Editor’s note: This article is an adaptation of the live webinar delivered by Phil Bongiorno in 2019. His comments have been edited for clarity and length.

You can read the summary article here as part of the 2nd Qtr 2019 Retirement InSight and Trends Newsletter, worth 1.0 CE when read in its entirety (after passing the online quiz.)

You may also choose to take the full length course “The Value of Safe Home Care for 1.0 hour continuing education (CE) credit.

By Phil Bongiorno, Executive Director at Home Care Association of America

The number of families utilizing home care services continues to grow in the United States. A higher number of family caregivers who are caring for a loved one with a chronic or debilitating health condition are turning to home care, rather than institutional care, for their long-term care needs. Many cite the desire for a higher quality of life and independence as the reasons for the choice of care at home. Most of this care is paid for using available disposable income.

Faced with a bewildering number of choices, family caregivers more and more are turning to companies that offer them the least expensive price for care without understanding the implications of their choice. Many are hiring workers from entities that do not employ or supervise their workers but merely “place” them in home care settings.

This article will provide ways to help you understand the differences in home care service models, reinforce the value of quality home care with your respective clients and assist in determining quality and value of home care providers.

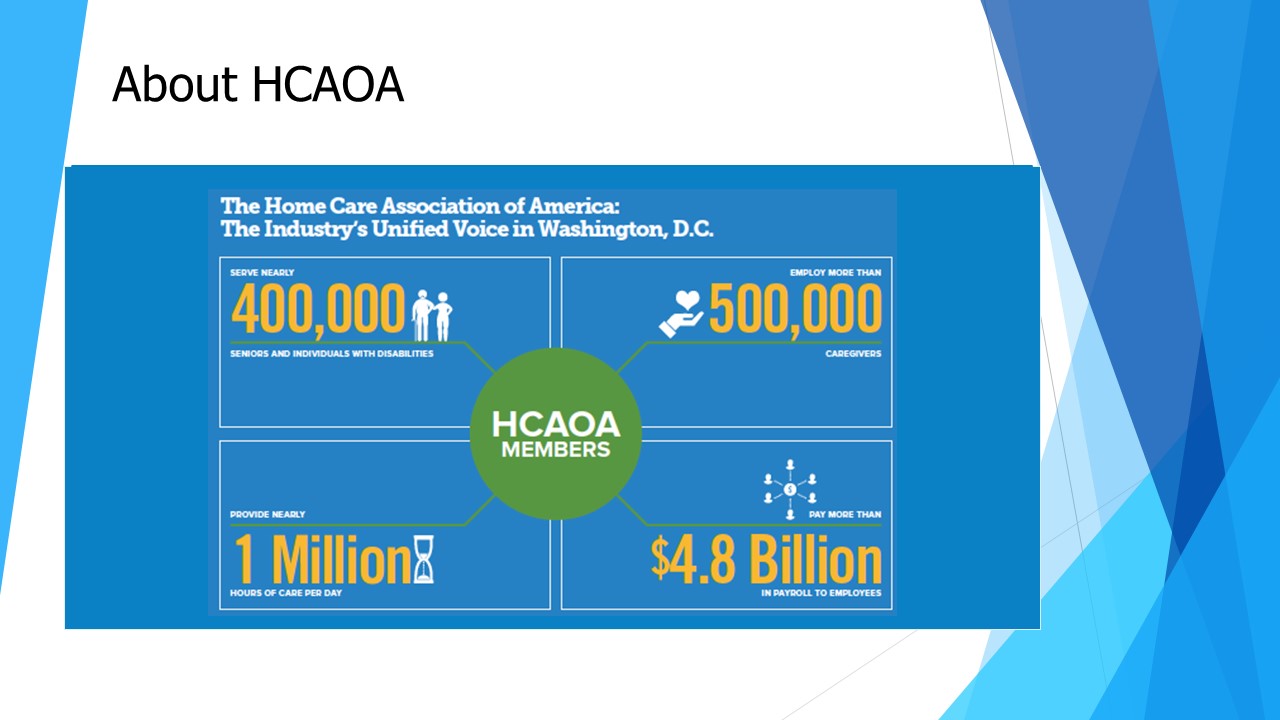

Who is the Home Care Association of America?

The Home Care Association of America represents homecare providers. We mostly provide what’s considered in-home personal care services supporting activities of daily living. Traditionally this has been called private duty care. Our organization started as the National Private Duty Association. We changed our name about six years ago to the Homecare Association of America.

Homecare is different from home health, and there are distinctions from home health depending on how it’s paid. Our association serves nearly 400,000 seniors and people with disabilities. We employ about half a million caregivers around the country. We have about 3,000 member providers that are providing close to a million hours of care per day, and we have a footprint of about $4.8 billion in the economy.

We believe that people should be able to age safely in place at home and remain active in their community to the extent possible according to their desires. We champion advocacy measures at both the federal and state levels that promote home care quality and cost-effective, affordable care. We advocate that appropriateness of care and client protection is best provided in an employee-based model.

A couple of years ago, we published the report, “Caring for America’s Seniors: The Value of Homecare.” We are not home health – there’s a distinction – so we decided to develop this industry report to establish the concept of homecare, what we do, and what our industry does.

This report is a meta-analysis of existing data; it’s not original research. It was a partnership between our organization and a group called the Global Coalition on Aging, which is made up of high-level corporations that have an interest in aging, both for their customers and for their employees, and it clearly defines our industry and demonstrates the benefits of homecare.

For seniors in the home, we’re helping prevent falls. Falls are one of the leading causes of injury and death to seniors. We’re helping keep seniors healthy and helping them keep their medication regiment on track for reminders. We’re providing companionship to them. Many people don’t know that senior isolation is one of the leading causes of mortality in this country. We’re in the home with the seniors helping them with activities of daily living to make sure they’re healthy and living a quality life in the home.

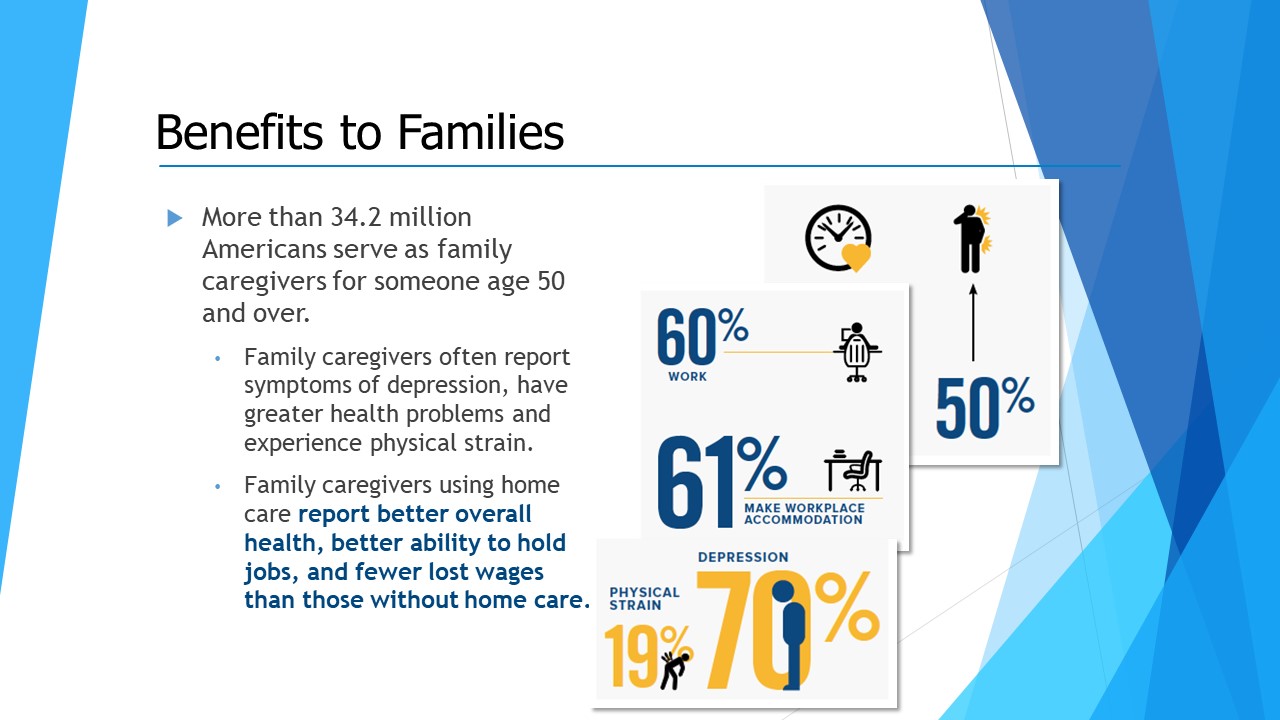

Over 34 million Americans serve as family caregivers for someone over age 50, and that statistic has certainly gone up in the last couple of years.

How can we pay for caregiving today?

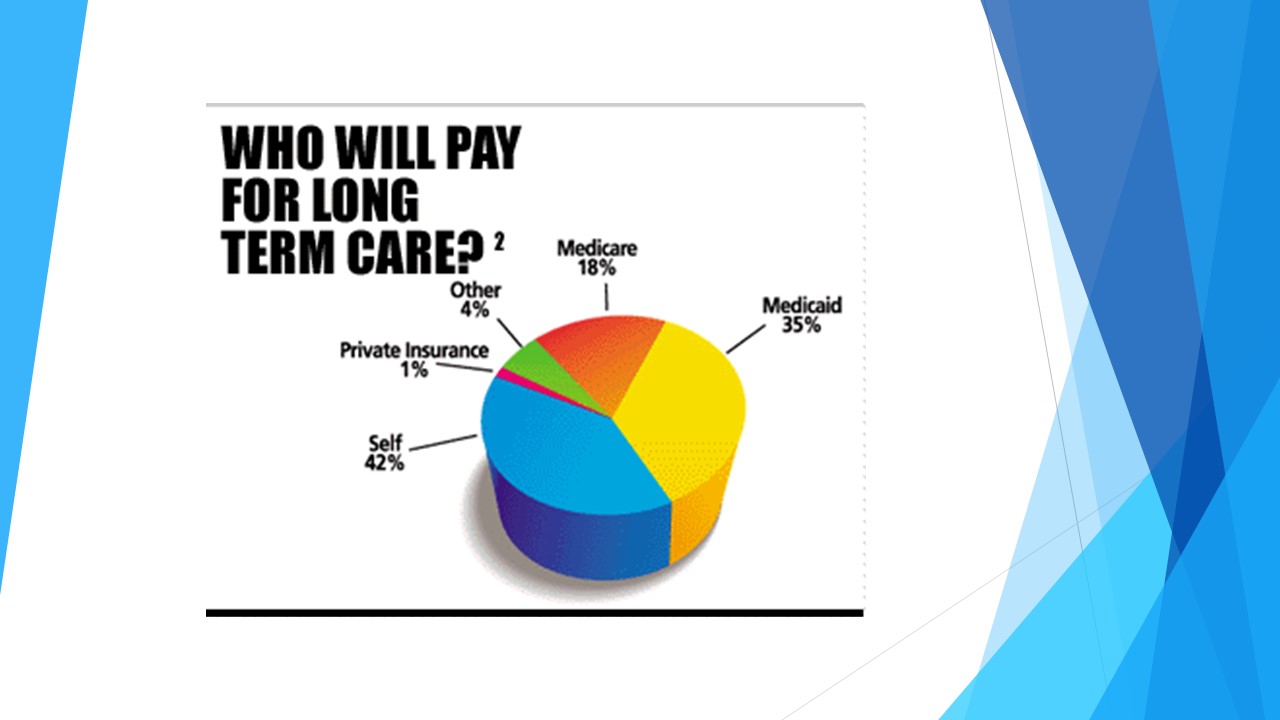

Right now, most of our care is paid for out of pocket. As you can see, government-financed care is primarily going to nursing homes, to home health services, and only a small percentage to home care services, and that’s primarily for veterans and the Medicaid program.

Data shows that by having someone in the home taking care of a senior, we help reduce healthcare costs in the form of readmissions, in the form of fewer doctor visits, and to relieve government health programs from some of the strain they have when it comes to the projected cost to those systems.

What is the plan to pay for healthcare? Right now, a lot of what we do is considered private pay or out of pocket, and in this statistic, you’ll see that long-term care services are mostly coming out of individuals. There is some coverage from Medicaid and Medicare, and I’ll talk about some of the government programs, but it’s something that is very important for all of you to understand how you can help your clients with this question.

Right now, some programs like Medicaid – you have to qualify, of course – will provide programs under what’s called the home- and community-based services waiver. Many of the Medicaid programs have this service in place, where it pays for home care services, but you have to qualify in the Medicaid program.

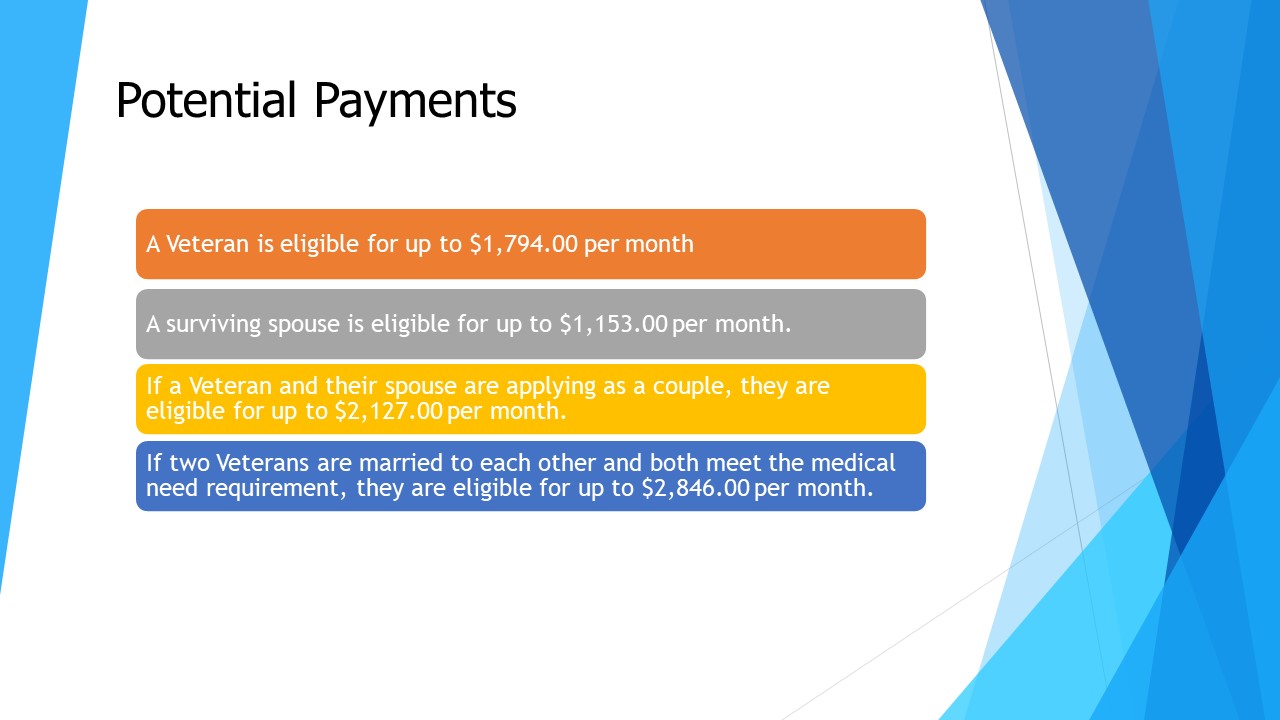

There are veterans’ programs as well that will provide veterans services, and what’s called the aid and attendance benefit, where you would have to qualify as a veteran and meet other requirements from the Veteran’s Administration (VA) to receive these services and have homecare reimbursed under this program.

Some changes are happening with the VA right now. We’ve had delays in payments from the VA to our members of three to six months, so it’s a challenge for some of our members to participate in this program because of the VA’s administration of this. We’re working with the VA to make some changes on how we can cut some of the red tape so that veterans can receive these services.

Other financing options include reverse mortgages, hybrid life insurance plans, annuities We look at other options as well – for example, the Medicare Advantage program. Many may not know this, but that program is growing. You have the traditional Medicare program where beneficiaries participate. You also have Medicare Advantage (MA), which is the managed care program of Medicare, and right now under the Chronic Care Act that passed a few years ago, the Centers for Medicare and Medicaid Services, or CMS.

The Center for Medicare and Medicaid Services allows for the Medicare Advantage or MA Plans to cover home care services. This is a new development in what was considered health-related services. Home care is still not considered a health service, but CMS is looking at what we’re calling social determinants of health, so in addition to home care, they’re looking at other services like meal delivery, home modifications, and that sort of thing. We’re working with these MA plans to establish appropriate reimbursement, so stay tuned for that. You’ll probably see more of that be promoted by the MA plans out there.

Another exciting opportunity is with health savings accounts (HSAs). We are working with Congress on the potential of allowing home care services to be an allowable expense. Unlike the flexible spending accounts, as you probably know, HSAs can be rolled over from year to year, so this is an excellent opportunity for folks that are investing and saving in HSAs to use that to cover home care services potentially.

Home Care Association of America (HCAOA) Public Policy Objectives

Another way to pay for home care services in the future is with tax credits. We’ve supported a bill called the Credit for Caring Bill, and it’s bipartisan. It’s interesting – we have everyone from a very conservative Republican from Iowa to Elizabeth Warren from Massachusetts – you can’t be further apart on the spectrum than these two individuals – that are supporting this bill to look at tax credits and how they can be used for home care services.

Tax credits for home modification are also in legislation that’s is proposed in Congress that will help offset home modification costs for families that are making changes like ramps and other accessibility modifications in the home to help seniors age in place.

CAPABLE is a program developed at the Johns Hopkins School of Nursing for low-income seniors to safely age in place. The approach teams a nurse, an occupational therapist, and a handyman to address both the home environment and uses the strengths of the older adults themselves to improve safety and independence. Recently the grant program at Johns Hopkins Baltimore hospital invested anywhere from $1,000 to $2,000 in home modifications for their Medicaid population, and they found that by combining home modifications with homecare, they saved a lot of money in readmissions and other healthcare costs.

At the state level, we support state licensure for homecare providers. Unfortunately, not every state has licensure for the services we provide. It’s interesting – you need a license in every state to catch a trout, but you don’t need a license in every state to take care of a senior or bath a senior. It’s interesting that we still have many states that have not licensed this service.

We support hospital discharge and referral legislation. This is legislation that points to hospitals to make sure they are referring properly to home care providers that are licensed.

We also support consumer protection disclosure legislation for placement registries. This legislation requires placement agencies to make sure families understand the type of model and relationship that they have with the caregiver, and that they often have responsibilities.

The Affordability of Home Care

One of the other things we’re working on is the affordability of care. Fifty-three percent said that affordability of care was a significant factor in why employees left their jobs, an others mentioned the inability to find trustworthy help and the inability for them to meet their work responsibilities as a result.

The National Academies of Sciences published a report, “Families Caring for an Aging America,” which examined the state of family caregiving and looked at the impact on caregivers’ health, their economic security, and overall wellbeing. It identified ways we can design interventions to support family caregivers. This report concluded that there are recommendations for developing a national strategy to help family caregivers.

The RAISE Act is a bill that directs the Department of Health and Human Services – HHS – to develop a national family caregiving strategy. They’ve already begun the process of convening a family caregiving advisory council to advise on this issue, so that’s happening right now. There’s a recognition by industry, government, and academia to look at how we can support family caregivers.

When you need to pay for home care, it creates an environment with no formal standards, no oversight, and in some cases, no criterion for business ethics, and that’s a concern we have, particularly in states where there’s no licensure.

As a result, there’s a variety of home care providers that deliver their services in various models when they provide those services, and the consumer has been and continues to be vulnerable, and it impacts our industry representing homecare providers.

What are some of the homecare regulation standards? This takes the form of no licensing requirements governing home care providers in some states, no regulations governing essential matters such as practices for the hiring and training of caregivers, and no regulations regarding care supervision or quality control practices of homecare services. This is all in states where there is no currently existing licensure.

Accountable homecare does things a little differently. HCOA sets and defines industry standards in the absence of a formal regulatory environment, so even in states where we do not have licensure, we have members who are operating under our standards.

There are two different models of homecare services delivery. The first is where the home care provider has an employer/employee model, and the second is what we call domestic referral agencies or independent contracting, which is often called the “domestic registry model.”

Under our first model, the employer model, you have a provider that is generally bonded and insured, offers comprehensive orientation with in-depth caregiver training, takes care of any legal issues that occur should the caregiver or client be injured in the job, and provides ongoing supervision. This is a significant distinction, and I’ll get into some of the Department of Labor requirements when it comes to determining who is an employee versus an independent contractor because there was recent guidance specific to home care.

The employer-model provider has a staff pool to call upon to quickly find a replacement for backup care. They always do an employment reference check, a background check for abuse and neglect, criminal background checks, and in some states, we’re supporting doing fingerprinting as well. They have pre-employment testing, like drug testing, in most states, and the employer also does skills assessment testing.

In addition to that, there’s requiring proof of certain certifications that would include things like whether the caregiver is TB-tested, whether they’re certified in CPR or first aid, any license – in our case, we have what’s called a CNA or Certified Nursing Assistant, which many of our caregivers carry as a credential.

Our members also have proof of whether the caregivers have a sound driver’s license. Driving services are often required, and many homecare companies allow their caregivers to drive the client to doctor’s appointments and other social activities.

Many of our members are embracing technology. They are investing in and working with companies for fall detection, medication reminders. Siri and Alexa have a lot of that kind of smart technology happening in the home already, so some of our members are taking advantage of that to assist in their caregiving needs. EVV – electronic visit verification – is also a technology that helps our companies make sure that the caregiver is reporting in when they said they were going to report, and that they’re where they should be when it comes to the client.

Wearables are a technology that are often embedded into clothing, whether it’s anything that goes around the neck like neckwear that allows for individuals to make sure we know where the client is, especially for someone who might be experiencing dementia who might wander. If they go out of a certain room or catchment area, there would be an alarm that makes sure individuals know where they are.

The other home care business model is a “Registered and Independent Contracting Model.” These are generally agencies or organizations that help families locate a caregiver and place one in a client’s home on an independent-contractor basis. Registries do not serve as an employer, nor can they take responsibility for supervision. If they did that, they would lose their designation as an independent contracting placement agency.

Because caregivers are independent contractors, they’re lower in cost, as there’s little or no overhead in the way of training, benefits, workers’ comp, and that sort of thing. The client is liable for payroll taxes and possible work-related injuries of the caregiver as part of this model, so basically, the family is directly responsible as the employer of the caregiver in this case, and often they’re not made aware of that.

Many of you might be aware of the distinctions between employees and independent contractors. The Department of Labor published a field assistance bulletin in late 2018 that specifically addresses Registries in homecare. The DOL’s guidance said that is a Registry is one that does not plan and provide care for the client, but might seek information concerning the type of care the client needs for matching purposes and looks at how the work is controlled. The caregiver may not receive any instruction from the Registry about how to care for clients. They can’t instruct caregivers how to provide caregiving services, monitor or supervise caregivers in clients’ homes, or even do a simple performance evaluation.

If they do any of these services, which we see as a quality standard in home care, they will trigger themselves as an employer, and they do not want to have that designation. They want to maintain their placement agency or independent contracting status. The Department of Labor has recognized that the absence of such control indicates that the Registry is not an employer of the caregiver. To maintain that status, they’re not providing a quality service to their families, which is why we see a distinction in this care as a standard for our industry.

You’ll see that with the Registry, the cost is generally 10-20 percent lower. However, you should be aware that there are hidden costs that are not reflected in this percentage that clients don’t often consider. It’s the fact that they have responsibility for tax liability, they usually have to look at they’ll need to pay workers’ compensation insurance costs to go along with that. Homeowner’s insurance will generally not cover a worker’s injury in the home, and they will likely need to get a rider. Looking at it in total, it’s not much less expensive when you include these other costs.

What Should Your Clients Be Asking Prospective Homecare Providers?

We recommend that families question prospective home care providers with the following questions:

- How do you recruit your caregivers?

- Should a scheduling conflict occur, are there trained backup caregivers that are available? Frequently, when you have a Registry model, the family is placed with just one caregiver, and that’s the only one. If that individual is sick and cannot come to the home, what happens then? If that Registry is then directing another caregiver to the home, then they may not be a Registry. They potentially trigger an employment relationship.

- Are the caregivers bonded and insured? Many times, we don’t necessarily have that reliability with certain placement agencies.

- Are the caregivers employees of the provider? Again, it goes to whether there’s oversight.

- Does the provider handle the payroll and required taxes of the caregiver?

- Is there a criminal background check and a check for references for each of the direct care staff?

- Does the provider follow and/or execute a plan of care? That’s another distinction of our members. As part of our intake with clients, we’re making sure that we’re part of a plan of care from a healthcare provider or help to develop a plan of care when it comes to what the specific needs are of the client.

- If they’re experiencing a specific medical condition, what are some of the homecare needs that they will specifically have as part of their service?

- Does the provider perform periodic visits for each of their clients? Again, as an employer, that’s a standard. We would certainly do oversight and supervision. As a placement agency, if they begin doing that, they would have the potential of losing their distinction as an independent contracting agency versus an employer, so you’re not likely to see that happening with those agencies.

- Does the provider conduct caregiver training and supervision? Supervision of care is a clear distinction between what employers do and what independent contracting agencies do.

What Are Key Takeaways for Advisors?

Look at and take care to advise your clients on the distinctions and the quality and convenience reflected in the different home care service delivery models that we’ve covered here. Incorporate the checklist above to screen prospective homecare providers as a resource for your clients and their families.

Become more knowledgeable on the policy developments. I mentioned the tax credit bills and the opportunities we have in both the health savings account and the Medicare advantage programs. Be aware of what’s happening that could help you advise your clients on what their financial planning would look like if they were to take advantage of some of these programs if they become law.

We welcome you to network with the home care providers in your community as a resource to you and your clients, and also take advantage of the resources that we have from HCOA in promoting safe, quality home care services.

Visit our “Safe Home Care Initiative” website. Some of the things that I’ve addressed here are encapsulated on this website so that it can be a resource not only to families that are considering home care, but also professionals like you who are servicing seniors and their families.

We also have an individual professional associate membership category that financial planners can utilize. If you have an interest in home care and want to keep tabs on what’s happening in home care, we welcome you to be part of that.

About Phil Bongiorno, Executive Director at Home Care Association of America

With more than 25 years of extensive health care and public health policy experience, Phil has represented numerous associations focused on health care and disability issues over the years.

He began his role in January 2014 as Executive Director for the Home Care Association of America (HCAOA), a trade association representing nearly 3,000 home care providers across the United States. Phil is responsible for the Association’s overall operations, including strategic planning, financial management, membership development, education, advocacy and public affairs.

In his spare time, Phil is a long distance runner and has completed the Marine Corps Marathon 17 times.

Are you looking for a retirement speaker for your next conference, consumer event or internal professional development program? Visit the Retirement Speakers Bureau to find leading retirement industry speakers, authors, trainers and professional development experts who can address your audience’s needs and budget.

©2019, Phil Bongiorno, Executive Director at Home Care Association of America. All rights reserved. Used with permission.