Curtis Cloke, CLTC, LUTCF, RICP, Award-winning financial professional and retirement income expert, trainer, and speaker

Editor’s note: This article is an adaptation of the live webinar delivered by Curtis Cloke in 2017. His comments have been edited for clarity and length.

You can read the summary article here as part of the 3rd Qtr 2017 Retirement InSight and Trends Newsletter, worth 1.0 CE when read in its entirety (after passing the online quiz.

You may also choose to take the full length course The Holy Grail of Retirement: How to increase income and growth while improving liquidity – Curtis Cloke for 1.0 hours continuing education (CE) credit.

By Curtis V. Cloke, CLTC, LUTCF, RICP®, Founder of Thrive Income Distribution System, LLC

There is a bridge in Honduras where no roads lead to it, and there’s no river running under it. A cyclone came through that was so severe that it took out all the roads that led to the bridge. It also actually moved an entire river.

This bridge is metaphoric for what might happen if we continue to do the things the way we have done over the last 30 to 50 years of retirement income planning. It was a model that allocated a significant amount of assets to bonds, where you could expect somewhere about a 5 to 6 percent income yield consistently over time. Given this low-interest rate environment, we are in a 30-year trench that’s probably going to be quite different. Also, now we have the risk of equity losses in bond instruments if we are not careful. We cannot do what we have always done in the past because the cyclone of increasing longevity, metaphorically, has come through the financial planning industry. We must realize that those methods are rendered useless just as the bridge in Honduras.

The 2012 mortality tables by the Society of Actuaries were published in 2014. The last time the tables were released was back in 2000. There are 12 years between the previous numbers and the current numbers. Men who reach age 65 in America are on average living to age 86.6, and women to age 88.8, for an increase of 2.2 years during the prior 12 years. If we were to live 30, 35 or 45 years in retirement, and every 12 years we add a 2.5-year extension to our life, we can see how disruptive this is as we go through more market cycles.

When people live longer, there are body parts that go bad and illnesses that happen, which means we must maintain our health with more expense before we pass on. When we extend life, it is additional pressure, of course, as we all know, on our portfolios.

The Importance of Liquidity in Retirement

There are two types of liquidity: discretionary spending liquidity and investment allocation liquidity. I can move money from stock to a bond or bond to a stock, but it does not necessarily mean that I can take it out.

Let’s pretend Mary and John have been married 35 years. They worked for 40 years. They have $28,000 in their checking account. It is their emergency fund, their regular management of cash flow needs. Together, they have accumulated $1 million in their 401(k) plans.

There are two ways to address withdrawal rates. One is a withdrawal rate that would be predictable, static, and provides a level income in good and bad markets with a bit more safety. If you are willing to vary your income as markets ebb and flow, we can eke up your withdrawal rates a little higher.

Now let’s pretend John and Mary say, “No, I do not want to get into a place where I have to unpredictably lower my income standards with some market variability. Let’s use a safe withdrawal rate.”

We will not get into a debate about whether the safe withdrawal rate is 5 or 4 or 3 or 2 percent. Academics today will argue the 4 percent rule is dead on a static basis, that it is more like 2.2% or 3.0%. For this example, let’s assume it is 3%.

If John and Mary are average mass affluent clients, they might need $90,000 of income. Let’s pretend they have $30,000 in annual pension income and $30,000 in Social Security. If they have $1 million and 3% is the safe withdrawal rate, then they make it. Here’s the problem. Two years later when Mary says to John, “I want to take the grandkids to Disneyworld and the $15,000 we need is not in the $90,000 budget.”

If all these things were true, how much discretionary liquidity or spending capability can John and Mary get without putting risk pressure on their withdrawal rates? Everybody understands the answer to that is zero. The entire $1 million must be held hostage to generate the earnings needed to provide a safe withdrawal over the lifetime of their expected longevity.

This issue of control or the fear of missing out is something we need to address. We sometimes forget that we should preserve dollars, especially for those who have a much longer time to live after the first spouse dies. This situation becomes a significant woman’s issue to prevent making bad decisions while they are both still alive that can jeopardize that surviving spouse.

Take Key Risks Off the Table

There are five top risks out of 18 retirement risks that are paramount to mitigate:

- Longevity.

- Health insurance premiums and out of pocket healthcare costs, not including the long-term care issues that might happen later in life.

- Non-medical inflation.

- Sequence of returns risk.

- Market volatility for the accumulation of assets.

Too often I see software that asks you to put in a monthly or an annual income amount number and some inflation factor, but they don’t differentiate between the portion of that cashflow for healthcare that may need to be inflated at 6 or 7 or 8 percent and the remainder of that cashflow need that’s not medically related that might only need to be inflated 2, 3 or 4 percent. Our calculations need to separate the cashflows in retirement to directly reflect a different level of inflation for medical costs versus non-medical costs.

There are three basic retirement income approaches that address some combination of retirement risks – the systematic withdrawal income plan, bucket or ladder approach, and the income floor strategy.

With a systematic withdrawal income plan, you basically make many assumptions. You collect all the data and the intellect from the client through a discovery process and then plug it in. You agree to what kind of forecast to save and then you Monte Carlo test that to determine the success or failure. None of that is really going to happen the way you said because Monte Carlo completely ignores black swan events.

When you do that, you are assuming and consuming, crossing fingers and toes, hoping it all works out. Of course, you are hyper-sensitive as an advisor. You are watching things on a quarterly basis, you are meeting with clients regularly, and you are managing these things. However, it is an ‘assume and consume’ strategy.

The second strategy is the bucket or ladder approach, or a progressive, “time segments of money” approach. It can be non-guaranteed sources of bucket strategies or a combination of at-risk and promise-based or guarantee-based bucket strategies. Nothing wrong with either one of these two strategies.

However, the strategy I want to highlight is the income floor strategy, where guaranteed income solutions are added to that floor, and how the possibilities might be that we can create more growth, more liquidity, and legacy from that result.

Wade Pfau, Ph.D. wrote, “For retirement income, we must step away from the notion that either investments or insurance alone will best serve retirees. More emphasis needs to be on the basic forms of insurance products and how they behave as part of an integrated retirement income plan.”

Let’s pretend that I have two tools from my workshop. I have a shovel in the left hand. Down the wooden handle of the shovel, I am going to put the phrase “traditional investments.” I have a hammer in the right hand, and down the wooden handle of the hammer, I inscribe the word “annuity.”.

There are 42 types of annuities. Annuities can either be taxed on an ordinary basis, or on a last-in or first-out basis. Did you know that certain types of annuities can be taxed differently, like first-in, blend-out? So, it is not first-in, first-out. It is not last-in, first-out. It is first-in, blend-out.

There are components of certain types of annuities that also have either no commission at all or very low commission if those are the types the advisor is providing. So, these products do not have to be conflicted in any way, but they can create significant benefits by allocating income guarantees for a particular set of cases.

Let’s pretend for a minute that you are in a discovery process with your client. The client metaphorically reaches into his pocket, and he pulls out a 16-penny nail. The “annuity” hammer is specifically and specially designed to put the nail in the wall.

However, let’s pretend for a minute that we have an advisor, even though he sees the nail and knows what the nail means, he says, “I hate hammers,” and he throws the hammer away. He goes over to the wall, and he picks up a shovel because he likes shovels better. He tries to nail the nail with the shovel.

Now, further down in the discovery process, he is talking to the spouse, and she says, “We need to dig a hole.” Just in the same way, let’s pretend we are talking to some insurance guy who does not use investments. He hates shovels, and he says, “I think I will go get a hammer.” Well, he would look pretty stupid digging the hole if he is grabbing the hammer and losing the shovel.

Here’s the point: All these products have specific purposes. Often, when it comes to annuities, we hear about the bad uses and the bad Joes in the industry. We do not hear the good stories often enough about what these products do. It is important to understand what each product does uniquely and separately to mitigate risk in retirement. So, I’m not talking about a broad sense of annuity products. I’m talking about a very specialized set of annuity products that create tremendous value to the consumer.

If I want to guarantee that longevity risk is taken off the table for a block of the income, I certainly can’t guarantee anything unless I do it with an insurance-guaranteed product. I certainly can’t mitigate hyperinflation in combination with that if I do not use equities. I should have equities in the portfolio.

Divide and Conquer*

There are four things that we would like for our assets on the day of retirement.

- Preserve our wealth for heirs.

- Grow it slowly over time.

- Distribute from it to combination with secure income such as Social Security, pension and maybe rental income.

- Inflate the distributions to keep pace with inflation.

Altogether, the four things we want is to grow and preserve our dollars while distributing from those dollars and inflating that distribution. They are conflicting goals. They are difficult to do.

If I had bought a piece of farm land – and I thought about this a long time ago being from Iowa – that produced commodity crops in any state in the country 100 years ago, I would have met all four of those goals simply with ownership of a commodity field.

I have been considering this now for over 18 years. The further ahead of time that I purchase income, the better the performance, the less capital is used, and the faster I can generate with the remaining income needed with equity growth. I have been buying layers and layers of income over time as I approach my retirement. I am only 54 today, so I have been at this quite some time. I will not have to worry about that income being there because it is pension-like income.

The remainder of the retirement portfolio is then available for liquidity and discretionary income for things like taking grandkids to Disneyworld, and growth. I have created less dependency on a constrained portfolio for a safe withdrawal rate and can, therefore, chase more growth, and then I can start to focus some dollars on building a legacy to protect the surviving spouse.

We call this the defensive approach in combination with an offensive approach. I need defense and offense to build a portfolio to last a lifetime. My good friend, Tom Hegna, talks about “paychecks and playchecks”. This is what we mean about “divide and conquer.”

There are many goals to achieve in retirement income: create reliable income, meet or beat inflation, and minimize taxes. Unfortunately, a lot of the research and testing that’s done today ignores fees and taxes. There are income products that create huge tax efficiency and have no ongoing drag of fees whatsoever. If I ignore fees and taxes, I will miss some of the greatest benefits of testing an income floor that these products merit out.

We designed software for our office so income products were fully capsulated and recognized, as we tested with a fiduciary standard approach, which one of these combinations of product allocations together give us the most income for the least dollars so that we could grow and provide liquidity with the maximum amount of dollars in an unconstrained way. We want to max returns but not with too much risk based on a client’s risk tolerance and legacy needed for the surviving spouse.

Income-Guarantees Require Insurance

Income-guaranteed products require insurance. Often there’s a misbelief or belief that annuity products are only as good as the carrier themselves. That is not correct.

The FDIC provides deposit insurance to depositors of banks. For insurance companies, specific products are required to have something called statutory capital reserves.

The statutory capital reserve is valued every single quarter, reported and reviewed by the NAIC, the National Association of Insurance Commissioners. The present value of each one of these income streams is valued just like life insurance and disability, car insurance and homeowners’ insurance.

Insurance companies must prove that they are retaining, off the general ledger, $1.05 for every $1.00 in statutory capital reserves. That means that when their out-go versus their in-go minus the capital reserves is at a deficit, they fail and are taken over by the insurance department of their state.

However, those statutory capital reserves have been untouched, and they are there so the insurance department can take them over while finding a suitable carrier takeover for that block of promises. Those dollars are there to make good on those payments. There’s also a third layer of protection, a state pool guarantee.

Types of Retirement Income Annuities

Key retirement income annuities today:

- A SPIA is an immediate income annuity.

- A DIA is a single premium deferred income annuity.

- A Qualified Longevity Annuity Contract (QLAC) was approved by the federal government in 2014 that allows us to take some pre-tax dollars and kick them down the road as far as age 85 or at least as far as age 72, if we do not want to take required minimum distributions at age 70½.

Key elements of SPIAs and DIAs:

- They are a spread-based product, so when you get the income payment for the dollars you put in, and you calculate your IRR, there is no ongoing fee drag for these products.

- You can buy an inflation guarantee such as a 1 percent guaranteed increase, a 2 percent, 3 percent, 4 percent, and as high as 6½ percent. There are two products that exist, though I would not use them, that have an index-based adjustment with no cap.

- If I know how to manage the tax benefits for non-qualified after-tax sources, I get tax-exclusion tax treatment, that when applied appropriately, provides a first-in, blend-out tax treatment, which means I can take advantage of all kinds of other tax advantages that I would otherwise miss.

- All these guaranteed income products provide something called mortality credits. When I am 65, I get mostly return of principal and interest off the money invested. When I am age 90, I get very little interest. I am still getting my principal back until it’s paid back, but now I am getting many more mortality credits because some people in the insurance pool are living, and some are dying.

Guaranteed income products allow you to “buy income and invest the difference”* more aggressively.

A Retirement Income Dashboard and a Case Study

We focus on four quadrants.

- The investable net worth that addresses, “Am I running out?”

- What’s my withdrawal rate? We measure the withdrawal rate from the start of retirement to the end.

- How much discretionary liquidity do you have and what’s the reliability of the income?

- How much of the income that I need in retirement is from promise-based assets versus risk-based assets?

Let’s look at this case study of Larry and Cathy. They are 64 and 63, respectively. We picked longevity ages of 90 and 95 respective of their health and their family histories.

Both have Social Security. We have calculated their full retirement benefit. Larry had already elected a life-only pension before he met with us and it was an irrevocable decision.

They want $138,000 of net income in today’s dollars that need to be grossed up for inflation and taxes. For non-medical cash flows, we are going to assume 3 percent inflation, and for medical cash flows, the health insurance premiums and out of pocket costs, we are going to inflate at 5 percent.

They have non-qualified assets of $1.35 million and qualified assets of $1.535 million. Their home is worth $500,000. Their investable assets, total investable assets are $3,085,000.

Now, take a good look at this case study and think to yourself how difficult it may or may not be to build a retirement plan.

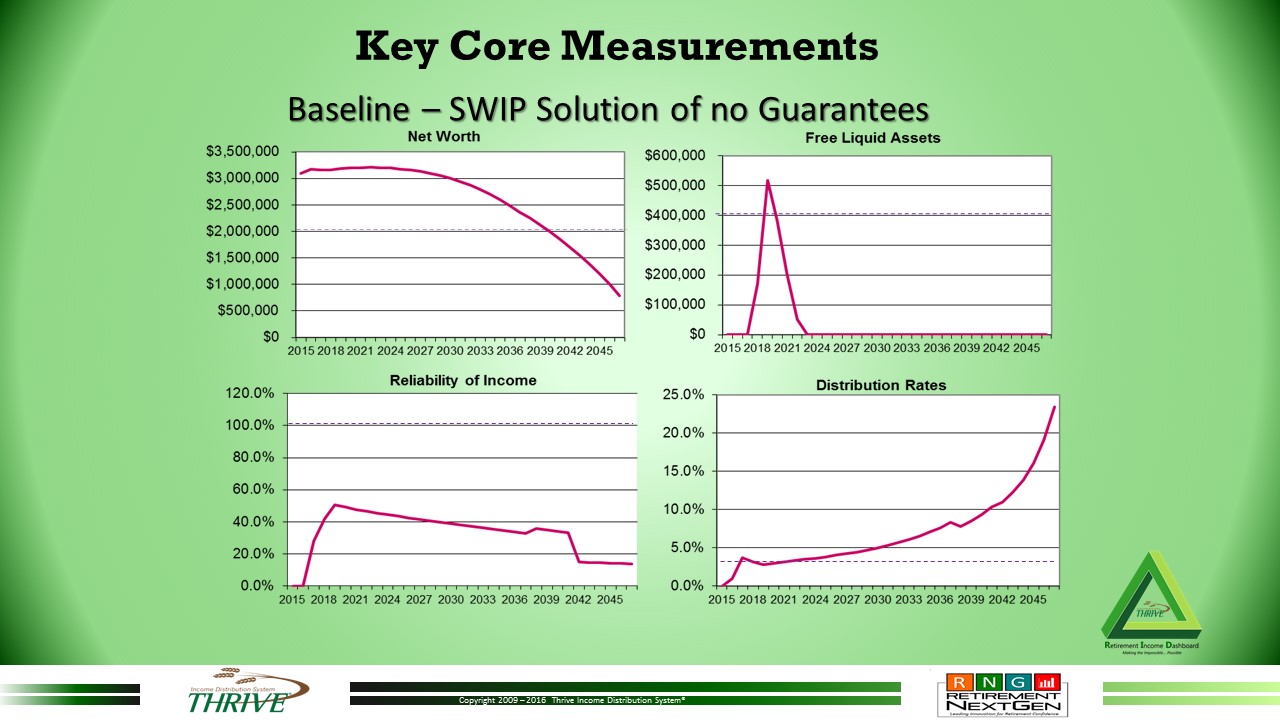

Let’s look at the following quantifiers or core measurements in our software dashboard below. Here we have a baseline or the SWIP (systematic withdrawal income plan) solution. It is a snapshot of the way things would be mathematically framed given the specs, performance, the fees if they are paying for current advice, the withdrawal rate and so forth.

From Thrive Income’s Retirement Next Gen Software. Used with permission.

The first component (upper left) is the net worth column. Larry and Cathy said they want to maintain about a $2 million block of value for their heirs.

The second component (bottom left) is the reliability of income. There’s the 100 percent reliability of income line, that takes into account inflation and taxes over time. The reliability of income redline starts out about 50 percent reliability because half is promise-based (Social Security and life-only pension) versus half is non-promised based, or risk-based (systematic withdrawals). As inflation starts to erode the promised-based income, the reliability of income goes down. Eventually, when one spouse dies, and some Social Security and pension benefits are lost (year 2042), you see that the surviving spouse has a much lower reliability of income than they had when they were both alive.

In the upper right-hand corner, the free liquid assets spike way up in the beginning. However, as soon as our investment performance crosses over our withdrawal rate and we are trying to preserve dollars, you can see that it drops to the floor.

We do not have discretionary liquidity in this particular case for very long. If we took monies out when we thought we had it, it would fall to the floor much more quickly. We really don’t have any discretionary liquidity long-term here whatsoever. Most of the assets must be held hostage to generate the performance needed to keep the withdrawal risk as low as possible.

The bottom-right component is the distribution rate or the withdrawal rate. At 3% it doesn’t take very long until the discretionary liquidity falls to the floor and where we cross above the targeted 3% withdrawal rate. Over time it gets well above 20%. I am not suggesting in the last trifecta of retirement that we cannot have higher withdrawal rates of 3 percent or 4 percent or 5 percent. Certainly, we can, depending on the amount of legacy we’re going to leave behind. However, I am going to suggest to you that this withdrawal picture, if I understand how to use it as an instrument reading a retirement dashboard, is really not safe at all.

Some of the unique and different things we tested to improve their retirement outcomes:

- Delay Social Security and create a bridge of income, so we did not have unsafe withdraw rates in the red zone at the front end of retirement by delaying Social Security.

- Created guaranteed income on a period certain basis will often provide low yields, but better yields than you can add in alternatives with very low tax implication.

- Establish an essential income floor using a variety of products. We tested qualified longevity annuity contracts that took some dollars off the table as early as possible and eliminate the risk of distribution risk at the later part of their retirement, while at the same time created some tax efficiency for about 10 to 15 years after age 70½.

- Created these brackets bumping Roth conversions programs. We utilized the tax bracket capacity before age 70½ to exploit at a low tax bracket, Roth conversions, which gives us back a significant amount of RMD control later.

Also, with some of the dollars that are freed up now, we can focus on other things that are important, such as adding a long-term care enhancement to life insurance to take some long-term care risk off the table.

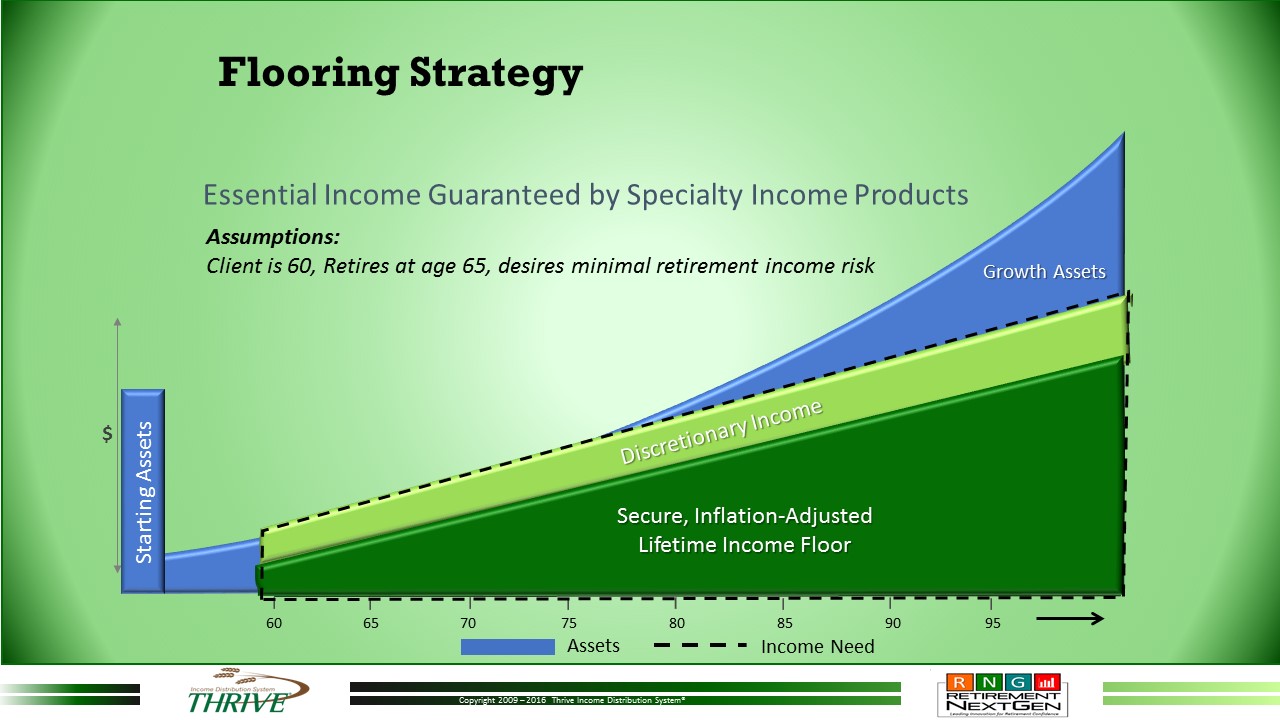

The following is an example of a flooring strategy. The dark green is the essential floor. The top of the lighter green (discretionary income) completes the income floor. Some of the income may be from promise-based assets, some from risk-based assets. The block of blue is long-term growth assets.

From Thrive Income’s Retirement Next Gen Software. Used with permission.

It used to take us many hours to test this mathematically. Finally, we created software so we can do this all in under an hour or 45 minutes in most cases. We will do 18 to 20 iterations with a variety of different products and solutions. Obviously, what we are trying to do is get the risk as low as possible without sacrificing performance.

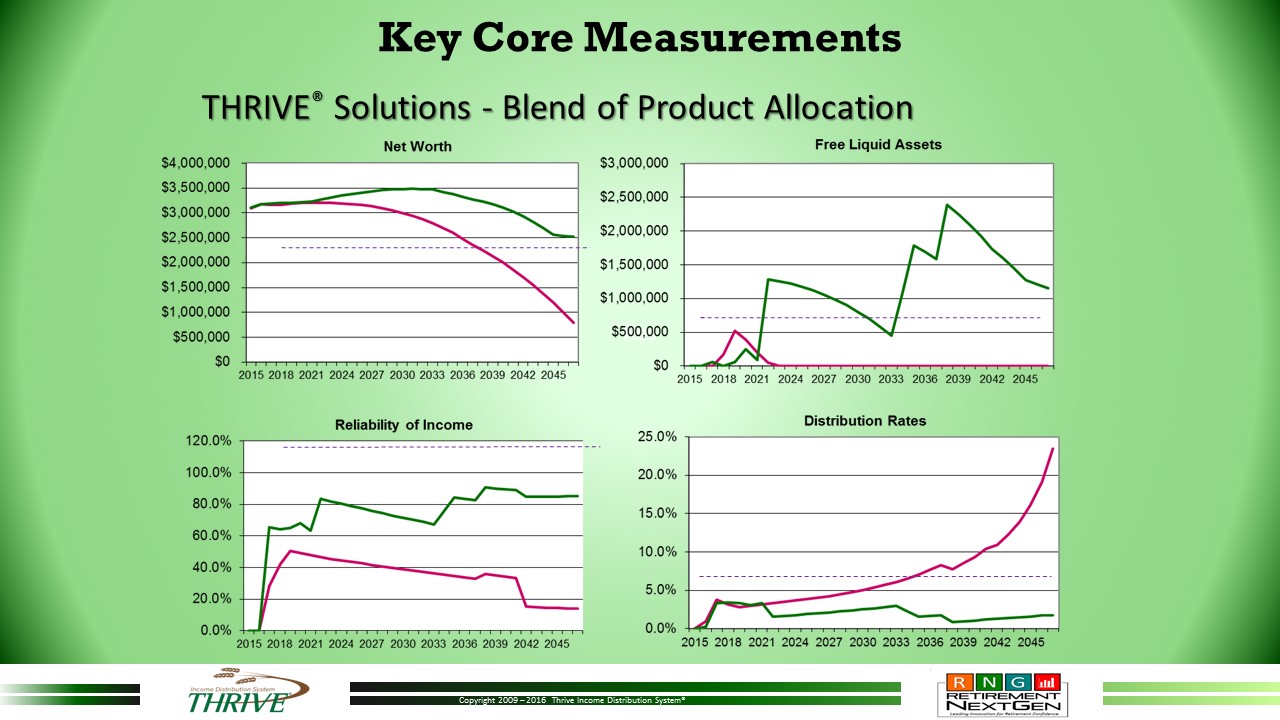

When we applied the solutions mentioned earlier, we see the following improvements (see green lines):

From Thrive Income’s Retirement Next Gen Software. Used with permission.

It is perceived or believed that when we buy income guarantees, we must be sacrificing performance. What if I told you that is absolutely not true? It’s not even true in this interest rate environment. We’ve been testing this for 18 years, and when properly done, it’s never been true. I don’t have to worry about what I’m missing out on to take some dollars from luck to skill. I can do more of what I want to do, and that’s having managed assets and more net worth ($2.5 million green line) without this constrained portfolio for a safe withdrawal rate.

More of the income is now from promised based assets for improved reliability of income, so the client is simply going to be happier. We have also created all kinds of discretionary liquidity (upper right). In fact, once we are past the year 2020 or so, we have about half a million dollars of liquidity or more that are totally unfettered, so the dollars are not held hostage to generate income.

Finally, the distribution rates are in line (bottom right). We have brought that distribution rate from dollars invested in the market way down from dependence on managed assets and the market.

So, this would be a hybrid. Most of our cases are in fact hybrids where we are bringing in the secure inflation-adjusted income floor. We are using bucket strategies with some managed dollars, and then we have long-term growth assets.

The role of a fiduciary is to be unbiased in what we do, embracing all the tools in the toolbox, even though some tools are used more often than others. It means taking an agnostic financial life planning approach as a best-interest standard. It is the math and science of best outcomes and testing that includes fees and taxes. You cannot ignore those things when doing the tests. Let’s get over our fear of missing out. Let’s test it, so we know instead of guess.

*Denotes licensed trademarks of Thrive Income Distributions System, LLC

About Curtis Cloke:

Curtis Cloke, CLTC, LUTCF, RICP, Retirement Income Expert, is an award-winning financial professional and retirement income expert, trainer, and speaker with three decades of experience in income distribution planning.

Curtis actively engages all his audiences with his personable character and genuine care for clients’ retirement needs and concerns. Through his extensive experience, he has perfected the ability to quickly and accurately identify the income needs of all his clients and he’s developed a system-based sales approach that he teaches to advisors. Beyond using annuities to create guaranteed income for life, he shows advisors how to generate the maximum inflation-adjusted income for their clients using the least amount of the portfolio.

Curtis began his career as a financial professional with Prudential Financial. After many successful years with Prudential, he merged with a second firm and then in may of 2014, he founded his own firm, Acuity Financial, Inc. This is where his continues to apply and blend his expertise for his clients by providing advanced retirement income-planning strategies and techniques for financial professionals. Curtis is the developer of the Thrive Income Distribution System®, that provides a contractual solution for inflation-adjusted income utilizing the least amount possible of the client’s portfolio value. He has also developed and provided continuing education training to professionals on many topics relating to retirement and estate- planning strategies.

Are you looking for a retirement speaker for your next conference, consumer event or internal professional development program? Visit the Retirement Speakers Bureau to find leading retirement industry speakers, authors, trainers and professional development experts who can address your audience’s needs and budget.

©2017, Curtis V. Cloke, CLTC, LUTCF, RICP®, Founder of Thrive Income Distribution System, LLC. All rights reserved. Used with permission.