But what we’ve seen over the last 20, 30 years is the decline of traditional DB pensions, those true pensions that provided a guaranteed income for life. We do have other kinds of pensionized income that workers earn through mandatory old age pensions such as Social Security. But the replacement rate from those programs in retirement is low, and expressed as a fraction of income the replacement rate gets lower as your income increases.

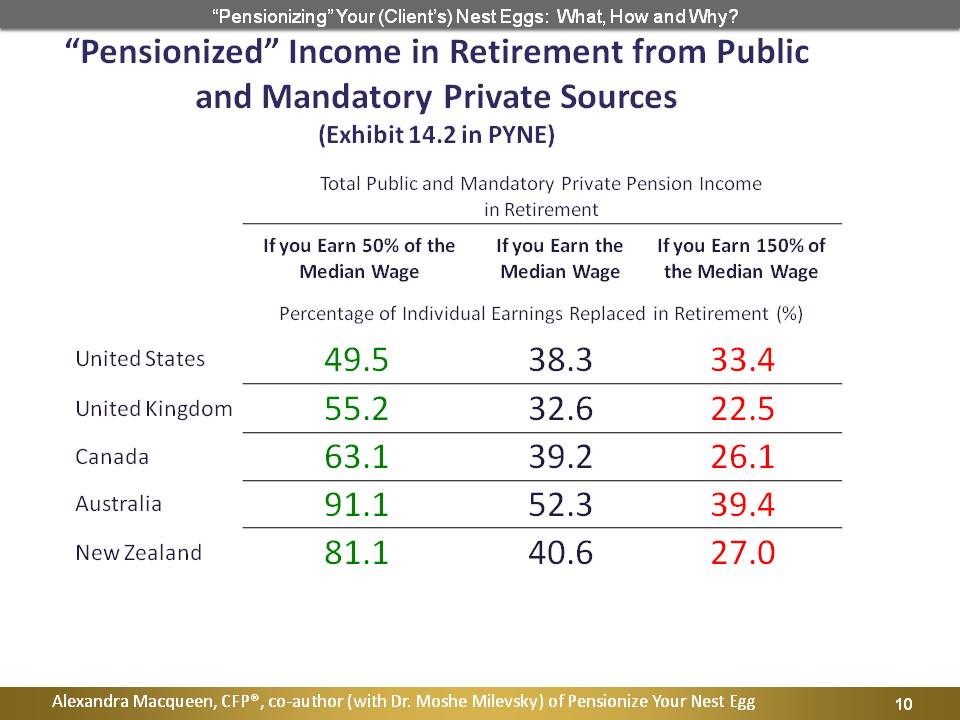

So if you earn approximately the median of what your peers are earning in the workforce, retire and collect Social Security and any other mandatory private pension income sources defined by the OECD, you might get as much as 52 percent – that’s from Australia – of your pre-retirement income replaced from those public and mandatory private sources. If you earn 50 percent of the median wage the proportion of your pre-retirement income that’s covered by those mandatory sources increases, in fact, all the way up to over 90 percent in Australia.

In the chart above, in red we see if you earn 150 percent of the median wage, the fraction of retirement income that you can get in retirement from Social Security drops down – in fact, it’s the lowest in the U.K. – but the United States is put at the top as the most populous of all these countries. This is the sector of the population for whom pensionizing is an issue.

If I might get 50 percent, 60 percent, even 90 percent of my pre-retirement income replaced by virtue of programs overseas based on my participation in the workforce, or my age if it’s an old age pension, I’m not going to worry too much about this. But take a look at the other side of the ledger; I’m going to worry a lot if that replacement rate is one-third or one-fifth of what I’ve been receiving prior to leaving the workforce.

In sum, we’ve lost for the most part these traditional defined benefit pension plans where only 14 percent of workers in the United States now have a defined benefit plan, and what we know is that those pensions provide protection against risks that we don’t face in the accumulation stage of life.

What are these new retirement risks?

There are three basic retirement risks. The first one is longevity which, of course, is just the risk that you run out of money before you run out of life.

We often think that life expectancy is from birth, so we might see a number like 80 or 84. However, if we calculate life expectancy at the age of 65, it will always be a longer timeframe than life expectancy at birth.

If you are U.S. male and you have made it to age 65 you might expect to live 17 years, and there’s a standard deviation around that average of 8.65 years. You might live 17 more years, but you also might live 17 minus 8 years or 17 plus 8 years.

For U.S. females, they can expect to live to a later median age and a later absolute age. There’re a lot of additional years that females on average might live as a group.

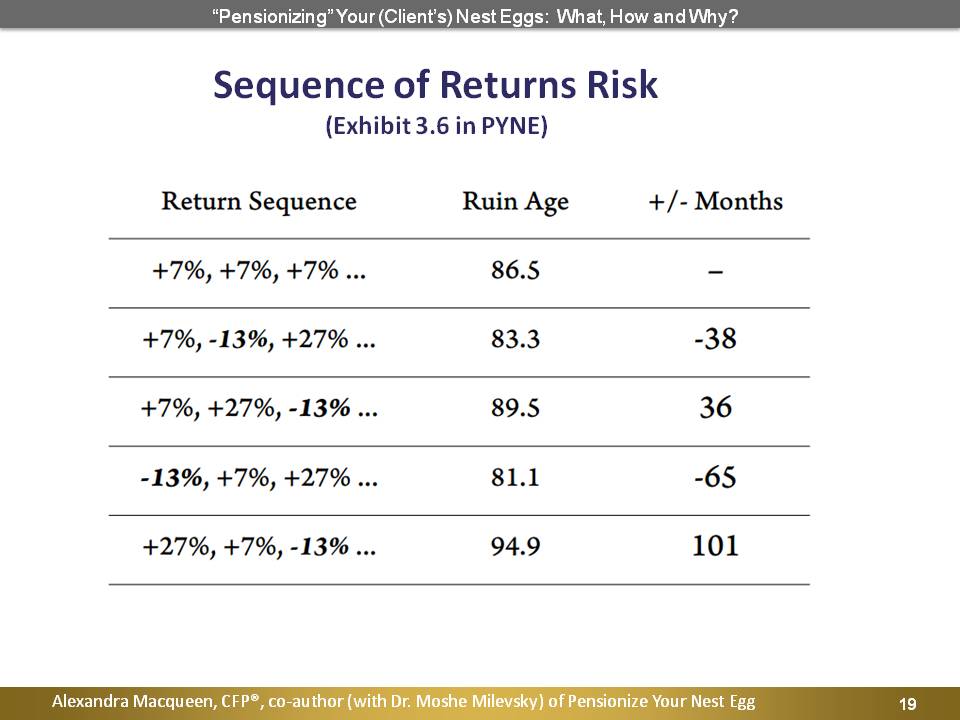

The second risk is sequence of returns risk. Let’s assume we have a retiree starting at age 65 with a portfolio that’s earning a 7 percent annual rate of return.

When do we run out of money which we define as the “rule in age,” when the portfolio worth zero? At age 86.5 if we receive smooth predictable 7 percent returns.

Let’s think about the ways in which a 7 percent return can be calculated mathematically. To illustrate this concept in the second return sequence above we have returns of 7 percent minus 13 percent, and plus 27 percent. Mathematically these sum to a 7 percent average return. However in this case we run out of money 38 months prior to the smooth 7 percent return first example. As we work our way down the table, we see the impact of the sequence in which these returns are earned can have on the longevity of the portfolio. In our bottom row, we can see that if we earn strongly positive returns in the first year of withdrawals, we run out of money at almost 95 years of age, compared to 86.5 years of age in our first scenario.

The point is that a portfolio producing the same average return but varying those returns in when they are earned – the sequence of returns – and making no other changes to the portfolio, will cause us to run out of money faster if we started withdrawing in a year of negative returns.

Our third retirement risk is inflation. In the U.K. inflation might be 5.4 percent, in the U.S. 3.9 percent; there is still tremendous variation both within the countries by year and across the countries. The highest single rate is the United Kingdom was 25 percent in 1975, but wasn’t actually mirrored in any of the other major countries.

We can be fooled by low numbers. We need to think about how to protect retirement income from inflation and we need to think about how inflation ebbs and flows across time periods. We can become indifferent to it in long periods of low inflation such as we have experienced recently, but the risk of inflation can be quite dramatic and is real over the long term.

How Does “Pensionizing” Provide Protection from Retirement Risks?

Product allocation is the process of deciding how much of your nest egg should be invested in financial instruments that protect against these three risks; longevity risk, sequence of returns risk, and inflation risk. An optimum product allocation strategy is driven by diametrically opposed priorities: the security and sustainability of desired income for a retiree versus the estate value for their heirs and beneficiaries.

We can think about product allocation as conceptually similar to asset allocation in the accumulation stage where we support risk versus return tradeoffs. In retirement product allocation, we tradeoff income today versus a financial legacy in the future.

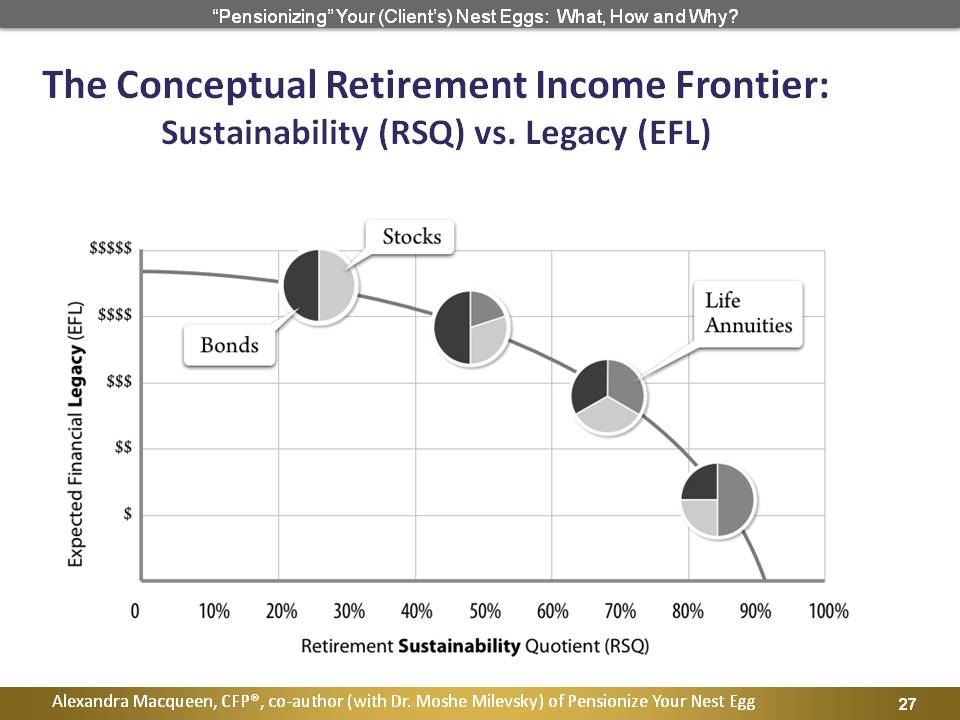

Our product allocation frontier is plotted along a frontier which we call the Retirement Sustainability Quotient (RSQ), which is a measure of the likelihood that a given mix of products and assets will provide desired lifetime income in retirement, or the expected bequest of a financial legacy value, in today’s dollars. Product allocation can protect against retirement risks by mixing and matching different financial products.

Let’s think about the available products to provide income in retirement and how we might compare and contrast them in terms of how they can protect against these risks for retirees.

In the above chart, our first product category is “Systematic Withdrawal Plan” or just “Investments.” We can see how it scales in terms of protecting for longevity, sequence, inflation, liquidity, legacy, and fees and expenses, compared to using a lifetime annuity, whether immediate or deferred. We can see that the annuity provides longevity protection and provides sequence of returns protection, compared to the investment portfolio which provides neither.

Our last product category is the products that are a hybrid of the investment portfolio and the lifetime annuity, so we can think about the available product categories as existing on a spectrum or in three silos. The annuity provides lifetime guaranteed income at the expense of liquidity and the expense of legacy. The investment portfolio provides inflation protection on liquidity and a legacy value at the expense of longevity protection and sequence of returns protection. In the middle we have this hybrid sector which attempts to provide some benefits across the spectrum. So we have longevity protection, sequence of returns protection, and we’ve retained legacy value. In sum, there is no single product or category of product that dominates across all the risk features. Each product partially or fully hedges risks, each product offers different costs and as tradeoffs.

So how do you allocate a client’s investable wealth across these products? We can plot product allocation along a frontier, which is similar to the asset location frontier.

On the bottom axis, or the X-axis, we have the RSQ which measures the likelihood that the client’s retirement income plan is sustainable over their expected lifetime. On the Y-axis we have something called the Expected Financial Legacy (EFL) which is a dollar figure that is the value today of a client’s plan.

We can see that on the top left the allocation is only between stocks and bonds; as we progress right, we start to add annuities. As we add annuities to the retirement income plan, thus sustainability of the plan is increased. So we’re moving up the RSQ scale at the expense of the EFL.

In mathematical terms, an expected value is what we think of as a probability weighted average of all possible values. So expected value doesn’t mean guaranteed value; we’re not using it colloquially, but saying this is the value that the plan has if the client was to take into account all probabilities around their survival over their expected lifetime. It’s generated by an algorithm.

Case Studies for Pensionizing a Nest Egg

Say we have a retiree with three potential retirement income plans.

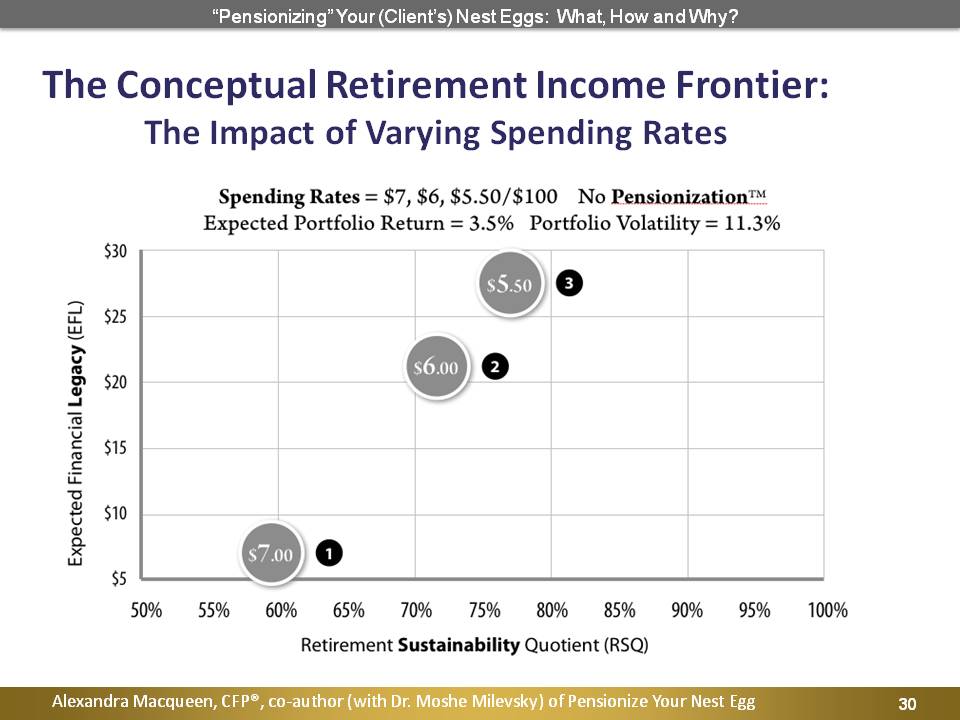

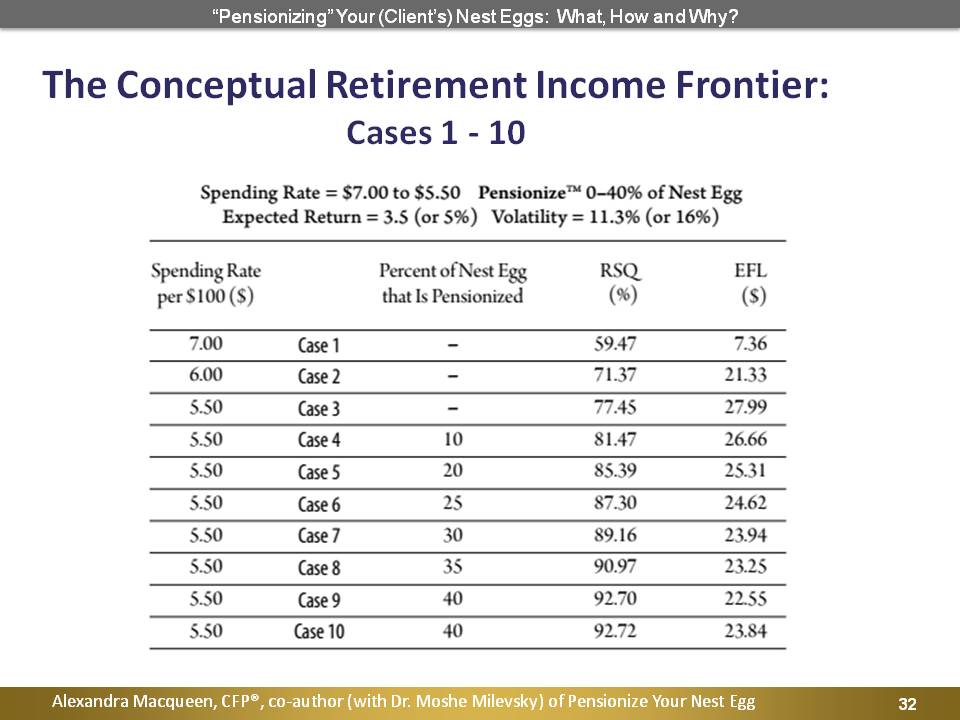

First, we’re going to focus on spending rates. In Case No. 1, if our retiree plans to spend 7 percent per year, the sustainability value of that plan is just around 60 percent, or essentially a 40 percent chance of failure. In other words, the EFL for this case is quite low.

In Case No. 2 the impact of spending 6 percent per year instead of 7 percent moves the expected financial legacy up to just over $20 per $100 of portfolio, and the sustainability value jumps up to over 70 percent. In our third case, spending is bumped down to $5.50 per $100 of portfolio, and you can see the impact on both the sustainability quotient and the EFL.

The point of showing these is to demonstrate that spending rates are very foundational in determining the sustainability of a portfolio. There is no magic that you or I can do to make a portfolio sustainable when given a high spending rate.

In Cases 4-10, by allocating 10, 20, 25, 30, 35, and 40 percent of the portfolio to a lifetime annuity, you increase the client’s sustainability value, but at the expense of their expected financial legacy. This slide demonstrates the impacts of adding annuitized income on the sustainability and the legacy value of different retirement income plans.

When we add annuitized income to a portfolio, which is the definition of pensionizing a portfolio, you can then reposition the remaining assets to take on more risk. The sustainability value moves from approximately 60 percent up to approximately 93 percent, leaving a financial legacy value of 24%. All we’ve done is used product allocation to allocate varying amounts of those dollars in their nest egg to financial products that provide a sustainable income over their expected lifetime at a cost to their financial legacy.

The Implied Longevity Yield

What choices and behaviors increase sustainability? Remember, longevity is a risk that is present for retirees who do not have guaranteed retirement income, where we live a very long time beyond what we’ve planned for, beyond what our assets might support, depending on your withdrawal rate.

That risk is growing. So the choices and behaviors that increase sustainability are:

- Spend less. So we’ve showed mathematically the impact of a lower spending rate on a sustainability and legacy of the portfolio, and

- Consider pensionizing a portion of the portfolio. The implications of pensionizing on the asset allocation of the remaining portfolio are you get more legacy and you get more sustainability once you’ve pensionized a sufficient fraction of the nest egg, allowing you to take more risk with the remainder of the portfolio.

Said another way, if the floor income is secure, the remaining portfolio can be repositioned for higher legacy values at no cost to that sustainability value. This is an attempt to tradeoff mathematically or model mathematically if I buy an annuity now or if I buy an annuity later. In other words, what is the yield I need to receive on my invested portfolio that preserves my ability to buy the same annuity income at a later date?

If I’m 65, I don’t want to buy an annuity now, although I am retiring. I want to think about buying an annuity at age 70. What is the rate of return I need on my invested assets to ensure that I preserve my capacity to buy the stream of annuitized income that I would like at age 70? What if interest rates change during the time that I’m waiting to buy the annuity?

On the site PensionizeYourNestEgg.com or if you are registered with CANNEX the annuity quoting service (CANNEX.com), there is a tool called, “What if I Wait,” which models the impact of interest rate changes on annuity payouts as well as a tool for calculating the implied longevity yield. There’s also a third tool for illustrating the cost benefit analysis across benefit tradeoffs of pensionizing, which allows you to project if a client buys an annuity at age 65 and lives to an age which is the crossing point between the income a client receives from the annuity that offsets the cost to her estate of purchasing that income. In other words, how many years need to elapse before I have now earned back the income that I received from the annuity which completely replaces the estate value that I expended when I first bought the annuity? It also describes or calculates the probability of living to that age.

There are some deeper dives in the book Pensionize Your Nest Egg that go beyond the concepts that we’ve described here that will allow you to explore more analytic explorations of the value of annuity given changing conditions, given interest rate changes, given the cost of the estate, given survival probability. You may want to explore them more for yourself.

Takeaways for Advisors for Pensionizing Nest Eggs

- Traditional defined benefit pension plans are disappearing. What that means is that you and your clients are increasingly relying on do-it-yourself retirement income solutions.

- The solutions that worked when you were building nest eggs in accumulation are unlikely to be the solutions that will work in decumulation. There may be are scenarios where you don’t need to adjust anything; you can just kind of smoothly move over to withdrawals from a nest egg. However, it’s unlikely.

- Longevity is increasing but it is still highly variable. You can help clients protect themselves from longevity risk. Longevity insurance comes in the form of a lifetime annuity income, but at a cost.

- Consider framing retirement income planning along the frontier which demonstrates the tradeoff between legacy versus sustainability. Have the conversation with your clients that allow them to distinguish what they want to maximize income for as long as they are alive, or if they want to maximize an estate value.

- Analytic tools are available to help you explore and deliver these conversations with clients. Use the tools on the PensionizeYourNestEgg.com site to plot a plan that is suitable for your clients based on their preferences and their choices.