Reverse Mortgages Today

Dr. Robert Merton, a Nobel laureate in economics at MIT, is literally traveling the globe letting folks know that the one asset most retirees have is a home – decade in and decade out, it’s at about 80 percent. If you marry this asset with the fact that they can use a reverse mortgage and it’s a non-recourse loan, then there’s something new to be thinking about in terms of the retirement income crisis that is facing many people who don’t have pensions.

We know that retirees draw down assets as they age, but there is this problem. They have a lot of home equity left at the end. Is there a way to weave that home equity earlier into their retirement plan so they are actually able protect some of their assets and not just be cash poor and house rich?

When you look at how ubiquitous home equity is, you may wonder why it is invisible in retirement planning? For the most part, designations do not test to it. There are a couple of designations that have jumped on board like the Certified Retirement Counselor® (CRC®), but certainly the CFP® designation does not. Broker-dealer compliance officers forbid discussion of housing wealth.

Financial professionals don’t get paid on reverse mortgages. Possibly, it’s just easier to say, “If you run out of money then we’ll turn to your house. We’ll use it as a last resort.” I’ve heard a lot of advisors and retirement counselors also tell people they just need to downsize. One of the things that’s puzzling about this is, if you look at the recent Merrill Lynch Age Wave Study, you find that most retirees really don’t want to downsize. In fact, they’re spending an enormous amount of money – something like $90 billion a year – remodeling. It’s not just remodeling to meet medical needs, but building big gathering rooms so they can have their children and grandchildren together.

Software does not allow illustrations showing what a plan would look like when you incorporate reverse mortgages versus not incorporating. We hear that there are some changes being made and a few software companies are waking up to that, but as a general rule software that illustrates using reverse mortgages in retirement is not available.

Nobel Laureate Robert C. Merton, School of Management Distinguished Professor of Finance from MIT, wrote the following about reverse mortgages: “It is both a stream of income as a hedge, as an asset. It changes from the former to the latter when the people in the house no longer need it. The reverse mortgage recognizes it by saying as long as you’re in the house you pay nothing, even if you live to be 120. When you’re not there, your heirs get the unspent cash from the reverse mortgage and they can sell the house, pay the amount due, keep the difference, or let the bank take the house if the amount owed exceeds the value of the house. That’s a wonderful contract.”

Recent Changes in the Reverse Mortgage Market

If you bring up a reverse mortgage with your clients, they may be shocked. They probably have the same misunderstandings and negative opinions that possibly you do. However, the reverse mortgage market is changing for the better.

The reverse mortgage in the past has always had inherent safeguards, but it was subject to abuse in some cases. So the Reverse Mortgage Stabilization Act of 2013 went a long way to making sure that the possibility of abuse was reduced. So there were four major changes.

- Brakes were put on the amount of equity that can be used. You can’t use too much of it too soon. There are limits on the initial disbursements.

- Before, a reverse mortgage was marketed to and seen as something for people who had reached the end of their financial ropes. But those folks would not even be eligible for a reverse mortgage today because you have to be able to demonstrate willingness and capacity to meet your tax and insurance obligations.

- When you’re working with any Federal Housing Authority (FHA) mortgage, there are mortgage insurance premiums, both upfront and ongoing. If you’re in a position to use your reverse mortgage funds slowly at the outset, your mortgage insurance premium will be discounted to 0.5 percent versus 2.5 percent if you’re using it more aggressively.

- There are now protections for the non-borrowing spouse. There were horror stories when the younger spouse wasn’t on title. The husband would die and she would have to leave the house. That can’t happen any longer. The non-borrowing spouse cannot be displaced in the event of the borrower’s death.

One other development that most people are not aware of is there is now a tremendous secondary market demand for reverse mortgages. They are securitized through Ginnie Mae. People don’t refinance them when the rates go down. We’ll see later, that if you have a line of credit and interest rates go up, that’s when you really want to hold on to it. Because of this market demand, if you can help your clients negotiate interest rates, just like on a forward mortgage, it’s possible for you to negotiate that set-up fee to less than $500. That’s because the demand on the secondary market allows for lender credits which can be applied to the origination fee, the third party fees, and even the upfront mortgage insurance which goes to FHA.

Four things to keep in mind when you get into a discussion with your client about reverse mortgages:

- The borrower never gives up title to the home and the bank doesn’t get the home,

- The borrower will never owe more than the home is worth; it’s non-recourse,

- If there’s equity left over, it will belong to either the borrower or his estate, and

- The borrower never has to make a monthly payment on the principal or the interest until the last one of them dies, moves, or sells. Caveat: the borrower must keep their property obligations current.

Key Features of Reverse Mortgages

- More than 90 percent of reverse mortgages out there are FHA-insured Home Equity Conversion Mortgages (HECMs). This means that, just like an FHA loan on the traditional forward side, there is going to be an upfront mortgage insurance premium added to the loan balance and then an ongoing mortgage insurance.

- Age requirement – one of the borrowers has to be 62. The loan amount available is based on the value of the home and expected interest rate – which is the 10-year swap rate – and your age. But 50 percent is a good rule of thumb for a 62-year-old for right now. If you have a client with a $400,000 house with a $200,000 mortgage, they would be able to transition to a reverse mortgage. They would have roughly $200,000 available and it could serve to pay off that existing mortgage, leaving you with a reverse mortgage where there are no monthly debt payment requirements.

- Ways in which loan proceeds can be received – you can take a lump sum at the outset sometimes. One of the circumstance is paying off a current mortgage. You can set up a line of credit which can be drawn upon in any amount as long as there is available credit. Or you can take periodic payments for a fixed number of periods over the life of the borrower. If you take it for the life of the borrower, you’ve basically annuitized your house to provide what is in effect an annuity payment, although it would end if the borrower leaves the house. You can also combine these various versions.

- Interest rates generally are variable, although there is a fixed rate HECM. Again, the setup fees involve regular mortgage fees. But because it’s an FHA mortgage, there is an initial mortgage insurance premium. The cost of that varies based on usage. The borrower cannot be evicted, except for failure to pay property tax or homeowner’s insurance or failure to maintain the home. Dr. Merton’s favorite point is HECM debt is non-recourse. Repayment is not due until the last borrower has permanently left the home.

Case Studies: Reduce Sequence of Returns Risk with a Reverse Mortgage

Now we’ll move on to the case studies and think about ways to prepare for the unknown. Jamie Hopkins Esq., MBA, LLM, CLU®, RICP®, is Associate Professor of Taxation at The American College of Financial Services in the Retirement Income Program and is Co-director of the New York Life Center for Retirement Income. He wrote an article in Forbes that is a manifesto for thinking about housing in retirement. “The lack of focus on home on home equity and retirement income planning is nothing short of a complete failure to properly plan and utilize all available retirement assets. This needs to change immediately because strategic uses of home equity, especially reverse mortgages, can save many people from financial failure in retirement and help stem the overall retirement income crisis facing Americans.”

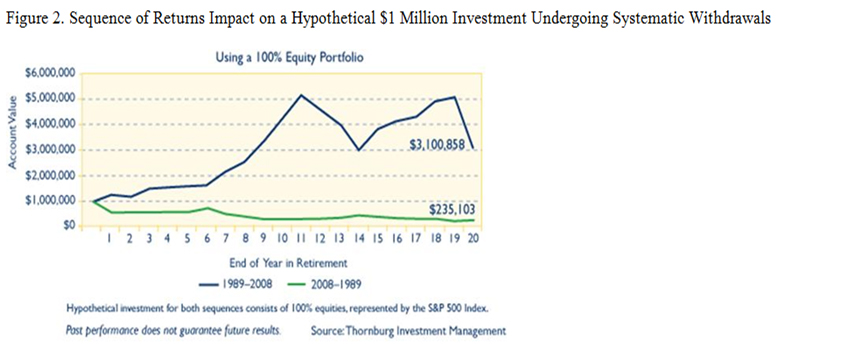

Sequence of returns risk means that down markets matter, particularly if they happen early in retirement. Here’s an example from Thornburg of the same portfolio, taking systematic withdrawals. The years of returns are just inverted here. So it’s 1989-2008 in blue and the same returns inverted from 2008-1989, and continuing to take those systematic withdrawals. 2008-1989 started bear market and 1989-2008 has sustained bull market.

You may be saying to yourself, “Well, why wouldn’t I just not set up a home equity line of credit (HELOC) instead of a reverse mortgage and get the same result?” There are a few reasons.

- In 2004-2006 there were billions upon billions of interest only HELOCs written. It seemed like a good idea to just take out a HELOC and just make payments on the interest. The problem is the draw period does end, and then principal and interest payments begin. But because the principal has not been reduced in that first 10 years, there’s a compressed principal payback and considerable payment shock can ensure.

- HELOCs are not as reliable as a HECM line of credit because it can be frozen, reduced, or cancelled at the bank’s whim usually just when cash flow is most stressed. I’ve heard from so many planners about this. Just when their clients needed help in 2008-2009 their HELOCs were cancelled. In fact, in June 2008 over $6 billion in HELOC credit was frozen. HELOC credit capacity is completely arbitrary. It can be reduced.

- HECM credit lines keep up with inflation regardless of what collateral value becomes. The HECM line of credit grows in borrowing capacity and that cannot be changed, even if home values drop. Once you set up a HECM line of credit, if the home value sinks, it has nothing to do with the loan. They only look at the value of the house at the beginning. There is never a reassessment of that during the loan.

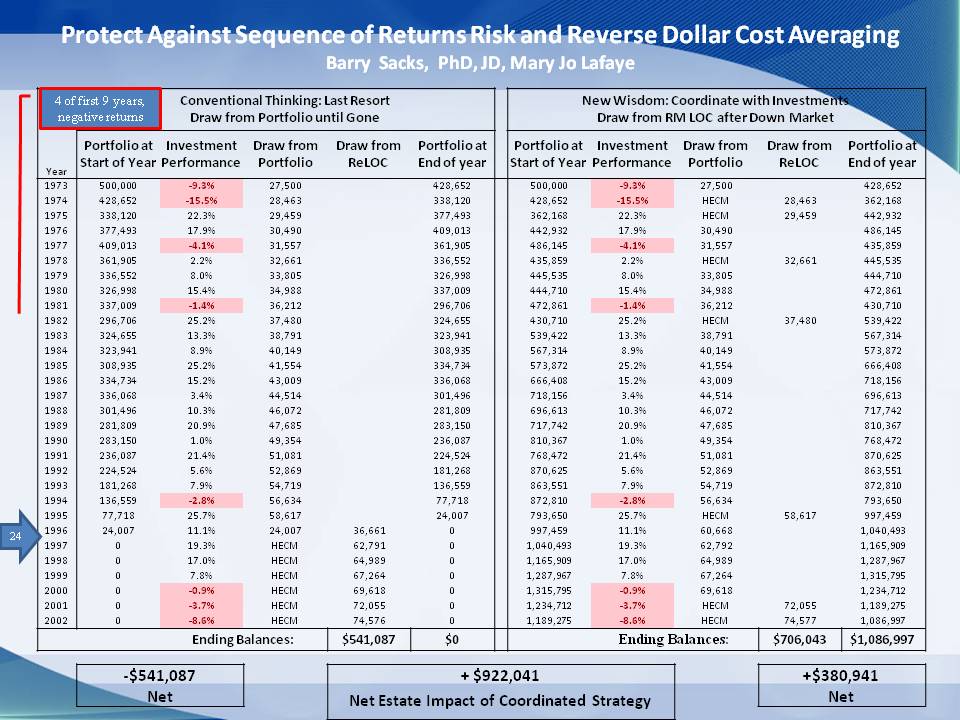

Dr. Barry Sacks has a PhD in physics in MIT and a JD from Harvard and was a tax and pension lawyer for 40 years. He started thinking about this back in the early 2000s, as he was approaching his own retirement. He was thinking about, “What if I didn’t have to sell my investments after a market downturn?” He developed a strategy where on January 1st, he takes a look at setting aside the upcoming year’s expenses. If the portfolio was up last year, he’s going to go ahead and take his draws from his portfolio. But if the portfolio was down, he’s going to take his draws from a home equity conversion mortgage, reverse mortgage, line of credit.

Dr. Sacks has published in the Retirement Management Journal how to protect against sequence of returns risk and reverse dollar cost averaging in conjunction with Mary Jo Lafaye. If in the previous year the market was in negative territory, use the HECM. He compares the conventional wisdom (use up all your portfolio, turn to your house as a last resort) to the new wisdom (coordinate draws from your HECM, depending on what the market has done). He used a historical portfolio performance from 1979-2002 because he wanted to demonstrate what poor early sequence of returns could do to a portfolio under the stress of systematic withdrawals. As you can see, he starts at $27,500 and, regardless of what the portfolio is doing, he takes draws that are keeping up with inflation and constant purchasing power after that initial draw. Inflation was 3 percent in this example.

As you can see, the client runs out of money basically on year 24, and now we’re hoping the reverse mortgage still exists. He’s going to take out a reverse mortgage and hope he can get draws of this magnitude from your reverse mortgage 25 years down the road. Using conventional wisdom, the client has zero in the portfolio and has an ending balance of $541.87. Compare this to the new wisdom, where in every year following a negative performance, the portfolio rests and the client draws from the HECM. You can see it’s the same draws, but just from the HECM. At the end, we get an ending balance of $706.00 on your reverse mortgage.

But look at what the portfolio did; it’s $1 million. It’s zero using the conventional wisdom of home equity as a last resort. So you have to ask yourself, would the kids rather have the money or the house? There is a $922,000 spread differential to the estate of one strategy over the other. Pretty compelling numbers.

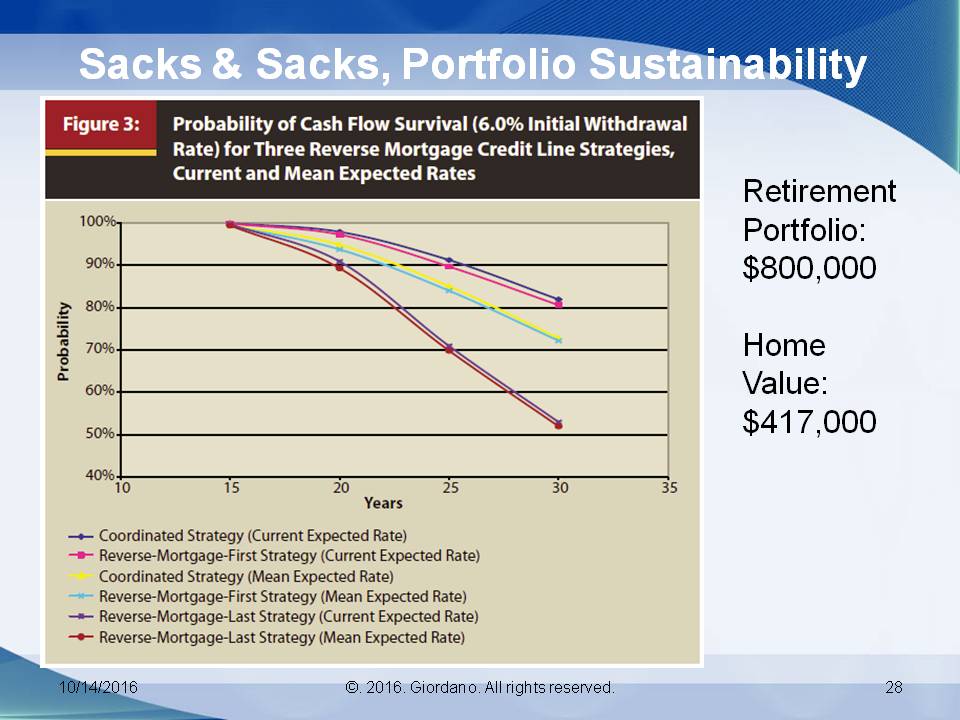

Dr. Sacks and his brother Dr. Steven Sacks wrote a paper in 2012 in the Journal of Financial Planning. They looked at different initial withdrawal rates. When you start at 4 percent, the probability is pretty high that you’re going to have enough money to last. We’re just showing it at a 6 percent initial withdrawal rate. It demonstrates that, if you use the coordinated strategy, which is using your HECM line of credit in the years following a downturn in the market, the probability of having cash flow survival is way up here. If you use a reverse mortgage as a last resort the probability is way down here.

It gives confidence that your client can spend maybe more than the lower initial withdrawal rate. There are findings where there are substantial increases in the cash flow survival probability when home equity is not used as the last resort. Residual wealth after 30 years, even if you take into account the debt on the home, is also twice as likely to be larger. They did find a high ratio to home value to financial portfolio allows for greater sustainability.

Case Study: Grey Divorce and Reverse Mortgages

Unfortunately, more married Americans over the age of 50 are calling it quits. It’s more than double for those over the age 65. This creates a problem, since in order to divide assets the marital home often must be sold, since the departing spouse may not want or qualify for mortgage debt on a new house. In grey divorce, it’s especially dangerous to divest retirement funds for home purchase or take on traditional mortgage that stresses resources.

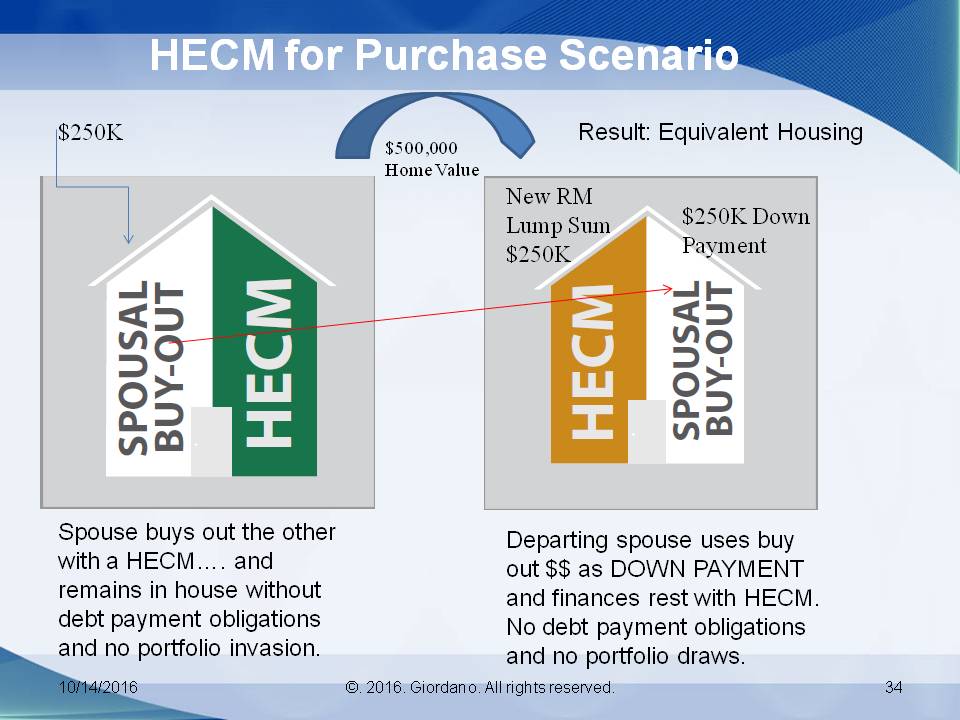

So even if the marital house is sold and the proceeds are used to purchase new homes for both parties, this could represent an unpleasant step down for both. Let’s say they had a $600,000 house and they both get $300,000. They don’t want a mortgage. They don’t want to invade their portfolio. You may not know that you can use a “reverse mortgage for purchase”. Let’s see how that would work in a couple of grey divorce scenarios.

In the first example, the spouse buys out the other spouse in a home equity conversation mortgage and gets to remain in the house without debt payment obligations and no portfolio invasion. The wife puts a HECM on the $500,000.

Following our 50 percent rule, the husband now has $250,000. He can take out a mortgage, move to a different part of the country, or go into his portfolio. He can also settle for a house that costs $250,000 while his wife continues to live in the marital home. But he can also take that $250,000 and leverage it now with his own reverse mortgage – a HECM for Purchase. That will provide $250,000 in financing. So he takes $250,000 down as his monetary investment on his part and will be able to leverage the rest of that purchase price with a HECM for Purchase.

So the departing spouse uses the buyout dollars as a down payment and finances the rest with a HECM. No debt payment obligations are required and no portfolio draws.

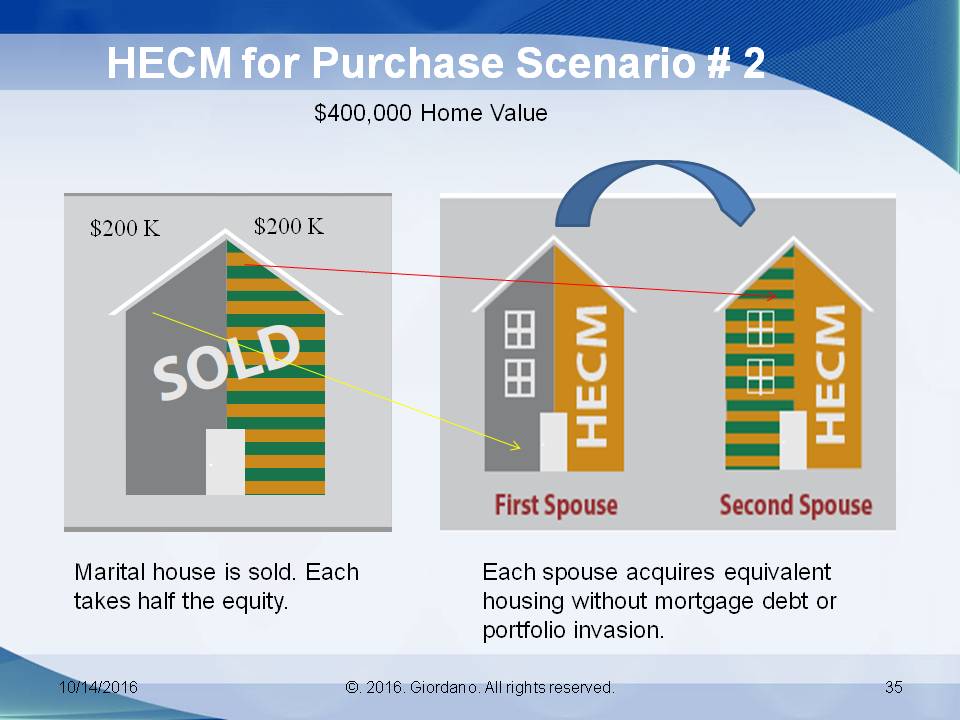

Now this time let’s use a $400,000 house.

Let’s say the marital home is sold and each takes $200,000. The first spouse is going to put that $200,000 down as a down payment and is going to leverage buying a $400,000 house by using a HECM for Purchase. She comes to the closing table with another $200,000 and she’ll be able to live there without making payments on the principle or interest until she dies, moves, or sells.

The husband takes his $200,000 and applies it as a down payment toward his home. He leverages that $200,000 in cash with a HECM for Purchase transaction, which will allow him to buy a $400,000 house. So now everybody has been restored to the kind of housing they’re used to, but more importantly, it’s equitable housing. Whether they want to let the interest on the reverse mortgage ride or not is up to them.

Case Study: Long-term Care and a HECM Line of Credit

In this case there are no long-term care premiums. Instead, you establish a HECM line of credit at retirement outset and then you use it only if you need it. It’s going to function like insurance. The HECM line of credit is hedged against an inflation and declining home values because its future value is guaranteed.

Any HECM transaction where there is an existing line of credit is contractually obligated to increase that line of credit every single month at a rate set at closing. It cannot be changed. If you’re in the habit of telling your clients to wait until they get older and they’ll get more money, guess what? There have been FHA changes in the last 10 years that have reduced the percentage available three times and raised the cost of insurance twice in the past 10 years.

When interest rates rise, funds available on the HCM line of credit decrease. You want to get into a reverse mortgage when interest rates are low if you possibly can. You may not qualify for a reverse mortgage if your financial situation changes down the road. Carrying costs are basically nil for a line of credit. If you haven’t drawn the money, it’s not incurring interest and MIP charges.

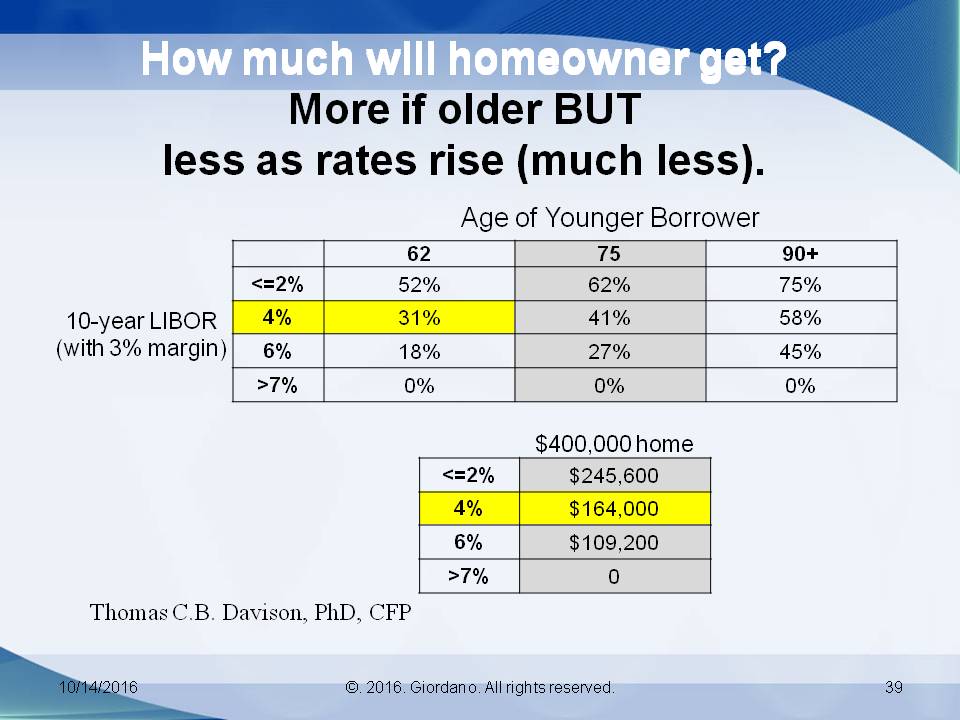

So how much will the borrower get? It’s true they can get a little more if they’re older, but that advantage gets erased as rates rise. So the point of this is that the amount of money you’re eligible for in a reverse mortgage is much more sensitive to interest rates than to age.

At a 4 percent rate, a 62-year-old would be eligible for 31 percent. This is a higher rate. This is where we are today. But a 75-year-old would only be eligible for 41 percent.

Look at the difference when rates change on a $400,000 house for a 62-year-old – what the actual dollars are. You move from this interest rate and are eligible for $245,000. But if rates go up, you’re only eligible for $164,000. So please don’t let anybody tell you, “I’ll just wait until I’m older and I’ll get more money.” That is a really risky strategy.

Case Study: Using a Reverse Mortgage to Maximize Social Security

Say we have a single woman, retired, turning 62, and expects to live to age 95. Living expenses are $87,000 per year. If she were to begin her Social Security at full retirement age, it would be $2,500 a month. She does have a pension of $5,000 a month. She has $500,000 in an IRA. She would be eligible for $240,000 from her reverse mortgage line of credit. She is a California resident, which means she gets whacked on taxes.

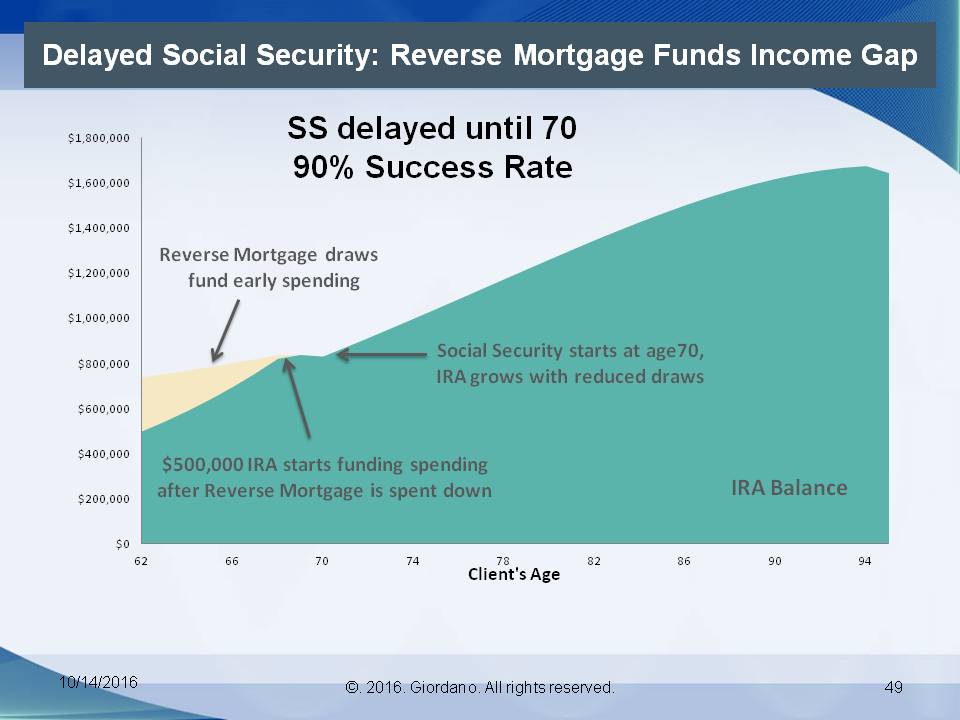

So we know deferring Social Security to age 70 provides 132 percent of the full retirement age benefits, so a lot of folks would understand that that can make a big improvement in retirement income security. If she were to start taking her Social Security at age 62 and not have a reverse mortgage, and draw on her IRA, in 95 percent of her lifetime she’s going to run out of money. That doesn’t give her much confidence.

But what if she delayed her Social Security and instead took draws from her reverse mortgage for income? It lasts until age 68 and then for two years she has to take all of her spending net of her pension from her IRA. But at age 70, that big nice Social Security check starts to show up. So why does this work so well? She has more assets to spend. She added $240,000 of home equity to her $500,000 IRA. She allowed her Social Security to be delayed by the reverse mortgage funding six years of spending. The reverse mortgage funded that first six years of spending.

Her investment portfolio was untouched until age 68, so she got six extra years of growth before she started withdrawing. Reduced sequence risk reduced the possibility that early on she was going to take withdrawals when bad returns hit early. Her investment portfolio draws after age 70 were reduced by the largest possible Social Security contribution.

If you’ve not thought about that, like all mortgages, proceeds from a reverse mortgage is debt. It’s not income, so you don’t pay taxes on it. A reverse mortgage dollar in a 33 percent tax bracket has the spending power of $1.50 if she’d taken it from an IRA she had to pay taxes on. It’s debt, but it’s real spending money at the moment.