By John E. Nelson, Purposeful Retirement Advocate, Author & Coach

Editor’s note:

This presentation was delivered in live webinar format in 2015. John’s comments have been edited for clarity and length.

You can view a YouTube brief of the original presentation here.

You may also choose to take the full length course and earn 1 CRC®, CFP®, and/or PACE CE credit.

Retirement happiness is a fascinating topic. First out of college, I started out as a financial advisor and then quickly moved into the pension area, designing, consulting and managing qualified retirement plans for employers. Pretty quickly, one of the things that I realized was that retirement finance is about people. One learning objective for this course is an idea and understanding of the relationship between income and happiness.

We toil away as individuals for decades and we work as advisors to help people establish a healthy and sufficient retirement income. What’s the relationship between income and happiness? We assume there is one, and of course we assume the more income, the happier we are. But let’s look at the science on that. The second learning objective by the time we finish today is that we’ll have an idea of what the main types of happiness are from research.

Types of happiness sounds funny but that will make more sense when we look at the kinds of research that psychologists have been doing – and economists – to look at the approaches and the pathways that people can take to be happier in life. That really comes to bear as we approach retirement.

The third learning objective is Harry Markowitz and Modern Portfolio Theory, which I’ve used as a springboard to understanding how to create retirement happiness also using a portfolio method. We’ll touch on are what the stages of retirement life are and how that translates into retirement. Making those transitions is a risky time in life because things change, so we’ll touch on what those risks can be.

And lastly – and this gets really to the heart of this idea of a successful transition – is that post-retirement, after that transition, people literally can have a different sense of identity, a different sense of self, and the life roles and social roles that they fulfill can change.

Part of what we talk about today is in the current edition of What Color is Your Parachute? For Retirement, but I’m working on the third edition, and most of today’s presentation will be in the upcoming edition, which won’t be out until next year. So this is a peek ahead into the future of the next version of this book.

The Relationship Between Income and Happiness

The reason that I made this transition from working just on the financial side of retirement preparation to this broader life planning idea is that, like you as a professional, I saw people who did all the right financial things, transitioned to retirement, and they had a fantastic life. They were happy, they were socially engaged, they had a sense of meaning and purpose, and they were active. Not only were they enjoying life, but they were actually doing something positive, constructive, that in fact, life after their career was the peak of their time in life; that they were, in fact, the best self that they had ever been.

On the other hand, I saw other people who did all of the same financial preparation, but they got to retirement and even though they had done the right financial things and they were financially secure, that next stage of life was not a success. For a variety of different reasons, they were not living the best version of their lives. Sometimes they were aware of being pretty unhappy in many ways; life, in fact, was better for them while they had been working. That was a paradox for me. While financial preparation is essential, there is no retirement without it, how can they design their life to be more successful?

If we ask people what will make them happy, get them to project into the future and do some life planning in advance and say what will make them happy, the first answer we get a lot of the time is simply “not working”. If you have a really bad job then not working is enough. When we invented retirement about 100 years ago, most jobs were dirty, dangerous, hard work. And simply the absence – the relief – of not having to do that dirty, dangerous work anymore was enough. But most of us don’t have jobs like that now. We may not love our work, but it’s truly not toil. It’s not that the absence of work by itself will bring happiness.

So if we try to go a little bit deeper and say instead of retiring FROM your job – which is how many people look at it – what would you be retiring TO? People say: I’d like to travel. I’d like to take up a hobby. I have a hobby. I’d like to spend time with friends. Travel, hobbies, friends; I don’t want to make light of these activities because they are important, but these answers are usually just an indicator that people haven’t really thought about it. This is the equivalent of when you have kids in school and you say, “How was school today?” And they say, “Fine.” It’s an answer that doesn’t really have thought behind it.

How do we get people beyond this, at a deeper level? One reason why it is helpful from a financial perspective is because the more time that people put into planning their life can actually, in many people, stimulate better financial planning; it’s all a package. We are learning from science that we’re often not good at predicting what will make us happy. We fantasize activities in the future that are wonderful in our imagination but they’re divorced from reality. Once we do them, we discover that they really weren’t that happy or fulfilling or engaging. They weren’t what we imagined.

Anecdotally, a good example of that is I happened to be, a couple of years ago, looking on Craigslist for a used car for my son. And I ran across this interesting post: “Jayco Popup Camper. My wife and I decided to give camping a try so we purchased a new popup camper. We went to Devil’s Lake and camped out for one night, then put the unit into the storage building for the last year and a half. It’s virtually new. The price for a new unit like this is $10,000; I’m asking $7,500 or best offer.”

Larry and his wife had this beautiful vision. They imagined and dreamed about the wonder of camping, so the way that they explored that is that they went and spent $10,000 for a new camper. They used it for one night and discovered that this wasn’t for them at all. So here’s the question. This is a trivial example – not that $2,500 for one night at the campground is trivial; you couldn’t afford to do that over and over. But it’s symbolic of example what we do as humans: We imagine something and the reality doesn’t match up. What are the processes that we can use to stimulate people to think at a deeper level using kind of a scientific approach to understand how they can understand themselves, and to prepare better for this stage of life that they spend literally 30 or 40 years of preparation.

The Main Types of Happiness

Enter the happiness researchers. About ten years ago I was attending a conference in Washington, D.C. hosted by the Gallup Organization – the national polling and management consulting firm – and I had a once in a lifetime opportunity. I spent an evening with these two guys: Daniel Kahneman and Martin Seligman. This was a conference of researchers conducting actual scientific research into what makes people happy.

Marty Seligman, called the Father of Positive Psychology, was the pioneer who took university-based research psychology and instead of just studying all of the mental illness unhappiness that psychology had been studying for decades, secured the funding and attracted the researchers to start doing large scale experimental studies into what makes people happy, how people thrive.

Marty Seligman had been the president of the American Psychological Association just a couple years before, and he was an eminent researcher at the University of Pennsylvania for 25 years at that point. I was taking a coaching-training program with him and was invited after the presentations that day to an evening event in a suite at this hotel.

He had invited the keynote speaker for this conference to join us for that evening, Daniel Kahneman. Kahneman is a professor at Princeton and is the only psychologist to ever win a Nobel Prize. In 2002 he won a Nobel Prize in economics. Kahneman, along with his longtime collaborator who had passed away a few years before, essentially created the field we now call behavioral economics or behavioral finance. He’s a genius among geniuses, the guy who started the whole behavioral economics phenomenon.

These two guys knew of each other but they didn’t conduct any research together. Over the course of a couple of hours in this hotel suite with essentially a small group of people, two of the leading geniuses in the world talk about the nature of happiness and how to approach both the study of happiness as well as helping people to be happier.

Kahneman’s view was really about looking at what people already do and using research techniques to uncover the relationships between how people think and the resulting happiness or well-being that they have in their lives as a result. Behavioral economics and behavioral finance is about the gap between people’s immediate perceptions, their rules of thumb about doing things, and how divorced or different that is from a rational approach when it comes to thinking about financial or economic decisions. It’s the split in the human mind between thinking rationally and just using rules of thumb to make quick, rapid decisions that are often economically not the correct way to go. His interest in happiness was similar. He looked at some of the questions of what do we actually experience in the moment as happiness or unhappiness, and then how we, by our thinking, change that in some way or alter it. We’ll look at a landmark study that he was part of that is foundational to anyone in the retirement or financial planning world.

Marty Seligman was studying processes that people can use to make themselves and other people happier, especially studying what works to increase happiness in life.

Let’s look at an underlying assumption that we have been using our whole careers. The game of ‘Life’ was a board game introduced in the early 60s, not quite as popular as ‘Monopoly’, but very popular for a long time. The game of ‘Life’ contained the twists and turns we take with the things that happen to us. It won’t surprise you to know that a lot of this game, like ‘Monopoly’, is financial. You need money to play the game, and at the end of the game, you end up in one of two places with no in between. It’s all or nothing: You’re either in Millionaire Acres or the Poor Farm. And it goes without saying that if you end up at Millionaire Acres, you’re happy; and if you’re in the Poor Farm, you’re sad – the game of ‘Life’. We have automatically linked more money with more happiness and lack of money with less happiness. That’s largely true. The question is, how is it true or when is it not true?

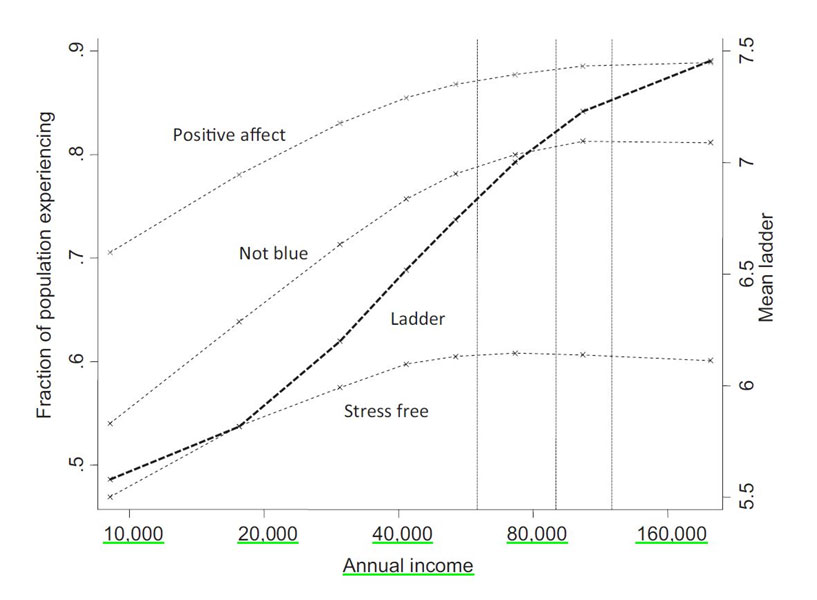

That’s what Daniel Kahneman figured out for us. There would be a lot of studies going forward on this topic, but a particular one that we’re going to look at here is a landmark. I would suggest that for your job, this might be the single, most important data chart or figure that you could study and understand to have a sense of the purpose of your work in the world.

What Kahneman did, with the help of the Gallup organization, is telephone over 1,000 Americans every day for a year. They ended up with over 400,000 responses for this study. They asked a number of questions, with some having to do with the emotions that people had experienced. From Kahneman’s research, we know that the longer you wait to ask people about their happiness, the less accurate their answer will be. The polls asked people about their experience of the prior day and about their income level – these were not retirees but from all strata of society, income levels, and age bands. What does this chart tell us?

Look at the bottom where you can see, left to right, that the simplest part is income bands, people making $10,000, $20,000, $40,000 a year annual income up to beyond $160,000. The data on the left axis is the fraction or percentage of the population experiencing which affect in the prior day. Why is this important? Let’s look at the first one.

The first result here is positive affect, what most people would call happiness; that is positive emotions in the moment. People were asked to what extent did they had feelings of happiness or joy, or did they enjoy themselves yesterday? And as we can see, these people – even the people only with $10,000 a year of annual income – 70 percent of those people said that they had experienced these causative emotions or positive affect the prior day.

But sure enough, at $20,000, $40,000 there was a greater likelihood, or a greater proportion of them, had joy and happiness in their lives. But we notice a plateau. The people at $160,000 of income didn’t have many more positive emotions than people at $80,000. $80,000 to $160,000 is doubling of income with almost no increase in positive emotions. If people pushed and worked and tried to get their income up from $80,000 to $160,000 a year, just like that person buying the Jayco camper and discovering after one night that it wasn’t their thing, people who focused on increasing their income – most of them – are not actually going to have more positive emotions in an actual, regular day than somebody making $80,000. There are all kinds of other probable benefits, but positive emotions is not probably one of them.

Let’s look at the next one. This is the other side of that coin which is the absence of negative emotions. In fact, people have positive emotions and negative emotions in the same day. This was asking people about not feeling blue, about not having those negative motions. Of people earning $10,000 a year, only 55 percent of them could say that they had not had blue or negative emotions the prior day. That is pretty amazing in itself: over half of them didn’t report feeling negative emotions. And that got better as we went up but we still got that same plateau. After about $75,000 annual income it didn’t improve people’s opportunity to avoid those negative emotions.

Thirdly, they asked people about stress: to what extent yesterday was your day stress free? And of course as humans, we didn’t score near as well on this one. Because in general, for people at $10,000, only about 45 percent of them could say they had a stress free day. But the same phenomenon continued. Reducing stress peaked at about $45,000 of annual income. People at really high incomes ($160,000) may have more stress than people at moderate incomes of $40,000 or $50,000, with $80,000 being the least stress reported the prior day, in that study.

When we look at this we may say: what is money good for? What is higher income good for if it doesn’t necessarily bring about more positive emotions, reduce negative emotions, and especially if it doesn’t reduce stress that much for higher income levels?

There’s one part of this study that is really eye opening because it’s so different from the actual experiencing of emotions that Kahneman identified. Kahneman’s specialty is looking at these divisions in the human psyche. The emotions that people reported as of yesterday is fresh, good data. They have a memory of what they did and felt yesterday.

But let’s use a scale that’s been used since the 60s called “the ladder of life satisfaction.” This takes the overall view that people have of their lives in the big picture, not yesterday, what they experienced as data, but how they feel about their experience of life.

The question literally goes like this: Imagine a ladder with steps numbered from 0 at the bottom to 10 at the top. The top of the ladder represents the best possible life for you, and the bottom of the ladder represents the worst possible life for you. On which step of the ladder would you say you stand at this time? When you evaluate your life satisfaction on this ladder, is it a zero, a ten, or somewhere in between? How satisfied are you with your life?

Here’s what the survey showed. On the left you can see that of people with only about $10,000 of annual income, almost half of them thought life wasn’t that bad; it was about a 5. That’s amazing. What’s really amazing about this, though, is that this effect, this evaluation of life – this life satisfaction – did not plateau as early or as quickly or as remarkably as the actual emotions. There was a disconnect. People with higher incomes didn’t have better emotions but they had more life satisfaction. Kahneman would say that more income did not improve their experience over about $75,000 of income, but did improve their evaluation and satisfaction with their lives.

That is what I think you are doing for your people in your work as a financial planner, benefits counselor, plan administrator. By helping them build secure retirement income, ultimately you are helping them to evaluate their own life more favorably. When they get to retirement, their satisfaction with life will be better with more income. So this goes way beyond the functional aspects of all the things we do with money.

It shows us that prosperity and good health are merely the foundations for happiness. They do not create happiness. But not having sufficient income hurts people’s opportunity to be happy. Not having good health hurts people’s opportunity to be happy. So what we’re doing is helping them build the foundation. We’ll look at two approaches that go toward the creation of approaches that people can use to plan a life to be happier in retirement.

Seligman says that most of us have an automatic knee jerk reaction that happiness comes from pleasure. He identified that pleasure is just one way of being happy. In fact, there are three paths to happiness, with two other approaches that are not as obvious: engagement and meaning.

Pleasure doesn’t take effort or skill or require anything of you. But engagement is using our skills and strengths and abilities toward a positive challenge, especially one we choose and we value; one we think we can be good at. Most of us, if we’re lucky, are likely to have engagement in our job if we’re in the right job doing the right work using the right skills. In retirement we lose that. An engagement as a path to happiness is something we need to cultivate for retirement. Pleasure is what we think about; having fun. It’s like retirement is a vacation. Engagement is like retirement as work but positive work, positive challenge. That’s what engagement means.

The third path, meaning, involves being of service to something beyond ourselves. In our working career, our sense of meaning and purpose may come from doing a good job at work, of being part of the team, serving the world in some way. Our sense of meaning and purpose might revolve around being a good breadwinner and supporting our family, helping our family members, raising kids.

As we enter the retirement stage of life, meaning and purpose can be in jeopardy. If the kids are grown and we don’t work anymore, what is our sense of meaning? This is Seligman’s simple formula breaking down the three paths to happiness in to very simple, discreet, effective analyses.

When it comes to planning retirement, people think about retirement as pleasure and enjoyment, a vacation. But they can’t do this for 20 or 30 years with engagement and challenge. People don’t think about this because from the outside, engagement and challenge from the outside looks like work. So finding things that look like work in retirement, people may shy away from that.

The secret is this: If you’re using your unique skills and abilities, you can accomplish things that seem impossible to other people, but not for you. You get a state of enjoyment and flow and you’re totally occupied. Finding these sources of engagement in retirement is the key.

Meaning and purpose: There was an article years ago in the Washington Post about a geriatric psychiatrist who worked specifically with elderly people with mental health issues, mostly depression. Based on his years of working with people who had been long retired, and their mental and emotional problems, he summed it up that they just want to feel that they and their life matters. Once we retire, will we matter? Most commonly, our sense of meaning and purpose comes from what we value most deeply to give us a sense of meaning and purpose. How do we find these things?

How to Create a Retirement Happiness “Portfolio”

What we do is we build a retirement happiness portfolio. Harry Markowitz said that you build a portfolio by finding investment assets that don’t have the same kind of volatility. By putting fundamentally diverse elements together, it makes the whole portfolio stronger than it would be by these disparate or diverse elements in the same portfolio. This is the idea of a modern portfolio theory combination.

There’s another way to use the financial way of thinking that helps: The famous “Morningstar Style Box,” in this case the equity’s version, which says that we can easily categorize these equities by their capitalization – small, mid or large cap – and by their investment style: value, growth, or blend. And again, building a diversified portfolio – by being able to understand and cover the appropriate boxes that it gives a stronger, more diversified portfolio. That’s the theory.

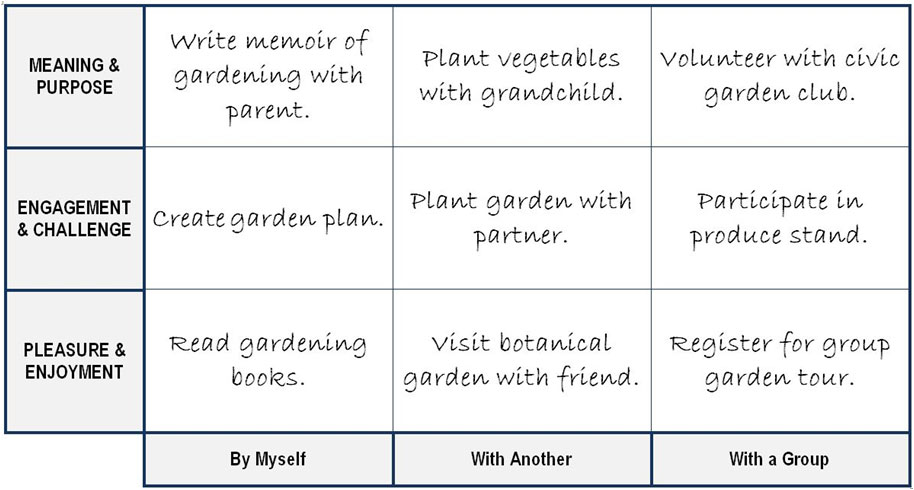

Can we do this with happiness? To Harry Markowitz, Nobel Prize winner, it’s a pretty good idea. Can we translate this to planning our lives? The answer is yes. On the left side of the chart below are the three paths to happiness that Martin Seligman identified. At the bottom we have the first path or approach to happiness that retirees usually have no problem finding on their own: enjoyment and pleasure.

On the left hand side in the middle is that next step up: engagement and challenge. Those are the activities that require skills that require strengths and abilities to perform. The sense of accomplishment and competence that we get in life. The third has to do with meaning and purpose: retirement life planning activities that help us align with and be of service to something greater than ourselves. Across the bottom we split or organize those activities based on the social connection that we’re making because beyond Seligman’s three paths to happiness, the single greatest indicator of human happiness is social connection.

The more social interaction and social connection we have, the happier we are. The three columns are activities in the next stage of life in retirement that you can do by yourself, activities that you would do with another person, and then lastly activities with a group.

Let’s take a simple example about gardening to illustrate how this works. One thing people can do for pleasure by themselves would be to read gardening books. It doesn’t take any skill and can be done by oneself. But to rise up a level for engagement and challenge would be to research and create a garden plan for the next year, figuring out how different ground covers and plants could work together in the garden. And for sense of meaning and purpose, something you’d do on your own, perhaps, would be to write your thoughts or stories about gardening with your parent. That gives a lot of people a sense of meaning and purpose is to know where they came from and being part of a larger family.

How about an activity with another person? Pleasure and enjoyment would just be visiting a botanical garden with a friend, which doesn’t take any skill. To go up a level one would plant a garden with a partner. How about meaning and purpose? That might be planting vegetables with a grandchild and passing on and being of service to someone, something beyond ourselves.

Lastly, pleasure and enjoyment in a group might be registering and joining with a whole garden tour and being part of a larger group of people, where you get to know some of those people. Engagement and challenge. In this example, to achieve the highest sense of meaning and purpose, would be joining a gardening club which regularly meets with other people who have similar interests and values because they are working in public gardens for the greater good of the community.

We can take people by the hand and lead them through this as a portfolio of choices, important because as people age they find there are some things they can continue to do, and some they can’t. It’s the portfolio aspect of this that gives people the ability to weather those changes in life.

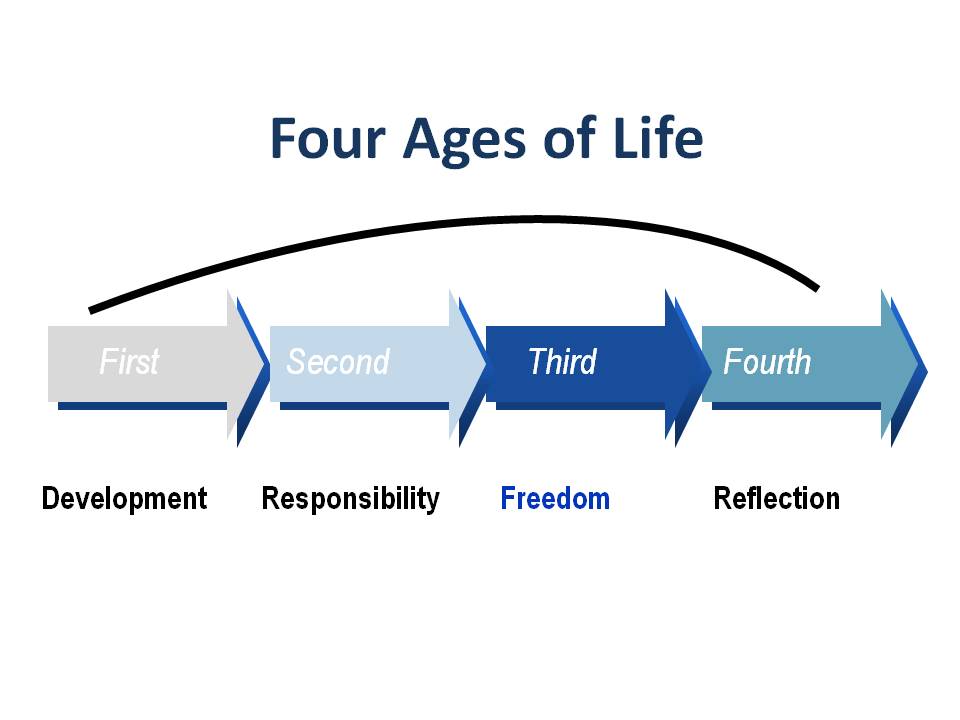

People when they retire have to figure out who they are now. A better way to think about where people are in life is this model by Peter Laslett from Cambridge University years ago, who talked about life as having four ages.

The first age is about development, being a child whose main focus is to develop for the life ahead. The second age of life is to take on responsibility, being a spouse, parent, caregiver, worker. The people in this second age of life make commitments in their lives and they get it done. The next age of life for most of us in retirement is about freedom from all of those responsibilities. The world opens up and we are free to engage, sometimes for the first time, in what we consider to be most important in life when our health is still good. The fourth age is the latter part of retirement when our health ability to do things, and our social connections. The purpose of that fourth age is to make sense of life and reflect on the other three ages.

Here’s the important thing. As we go through these ages of life – the four ages of life – our roles change; our social roles, our life roles. So, if you only took away two things from this, the first is that, similar to an investment portfolio, it’s literally possible for people to create a happiness portfolio of diversified activities across all the three paths to happiness that give the resilience, flexibility and ability to weather the future storms of life. And second, instead of seeing the transition to retirement as losing the essential roles and identity, people can take this time to consciously explore and choose new roles for the next stage of life. Doing these two things, especially with a specific process, make it possible to actually plan ahead and to be better at predicting what’s going to make you happy.

About the author:

John E. Nelson is a career and retirement coach and speaker. He is coauthor of the best-selling and award-winning book, What Color Is Your Parachute? For Retirement.

His work integrates research from psychology, economics, medicine, and other fields. John’s Well-Being model has been used by the federal government, professional associations, AARP, the United Way, FORTUNE “100 Best Companies to Work For” employers, and others.

John and his work have appeared in TIME, The Wall Street Journal, The New York Times, USA Today, Business Week, and other publications.

John taught at the University of Wisconsin while completing the coursework for a PhD. But he wrote the Parachute book instead of a dissertation — even though he knew it wouldn’t count! The book is available here on Amazon.

Are you looking for a retirement speaker for your next conference, consumer event or internal professional development program? Visit the Retirement Speakers Bureau to find leading retirement industry speakers, authors, trainers and professional development experts who can address your audience’s needs and budget.

©2015, John Nelson. All rights reserved. Used with permission.