no-cost help?

This would be, in most cases, during Open Enrollment. These lines are all busy, so call early.

- 800-MEDICARE. When I was a volunteer counselor, we used to tell people to call in the after-hours, maybe late at night, just to get through. That’s the downside of 800-MEDICARE. This is a 24/7 line. They will do drug plan searches. They’ll tell you the lowest cost plan for your drugs and compare it to the plan you’re in. Then, unique among the phone numbers that we’ll see, this number will also automatically transfer you to the plan you want to go in, if you want to switch plans.They will do the same for Advantage Plans. They will identify the premiums and costs, compare them to the plan that you’re in, and then they will enroll you in that new plan, if you want to switch, effective January 1st of the following year.

- Medicare counseling agencies. Every state has one, and in many states, every county has one. I work for LA County. You can find your local one at this web address (shiptacenter.org). These people are good with Medigap policies because Medigap rules vary slightly among states, and they won’t know that at 800-MEDICARE. These people are very busy during Open Enrollment, so it’s good to call them early and make an appointment.

- The Medicare Rights Center. This is a 9 am – 5 pm New York-based national help line. They also are busy during Open Enrollment. These are volunteers, for the most part. They’re less helpful on Medigap policies, except for national rules.

- Do-it-yourself. A lot of computer-literate people can do their own Part B searches. We have instructions on our website about how to do it. If they’re patient and willing to take 15 or 20 minutes, or maybe 30 minutes the first time, they can go on and do everything.

This once-a-year exercise of reviewing your coverage and switching when you see substantial savings will save people money. In our business, the people we see are the people who frequently are in their 80s. They come to us, and they have not done anything, and they know they need to do something. Just this last enrollment period, we had a couple who will save $3,500 this year, compared to what they would have paid had they stayed in their other plan.

The Third Step: Coach Clients to Track Costs

The third step in our ways to help is the one that in some ways is not as important. It’s just to track costs, which is fairly easy to do.

They add their premiums to their cost-sharing. They can call their insurance company and ask, “How much have I spent out of pocket this year?” Add that to their premiums. Add their Part B premiums. My insurance company for my employer plan will tell me how much I spent last year for drugs. That’s a call.

How fast their costs are growing if they’ve allocated a certain portion of their retirement costs to healthcare – are they growing at 4 percent, 5 percent, or 8 percent? I think this is less important for some people if they do Step No. 2, and estimates are fine.

Takeaways

- Help retirees understand that most of the cost is going to be in later retirement.

- The most important thing they can do, and maybe the only thing they can do, is reexamine their coverage each year. Particularly early in retirement, it’s good to try to give some thought to the long-term implications, “Can I afford a $100,000 Medigap Plan F if I live to be 90?” If they can, fine.

- There are many non-profit agencies to help retirees review their coverage yearly. What we do is provide evaluations, primarily for people who are entering Medicare for the first time; we also do it for people who are already in. You can go to our website and then to our Services page. At the bottom, there’s a link to a sample evaluation.

About David Armes:

David Armes, CFP®, is Principal of Dover Healthcare Planning, LLC, a fee-only firm that assists clients in evaluating their Medicare options. Prior to starting the firm, David served for four years as a volunteer Medicare counselor after retiring from his job as real estate division manager for a large corporation.

David is the author of several published articles about managing retirement health care costs, including the cover story of the October 2017 issue of the Journal of Financial Planning.

Are you looking for a retirement speaker for your next conference, consumer event or internal professional development program? Visit the Retirement Speakers Bureau to find leading retirement industry speakers, authors, trainers and professional development experts who can address your audience’s needs and budget.

©2017, David Armes, CFP®, Principal of Dover Healthcare Planning, LLC. All rights reserved. Used with permission.