By Michael Falk, CFA, CRC®, Focus Financial Consulting

My primary motive here is to generate a thoughtful exchange for all of us regarding the benefit of long‑term economic growth. When we talk about retirement in a more positive fashion so to say, what we end up thinking about is a topic that’s actually quite young. Retirement’s really only existed for some 100 to 150 years, and it began based upon a simple concept that older workers had no more productivity capacity left. They used it all up.

And when I think about that, I think that is incredibly denigrating to older individuals. We also have to consider, and we’ll get into this, how that’s different today versus how it was 100 or 150 years ago. Bottom line is retirement is here, but what is it in today’s terms? Is it economically a loss of labor? Is it a “terrible waste of talent” and that’s a quote from a gentleman by the name of Dr. Robert Butler from the International Longevity Center.

Dr. Butler’s no longer with us, but I think this captures quite a bit and when we think about a terrible waste of talent, data from the Kauffman Foundation has studied and published that the highest rate of entrepreneurship in America is actually among the age demographic 55 to 64 today. Who would have guessed that? Is it expensive, too much, for all that are involved, workers and retirees alike? Or as we all remember from school then there’s always that last choice – all the above. And when you’re given a choice of “all the above,” how often is that in fact the correct answer?

Economic Implications

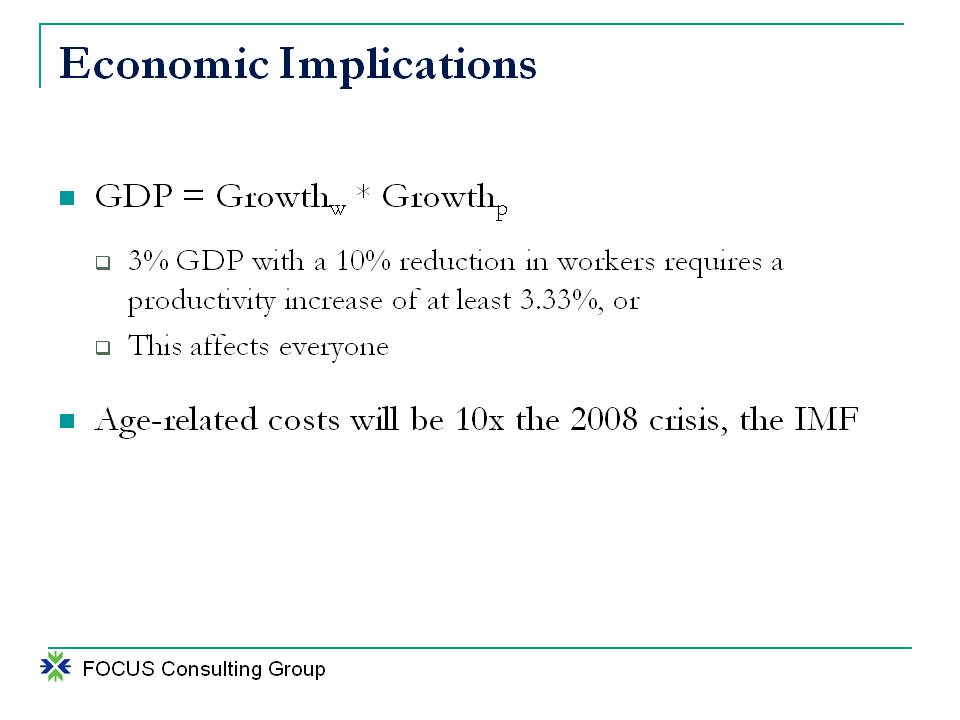

So, let’s get into the topic. What are the economic implications? When we talk about GDP (Gross Domestic Product) growth, we often think of the classic economic formula consumption plus investment plus government spending plus net exports. What you have in front of you is the alternative definition that gives you the exact same results.

Growth in the number of workers times the growth in output per worker. Let’s just do some real simple math here. If we want a three percent GDP in any given country and we experience a ten percent reduction of workers, that would require a productivity increase of at least 3⅓ percent just to maintain that three percent growth rate.

So, when we think about it from that perspective, it does beg an issue. No. 1, can we get to that level of productivity? No. 2, do we really want a reduction of workers? Well, so let’s take that first question. That level of productivity, 3⅓ percent, while it does not look like a big number, if we define productivity as output per hour of labor, the U.S. has never seen a decade from 1890 through 2000, and we can include through 2010 now, has never seen a decade where that productivity measure was greater than 3 percent – never.

Some of you are saying, what about since World War II was over? What about nonfarm averages of 2¼ percent? It’s just not there. In fact, globally, country by country, three percent is high by historical standards. Well, this is interesting because it affects everyone. Why does it affect everyone? Because if growth is slower, what we know as investment returns are lower. If investment returns are lower, that means not just savers but all investors, and as we know, retirees are still investing while they’re retired. Everyone is affected by this.

Nobody can avoid it, which leads us to this scary little piece of data. Age related costs will be ten times those of the 2008 crisis. This was released by the IMF (International Monetary Fund). Now, of course, this is talking by the year, you know, 2020, 2030 and 2040; that’s a straight line assumption. We can change this. This is well within our ability to impact. Nobody wants to repeat 2008 let alone something that’s ten times 2008. In fact we can go further. The United Nations regarding the OECD (Organisation for Economic Co-operation and Development) has estimated that GDP will be down by a third over the next three decades versus the last three.

Future Labor Shortages

So, that’s the point. We’re not talking about negative growth over the next few decades. We’re talking about a reduction in expected growth. At the end of the day, a reduction in the growth of the number of workers has a negative impact on GDP. That’s the point. So, when we talk about the growth or decline in number of workers, the question is, are we going to be facing future labor shortages? So, let’s start with some data.

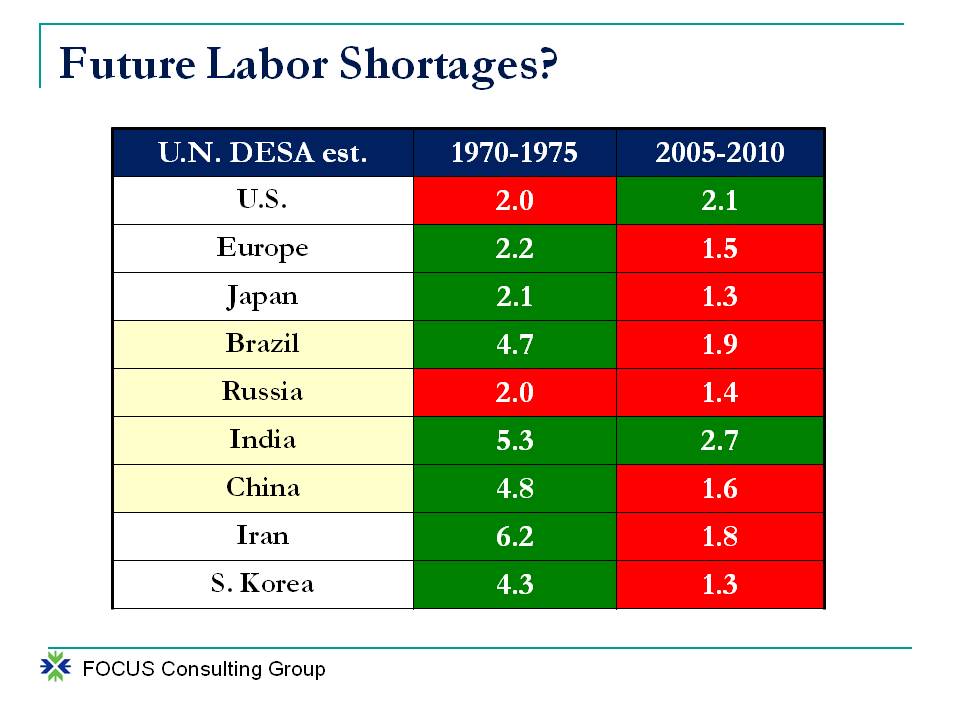

What we’re talking about here are fertility rates. You probably already know that 2.1 births on average per female in a society will stabilize a population growth. Higher than 2.1 grows the population. So, here’s what you’re seeing of the U.S., Europe and Japan and a little bit of a heat map. I’m showing over 30 years. Why over 30 years?

Because this is a real critical period of time. We can talk in terms of the baby boomer generation, or we can just simply talk about the growth in other parts of the world because people say this is a developed market’s problem, not an emerging economy issue. Well, here are the bricks: Brazil, Russia, India and China. What you can see is the fall in fertility rates is even greater in the emerging economies. We will come back to why that’s the case. Then finally, let’s add Iran and South Korea. Why? More Muslim-based countries.

Historically, Muslims have had higher fertility rates compared to other religion-based countries. What you can see on this chart, currently those numbers are below 2.1. Folks, at the end of the day, for all those who are worried about overpopulation, in the next two to three decades, we are going to plateau the number of people in the world and then it’s going to start to shrink. We are not going to have an overpopulation problem, but we do have an issue if we have this manmade structure called retirement that interjects.

So let’s talk about China for a moment, because China is a significant economic engine for the world. You can see their fertility number of 1.6. China will never recover; people know about the one child policy, which was very pro-male versus female. They reaffirmed the essence of that in 2008. Bottom line, today, there are roughly 120 boys for every 100 girls. They cannot come out of this population nosedive.

Economics Evolve

So, let’s move into why has this happened? Listen, economies evolve over time. Way back when, it was all agrarian or primarily agrarian. In fact, up until 1800 or the 19th century, economies were broadly 95 percent or more agriculturally-based. Today that number is less than five percent. This is talking about developed economies specifically. While again up until the 19th century, services were less than five percent of the economy, and they’re over 80 percent today. Manufacturing or the smoke stacks were the transitional phase. So, what’s happening?

If you think about agrarian-based economies and you think back to the original concept of retirement that older workers had no productivity left, this made sense. The physical capacity of individuals in their 60s and 70s, as an example, as it pertains to farming; they just couldn’t do it anymore. When it pertains to manufacturing or labor – not so easy. When it pertains to service-based economies, never in the history of the world have older workers had more productive capacity than today.

Well, now, when you think about how economies evolve and people having children, the first thing you should think about when you are working on a farm the children were the essence of free labor. When you think about healthcare 100, 200 years ago and we knew that fewer children survived to live because of disease, then you had more children. The three greatest explanations for why people are having fewer kids are because we have a lower need for cheap, unskilled labor today as compared to the agrarian age. We don’t need, from a healthcare standpoint, as many spares, which is not meant to be funny, but it’s true.

Great survival, sanitation and disease control is why we don’t need as many spares. In fact, increased longevity over time, we talk about how people are living longer and longer. It is estimated that that increased longevity is coming from 20 percent improved aging, which is good news, and the better news, 80 percent of it is from the drops in infant, toddler and maternal mortality, maternal being women passing during the course of birth.

So, getting rid of the zeros to five year olds in terms of the losses, if, the zeros survive, the five year olds survive, and the mothers survive because of greater sanitation and disease control, mortality has jumped. Overall, longevity has increased only about five to ten years, male/female respectively over the last 100 years. That number is starting to expand in fact.

Dependency and Migration

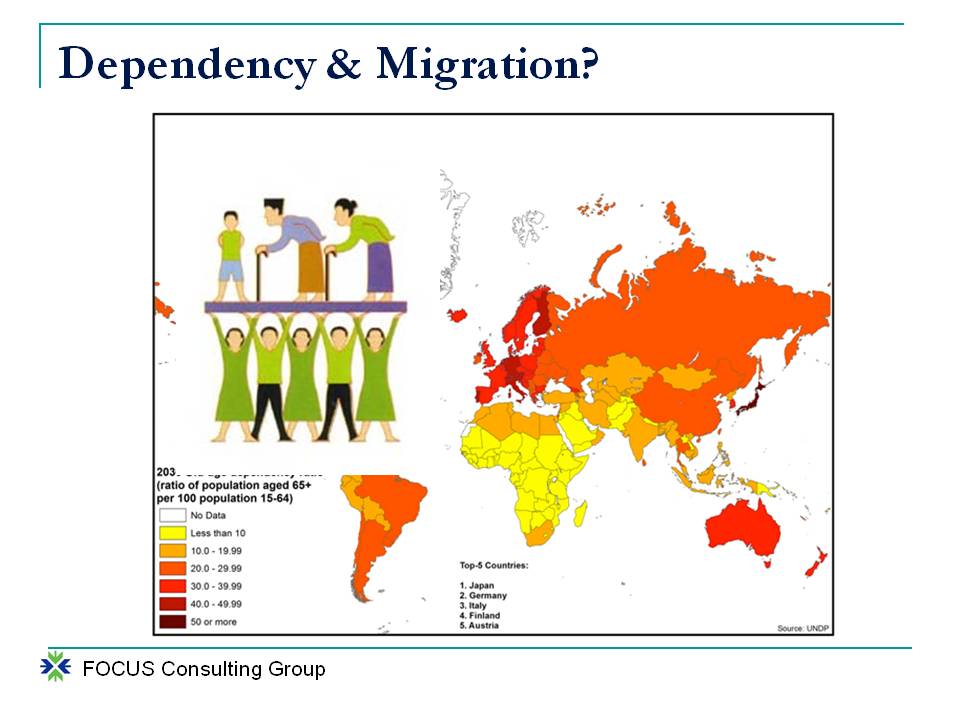

The final issue is as societies become wealthier, there is this kind of perspective that lavishing greater resources on fewer kids produces better versions of them. We’re giving them a greater ability to succeed. And we see that kind of in a competition standpoint of how people are busying their kids up with activities and learning and after-school curriculums. What does this lead to? Greater longevity and fewer children. It’s also what’s known as the dependency ratio. The dependency ratio in which basically – think of the working class supporting the young versus the old or retired class; that’s the simplest definition.

Dependency ratios, you can imagine, with fewer children, the young or pre‑working class is shrinking globally while the older class is gaining or growing. So, when you look at dependency ratios, they have an interesting mathematical construct. They’re good until they start to get a little bit worse. Then they get better again as we have fewer children and then as the worker population shrinks because of fewer children to grow up and more retirees, it gets demonstrably worse and it never improves. Why is this important?

Well, this is important because here is a view of the world in 2030 in terms of dependency ratios. Think of it as the closer you get to yellow, the healthier or better the dependency ratio is for these countries over the next couple, two to three decades. As you get more towards that deeper, dark maroon or red, the worse it is. What you can see outside of Africa and around India, the globe has an issue with the dependency ratio which leads to this migration question. A lot of people have thought that we can fix this by just allowing greater immigration into our country.

Well, not so simple because it’s a zero sum game globally and as you can see from this map, globally, everyone has problems. That’s aside from the fact if a given society is immigration friendly, if they can assimilate into the society. Bottom line is people underestimate that for the U.S. which has had a very long sustained solid, strong GDP as a country, it has been estimated that that reflects our ever‑growing workforce. About 40 percent of our population growth has contributed to that, whereas for example, in Western Europe, which is in bad shape from this aging perspective, the increase in population growth has accounted for an estimated 90 percent of Western Europe’s GDP.

The State of Retirement

Well, the population growth is shrinking, folks. We have to come to terms with some of these topics and retirement policies because retirements policies change everything. So what’s the state of retirement? Government programs, corporate benefits and then greater and greater individual or family behavior. This is what I want to take us into to review.

To start off with, let’s talk about social engineering. So in terms of Social Security or otherwise known as pay‑go schemes, this is a real interesting quote. “The system of which I was in was formulated deliberately in Depression times to intentionally discourage savings and coax job ‘hoggers’ into retirement.” That is a quote from a 2006 conference from Nobel Laureate Paul Samuelson. This conference was put on by the Federal Reserve of Boston at the Center for Retirement Research Institute at Boston University.

Social Security was born in an age where we wanted to shift workers into retirement to make room for other workers because of unemployment issues. So let me refrain and say that Social Security or pay‑go schemes are simply payments to people to be unproductive. If we just met on the street and you knew nothing about my background and I asked you this question, hey does it make economic sense to pay people to be unproductive? You would say absolutely not. With Social Security, this is exactly what we’re doing.

Low- to middle-income countries, think of the emerging developing economies, are going to experience the same types of challenges that Western Europe and the U.S. and Canada, as examples, are facing right now. They’re going to do it within 50 years of their development. It took the rest of us 150 to 200 years to experience this. Why? Because they’re creating retirement programs as they get wealthier and their fertility rates are falling at a much more rapid fashion than ours did, if I consider us the developed economy. Well, what happens is that the costs and risks crowd out personal savings.

You give people a program that says, “We’re going to help support you during your retirement and if they’re not financially literate enough, they don’t save or they save too little. The taxation maybe makes them think they’ve got it covered through Social Security. This is important because the displacement effect of public pension systems is that for a public pension, the equivalent dollar in expected benefits crowds out accumulated retirement savings by anywhere from 25 to 44 cents, so just the existence of the promises negatively impacts savings behavior. And we sadly know these days what’s happening to those promises because of the costs.

Private DB Pensions

So, if we’re going to talk about these types of pension systems, and Social Security is a pension and a lot more, but then we have to talk about just broadly speaking pensions. So, here is the good news about pensions. Pensions pool contributions and returns for a large number of people. Those who die leave their money behind. That’s the pooling of risks that helps to provide mortality credits to everybody else.

Because of those credits, a pension really on average only needs to fund the benefit for an 88‑year equivalent life, whereas in a defined contribution or personal savings format, individuals to equal that would have to save for a 105‑year possible life. Let’s put this another way: Pensions are a cheaper form of benefit. It allows benefits to be provided less expensively. I’m not negative on the ability of pensions to do good things but I’m quite hesitant and nervous about how they’re functioning today.

If the long-term estimated rate of return on the stock market right now globally is six to seven percent, which is what it is based upon a whole lot of different estimates, and the long-term estimated return on the bond market is two percent to three percent at most, somebody is going to have to tell me how in the world you get to seven to eight percent return assumptions even over the long term because these are the long-term estimates on their assets’ growth.

What has driven the behavior now is that pension systems are more invested into hedge funds or maybe alternative investments. Well folks, these are just other versions of investments. They provide leverage; they can only do roughly what other markets do other than the few investment managers who are truly special and add value.

The other issue is this leverage topic. You know, we’ve heard about state pension systems selling what they call pension bonds. Folks, this is a carry trade. You sell a bond. You get all the money and you hope to invest it at a greater return than what you have to pay out on the bond interest. This is not what we would refer to as good behavior.

Individual DC Plans

Are we asking these questions because pooling of risks is an extraordinarily positive and powerful tool for retirement and long-term planning? It doesn’t come without its risks. Take GM, the car company, as an example. Before 2008, GM essentially was a giant massive pension fund with a little side automobile business. Folks, let’s put this in perspective. The pool is having to include more and more people over time that are living longer and longer. It’s not sustainable. So, we turn to DC plans. Is this the solution?

Well, 82 percent of eligible workers are saving for retirement via their DC plans, not through IRAs. IRAs are primarily rollovers. So, this has taken us to increased self-responsibility. It’s not working because people aren’t saving enough. Well, the good news is we have some improvements there but we’re still not going to have that pooling of risks, right?

Saving is not natural. Saving is hard. There are a lot of different pulls on our income. Putting away for our future selves is not so easy although ironically studies and research have shown that if you see a picture of yourself in the future, it seems to help you save more today because you have empathy towards your future self. Financial literacy is tremendously lacking and from a lot of research, not so easy to boost.

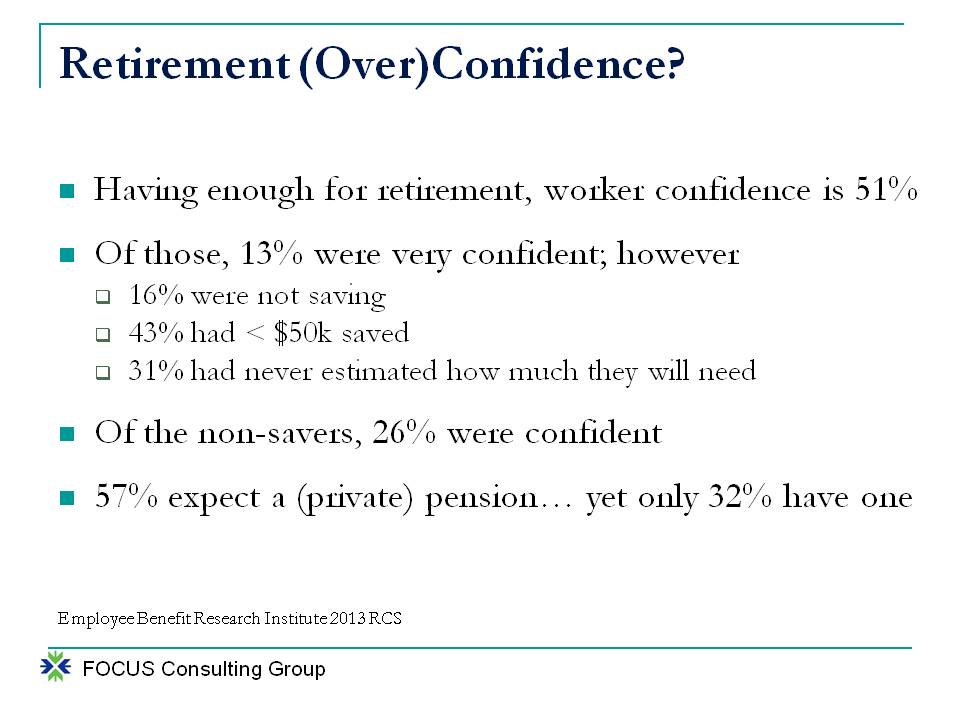

Retirement over confidence: EBRI and Mathew Greenwald & Associates gives us wonderful research every year. So, let’s just take a look at some of that research and ask some questions. When they ask people, “Do you think you’re going to have enough money for retirement?”, worker confidence is 51 percent. So, about half of the people are confident. That is not inspiring, but let’s dig a little deeper. Of the 51 percent, 13 percent of those were very confident.

So, let’s look at their behavior. Sixteen percent of them weren’t saving. This is fascinating. So, you’re very confident you’re going to have enough money for retirement and you’re not saving. So, are they telling us that they already have their big pile of money accumulated? What about the 43 percent of them had less than $50,000 saved? Folks, this comes back to financial literacy to a great extent. What is it going to take to retire? It can be a big number, certainly six digits. Thirty‑one percent of them never estimated how much they need.

So, in a sarcastic way, this is the one I find the most entertaining. Thirty‑one percent have never actually calculated how much they’re going to need but yet they were very confident. What is that confidence based on? My worry, and we’re going to come to this in a couple of bullets, that confidence is based upon the assumption of somebody else taking care of them. That’s my worry. What if that someone else can’t or won’t? Of the non‑savers, 26 percent were confident. I simply refer to this as the rich uncle approach to retirement planning.

People are going to have to die to allow you to retire. You know, that’s a jarring statement. Think about that for sec. Do you really want people that you love to pass away so that you could retire? Fifty‑seven percent of people expect a pension. Only 32 percent have one. People think something is going to take care of them which means they’re not preparing. That’s the behavioral reality. This is all from EBRI’s current research.

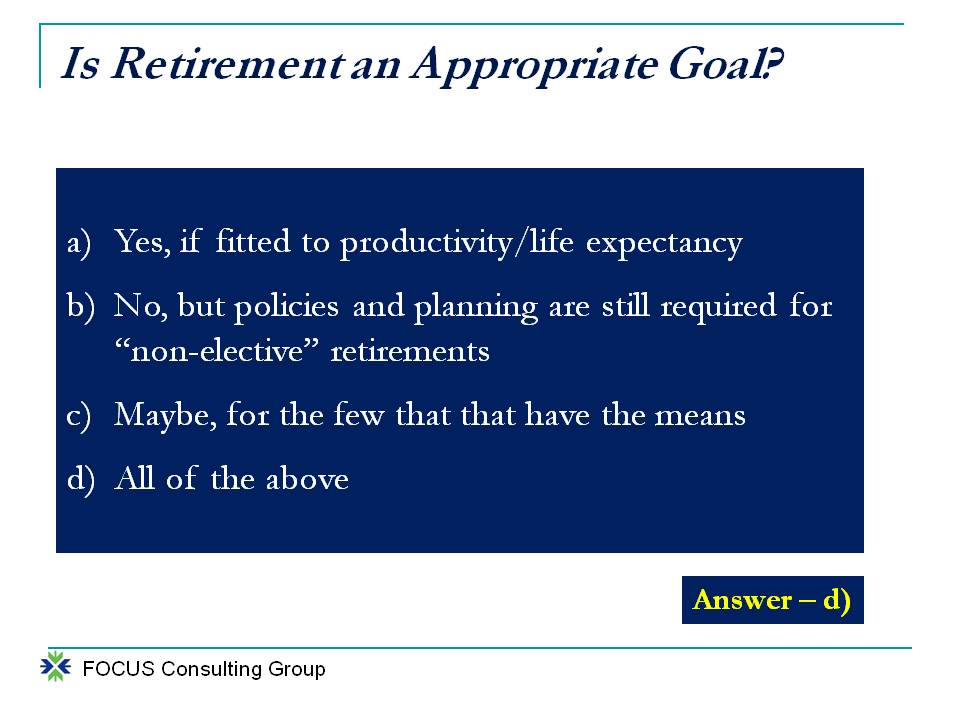

Is Retirement an Appropriate Goal?

So, which takes us to is retirement an appropriate goal? Here are the options:

A: I would say sure, if it’s fitted to productivity capacity or if it’s fitted to life expectancy, right? So, let’s make the math work for pension systems or Social Security systems.

B: Is no, it is not an appropriate goal. It’s not good. The policies and planning are still required for non‑elective retirements. What do I mean by non‑elective? Forty‑seven percent of early retirements according to EBRI are non‑elective: health, lack of employment. So, we can actually think of retirement planning as our own personal future unemployment insurance if we’re not capable. This is an important issue. What’s also important is expected age at retirement. So, today 43 percent by survey expect retirement to be when they’re 66 years of age or older, or never be able to retire, 43 percent. A decade ago, that number was only 23 percent.

C: The good news is that people’s perspectives are changing. We don’t know if these perspectives are changing for the right reasons however. So, maybe retirement’s appropriate for the few that have the needs. Listen, I’m not saying don’t retire. I’m saying there may be better things in life. Keep that thought in mind. I’m going to provide you some research in that area. And then of course all the above but, you know it’s an interesting issue, right? If retirement is too expensive for most people, then are we setting them up to fail?

Socially Re-Engineered

So, the first step is we talked about social engineering. Why don’t we re‑engineer it, folks, for all of the debates, all of the arguments? This is why I want to have a thoughtful exchange. Retirement at the age of 65 or 62 doesn’t work for society. I can also argue it doesn’t work for individuals, but we’re not there yet.

First of all, it doesn’t work for society. Listen, we can want certain things but we have to deal with reality. We have to age the retirement age.

If we wanted to stabilize the pension ratio long term, retirement needs to be at the age of 73. If we want to match the biological capability to work physical capacity, age 73. If we want to match longevity improvement or mentality reductions, age 72. Folks, we basically know the age; nobody wants to accept it. And governments are too chicken to actually move the age to the early 70s. Consider the work in the EU. I want to appreciate this and I hope this comes to America.

As the European Union is talking about increasing their retirement ages – we’ll leave France out of the discussion for a moment – they don’t know what they’re doing. The EU has put language in and proposed that the age at which someone is eligible to retire will be in consideration of the work that they do. Think of it this way: laborers, blue collar if you will, who are using their backs, their arms, their knees cannot work until they’re 70 plus. Let’s be real. White collar can easily work until they’re 70 plus.

And before people immediately knee-jerk and say well, wait a minute, they’re going to cost us that much more assuming you’re white collar. No, they’re not. One of the dirty little secrets about Social Security and longevity is laborers and people at the lower end of socioeconomic schedule don’t live as long. Letting them retire earlier will not harm the fiscal solvency of the system. People who look like me, white males, white collar, we’re the most expensive tax on the system because we live the longest and we have the highest amount of income to replace.

So, instead of social insurance or a pension, why don’t we think about this as a premium refund and means testing? Here’s an interesting little factoid for most people. When you start receiving Social Security, on average within 60 months, you will have received back every penny that you paid into the system. Now, that is not adjusted for investment returns. That’s just cash on cash within 60 months. My thought is, get your premium refund, your insurance premium that is, and then maybe we do some form of means testing.

Re-do Retirement

We need to redo it. How do we do it?

Remember, working longer makes the target age of when you can afford to retire much easier to achieve, and it’s okay for society because people are better financed, they’re more self-responsible and they’re retirement periods are shorter. It balances economic growth.

People with a sense of purpose in life are 57 percent less likely to die over any given five‑year period. This was studied by Rush University Medical Center with people of the average age of 80 – fascinating. Those who ranked in the top ten percent for muscle strength were at a 61 percent lower risk for developing Alzheimer’s disease than those in the lower ten percent for muscle strength. All else being equal, people who remain in the workforce have lower death rates. Study after study after study supports this issue – lower death rates and healthier aging.

If you have people who retire later, and have healthier aging before they pass on, it lowers cost to societies. Medical expenses in the final three to six months of one’s life typically equal the rest of the medical expenses over their entire life. There’s a big deal with healthy aging. And let’s be honest: when people are healthier, they’re generally a little bit happier. I published an article in 2011 entitled, Enough about the Assets Already. This entire industry focuses on the assets. Listen, can any one of us control the future returns in the markets on our stocks and bonds or mutual funds? Absolutely not.

What’s interesting is a psychologist will tell you people are generally happier when they feel they’ve got more control. If you want to have more control as a retired individual, then have fewer fixed expenses. Make your spending primarily variable. Going to a concert, going on vacation, travel, make it variable expenses, not your mortgage, not a car payment. This is what I’m talking about in terms of liability management.

Folks, we need to redo retirement. We need to let people know what it is, what it isn’t. It’s more than just money. It’s about what you’re going to do with your life. What do you want to do with your life? By the way, doing keeps your happier, healthier, and will allow you to age better.

So ask the question, what good is retirement? If it’s unhealthy for people, if it’s not good for businesses because they need workers, and it’s not good for an economy’s growth long term. The fact that we still are focused on this just makes me scratch my head.