By Nyal Bischoff, Independent Long Term Care Specialist

Editor’s note:

This presentation was delivered in live webinar format in 2015. Nyal’s comments have been edited for clarity and length.

You can view a YouTube brief of the original presentation here.

You may also choose to take the full length course and earn 1 CRC®, CFP®, and/or PACE CE credit.

Some of you may recall that just a few years back right around Christmastime there was a huge tsunami in Malaysia and Indonesia that caused enormous damage and hundreds of thousands of lives, literally. In looking at this huge baby boom population the question might become: where do you want to be if that tsunami hits? Do you want to be on top of that wave or on the bottom getting swept away?

I can remember watching Dragnet many years ago. Sergeant Joe Friday had a saying that he immortalized and made famous. He would always say, “Just the facts, ma’am – just the facts.” So here are some key facts about long-term care:

- Two-thirds of individual long-term care claims start with folks at age 80 or older.

- 70 percent of the people that are over 65 are going to need some form of care before they leave this world.

- A little bit more than half of Baby Boomers believe that Medicare would cover their long-term care.

- 47 percent of the adults in their 40s and 50s have a parent 65 years of age or older now.

- 21 percent of boomers right now provide financial support for a parent who is 65 years of age or older.

- Of the nine Baby Boomer retirement regrets, understanding life expectancy was number eight and last, but not least, number nine was not planning for long-term care expenses.

A lot of people ask me what was the number one regret of Baby Boomers? Their number one regret is lack of savings and an unrealistic understanding of how much will be needed in retirement. Their number four regret – this is another important one – was withdrawing money from tax-deferred IRAs too early.

These are critical issues that we’ll come back to.

The Costs of Long-term Care

With the probability of these facts, let’s look at what care costs are today. The median nursing home costs in the state of Michigan, where I’m from, are just under $100,000 a year to be in a private room. If you multiply that times what Kiplinger Magazine declares as the average stay in a facility, which is 2.4 years, today’s average cost hovers just a little bit under $250,000 if someone winds up in a nursing home. By the way, that does not include time that may have first been spent getting care at home and/or in an assisted living facility.

Now, let’s look at future costs. Let’s take that average 2.4 year stay, multiply it times a 4.2 percent inflation factor, take today’s average age applicant for long-term care insurance, which is 57, and project that out 25 years. This cost that today is $237,000 will hover over $600,000 by the time they get to what is called cluster age in our industry. That’s a pretty scary number. This future cost however is very often dismissed.

Now let’s talk about the big issue here, the hidden costs. Too often we have folks that don’t understand what comes along with the issues of aging. Nearly 60 percent of the people who care for Alzheimer’s and senility folks wind up having huge issues with emotional stress as a result of that caregiving. Fully one-third of them report depression. Unfortunately what is rarely talked about are the consequences to the spouse and the family, which by the way are the first line of defense when this issue arises. Folks don’t have a strategy for what happens when care is needed and very often the family takes the brunt of that abuse.

There’s a saying in our business that caregiving does not bring families together. It tears them apart. This hidden cost frankly is every bit as difficult to cope with as the financial cost. It’s like a one-two punch. It’s bad enough that you wind up needing care unexpectedly. The only thing worse is having to pay for it.

With this high cost and the high probability of folks needing care, why do you suppose people haven’t made plans or taken this issue into consideration? It’s called denial. Let’s go what denial sounds like when you’re having a conversation with folks about this topic.

- “It won’t happen to me.” My response might be; are you prepared to risk everything you are worth in case it does happen?

- “We’re heart attack people.” That’s the good news. The bad news is most people who suffer from heart attacks go on to an emergency room and live with subsequent stents or bypass surgery and ironically live many, many more years than they would have had they not had that heart attack.

- “My parents died quickly.” The road to needing care is paved, literally paved, with tens of thousands of people whose parents died quickly and they thought they were going to get the same wish as their parents.

- “I’ve heard this costs a fortune.” They think they’re talking about the costs for the protection. No, this does cost a fortune. In fact, the cost in Michigan is about $100,000 a year. You need to get them thinking about what the cost is of not having coverage.

- “My kids will take care of me.” Which one would be the first to put their lives and their job and their career on hold, board a plane and fly halfway across the country to take care of you? Not many people want that to happen.

- “I’m in great health right now.” I stole this saying from my doctor; my doctor says we’re all healthy until the day we’re not and the day we’re not healthy the rules change.

- “I’m a veteran; I’ve got VA benefits.” You need to understand that if you’re a veteran it’s no different from private pay. If you have assets you must pay for your care with those assets and only when you’re out of money do you qualify for any benefits.

- “I need to pray about this.” Who do you think sent me?

- “I have enough money. I can self-insure.” That’s the very exact reason why we need to talk about this, because the bottom line folks are focused on the wrong issue (called denial).

Health Changes are Equal Opportunity Offenders

Health changes cross both genders, all races, and every possible life status you can imagine. Let’s talk about some notable people with various diseases.

Multiple sclerosis: The first one that comes to mind is Annette Funicello, who was in the Mickey Mouse Club when we grew up. She was diagnosed with multiple sclerosis in her 40s. The point here is getting old isn’t the key to needing care. You can have the misfortune of having a diagnosis of one of these things that can cause a huge financial and emotional life change for you. Richard Pryor, a comedian, also had multiple sclerosis.

Lou Gehrig’s disease (ALS): The most notable one there is Stephen Hawking, theoretical physicist, probably the greatest scientific mind in our generation since Albert Einstein. Stephen Hawking was diagnosed with MS at age 21. Here is an astonishing fact about Stephen Hawking: he has required 24-7 care since 1985. Put a pencil to what kind of cost that must be.

Huntington’s disease: Woody Guthrie, Arlo Guthrie’s father – a folk singer – had Huntington’s disease.

Parkinson’s disease: here locally in Michigan, Mohammad Ali – a/k/a Cassius Clay – from Muskegon, was diagnosed at age 42 in 1984 with Parkinson’s disease. The Reverend Billy Graham was diagnosed at age 70 in 1992, and Michael J. Fox, actor, was diagnosed at age 30 in 1998.

Alzheimer’s disease: Probably the most famous one is Ronald Reagan, former president. Here in Detroit, Rosa Parks and Charlton Heston, actor. Glen Campbell was diagnosed with Alzheimer’s disease. Women are probably almost twice as likely to get Alzheimer’s disease as to get breast cancer and that’s a fact right out of the Alzheimer’s Association.

Strokes: A lot of people think that if you have a stroke you’re going to die quickly and certainly we can bring people to mind where that has happened, like Franklin D. Rosevelt and Winston Churchill. Kirk Douglas wound up having a stroke and his good fortune was he lived to talk about it and went on to even be able to act in some movies; so a stroke doesn’t necessarily end your life.

Accidents. Christopher Reeve is the easiest one that comes to mind: a horseback riding accident. Again, the key issue with health change is you cannot control what happens and if it happens, there’s going to be a huge issue as it relates to what it can do to people financially and emotionally.

On the accident side I can remember years ago in my early career I met a family. The gentleman had just retired. He had been in retirement for six months. He was working one afternoon in the ceiling of his garage rearranging some insulation, fell through, sustained a head injury and is a paraplegic. Anything can happen at any age and that gives folks pause to think about what can happen.

Aging and Healthcare Risks

As we get older things begin to change. Do you weigh the same amount today that you did when you graduated either from high school or college or when you got married? As you get a little older, in your 30s and 40s pretty soon that weight gain causes the doctor to sound the alarm bells because your cholesterol levels are up so you go on a cholesterol pill and a high blood pressure pill comes along.

For men, we have something called BPH, Benign Prostate Hypertrophy, called an enlarged prostate. Women on that same order get osteopenia which sometimes can lead to osteoporosis, the thinning of the bones, fractures and issues as such. Then the parts don’t work like they used to. We need to get the hips or the knees replaced. At some point we get an elevated A1C reading with the doctor and now we get onto a pre-diabetic medication or a diabetic medication. Folks with diabetes have multiple incidents of TIA, transient ischemic attack, or strokes. Ultimately memory loss occurs.

When you ask people what would happen if one of these events were to occur, guess what the normal response is? Well, I hope it won’t happen to me. Hope is not a strategy and this can be a very, very important issue to take charge of while you’re in good health and have a strategy to manage that.

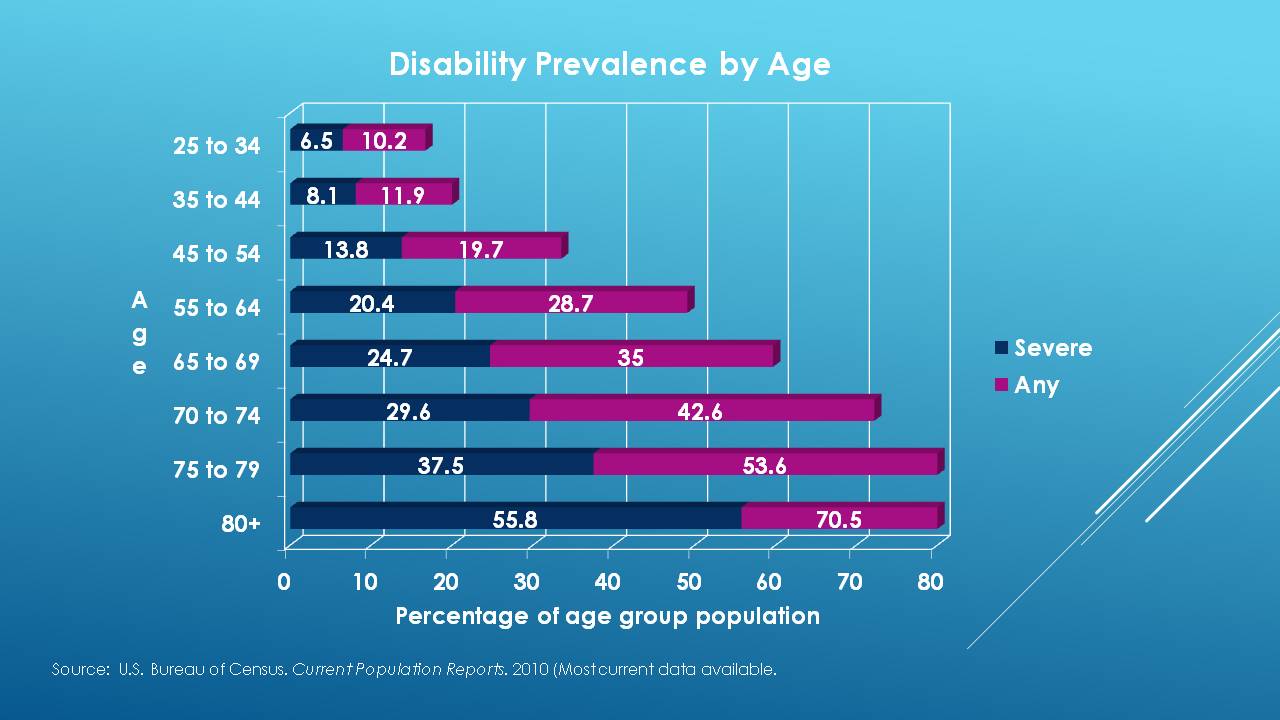

Below you see that of those 80 years of age or older, already half of them – more than half – have a severe disability, and another graph with the type of care needed. You also don’t want to not pay attention to what’s going on with younger clients because you don’t have to wait until you become old to need care.

What are the Options for Addressing Long Term Care Risk?

Only 30 percent of your clients have a pension. This should be a red flag. There’s a huge amount of risk involved if the amount they’re paying for long-term care will be at full retail plus their tax bracket. This turns out to be an emotional and financial wreck.

There are solutions to all of this:

- You can have health insurance, which we know only covers short-term acute care.

- Medicare only pays for a maximum of 100 days.

- You have to be broke to be on Medicaid.

- Your personal savings and assets are at risk and most of the time the personal savings that are used wind up being 401(k) money

- The last option is to transfer the risk.

What would your response be if 25 years from now an $800,000 loss could stare you in the face? What instructions would you give me? Here’s how we get to that $800,000 loss. We add a 28 percent tax bracket to the cost 25 years out, so they’re not just taking out $665,000; they’ve got to take out enough money to pay the taxes on that. Now we’re buffering something that is in the $850,000 range. That’s why you put this topic on the table for folks.

What are the solutions to all of this? Well, early in my career I learned something called “pennies on the dollar.” You don’t know if your clients will ever need care. Neither do they; and neither does the insurance company; nor neither do you, but most certainly if they need care this is a guaranteed equation to happen. For every dollar of care they need they have to get $1 of their assets or income to pay for it. It’s a very stark one-to-one relationship.

By using leverage and creating a wholesale opportunity for this instead of a retail opportunity you can literally take a portion of their investment interest income to put a huge pool of money around their assets so that in the event they need care there’s a lot of dollars to pay for it.

There are hybrid plans available that will allow them to get their money back if they don’t use it. If they need care, they’ve got money to pay for it for pennies on the dollar, and if they change their mind they can get money back. It solves all of it. The best advice is to use a portion of their interest income; if they don’t need their interest income to live on, this is a perfect financial solution.

What if they do need their investment earnings to live on? With medicine and science keeping folks alive longer today than ever before, if the husband and wife are the same age, statistically men are going to need care first.

If the man needs care first, and like Pac-Man gobbles through a significant portion of savings – and remember, we’re probably paying for it at full retail plus their tax bracket – what happens if that man uses a high percentage of these assets, pre-deceases his wife and now she lives another 15 or 20 years beyond his passing? What kind of lifestyle will she live on and what kind of reduced lifestyle and income will she have as a result of not having a plan and going by the strategy called hope? Bottom line: you can protect all of those monies by going into a program that will give you leveraged dollars to pay for care.

Is Home Care the Answer?

Ironically, one of the common responses you get when you want to talk to people about this is, “Hey, I don’t want to go into a nursing home. It’s going to take two doctors and six big guys to get me in a nursing home. I’m never going into one of those places.” What’s the preferred setting? Home care.

I have in my career met more than a dozen people who have spent in excess of $1 million paying for care in a combination of home and facility.

Years ago I had a client as an insured. I did not have his second wife as an insured. He called me one afternoon and said, “I want to buy more insurance.” I looked at a file and I said, “Sir, I don’t think you need any more.” He said, “I want to buy more insurance.” With that I made a trip to his home and within five seconds before I realized why he called me. His second wife had cancer. Fortunately for that household money was no object. I learned from him that he was paying on an annual basis $250,000 for care for his wife. It won’t take long at $250,000 to erase what most people have spent working their entire lifetime for. Even though we obviously couldn’t do anything for her, he wanted to beef up the insurance that he had with me.

Takeaways for Advisors

- Even though you manage risks every day, maybe wear that hat a little differently today because under it all you’re really a risk manager.

- Roughly 30 percent of your clients have a pension and most of their assets are tax-qualified, meaning they’ll be taxed upon withdrawal.

- We all age in place and aging in place has an inverse relationship to our investment portfolio. The longer we live, the more money we accumulate, and the more those assets are at risk.

- Denial is not a strategy. There’s a price tag for people who are in denial. They might think they have enough money, or their rationale is very strong. The price tag for denial is paying full retail plus your tax bracket.

- You can protect their portfolio by using some of their earnings and leveraging for pennies on the dollar.

Takeaways for Clients

- Most people prefer to pay wholesale versus full retail.

- Very few people take into account what the future and the hidden costs are. The consequence of not having insurance, the consequence of not having a plan, the consequence of leaving your family at bay to solve this issue can have catastrophic emotional consequences as well as the financial costs that we’ve already talked about.

- We’re all aging in place. Every day that we get a little older, the parts don’t work like they used to before and at some point they start to disassemble in a way that we would not prefer. The key is to go out quickly.

- Unexpected health events can have a dire financial and emotional impact on everyone.

- Simply using a portion of your portfolio earnings can resolve this issue for pennies on the dollar.

About the author:

Nyal Bischoff is an independent long-term care insurance specialist located in Troy, Michigan. Nyal has been in the financial services industry since 1982. Since 1988 he has specialized exclusively in long term care insurance helping thousands of people in Michigan protect their life savings from the high cost of care. As an independent agent he represents all the top carriers in both the traditional and hybrid long term care markets and is skilled at helping people navigate this complex area critical to a complete financial plan.

Because of his expertise, success and speaking skills he has often been the first choice as the lead presenter for product and group presentations for large audiences.

He was contracted with one of the largest insurance companies in the USA to train their Michigan agents about the nuances of this protection and is a sales consultant to several Wall Street brokerage firms for long term care for their financial advisors. He has been featured on radio talk show programs and has been referenced in newspaper articles about this subject. Thus far in his career he has personally sold approximately $4,000,000 of coverage.

Are you looking for a retirement speaker for your next conference, consumer event or internal professional development program? Visit the Retirement Speakers Bureau to find leading retirement industry speakers, authors, trainers and professional development experts who can address your audience’s needs and budget.

©2015, Nyal Bischoff. All rights reserved. Used with permission.