Editor’s note: This article is an adaptation of the live webinar delivered by Lori Bitter in 2019. Her comments have been edited for clarity and length.

You can read the summary article here as part of the 1st Qtr 2019 Retirement InSight and Trends Newsletter, worth 1.0 CE when read in its entirety (after passing the online quiz.)

You may also choose to take the full length course Hacking Longevity: How Three Generations Over 50 are Navigating Longer Lives for 1.0 hour continuing education (CE) credit.

By Lori Bitter, The Business of Aging

There are now three generations of adults over the age of 50 in the United States. The U.S. joins most of the developed nations of the world in increasing life expectancy. According to the Pew Research Center, the world’s centenarian population (those living to age 100) is projected to grow eightfold, from approximately a half a million people in 2015 to 3.7 million in 2050.

The Hacking Longevity study* sought to understand what these three generations of American adults think about living longer lives, how they are planning for extended life, and how longer lives affect traditional lifestage patterns and family dynamics. We wanted to know if patterns were changing; when people become grandparents, when they decide to retire. We wanted to know if these were presenting workplace challenges, and how people were dealing with the finances of a longer life. We really wanted to know about late-life planning, what was going on with giving and legacy, and how the different generations were approaching the end of life.

In the fall of 2017, we did a 2,100-person survey of people ages 33 to 85 to capture Generation X, Baby Boomers, and the Silent Generation. We also did 12 focus groups in two different markets in the U.S. Then we went into peoples’ homes and did interviews in two markets to get more highlights based on what we’d found in the survey.

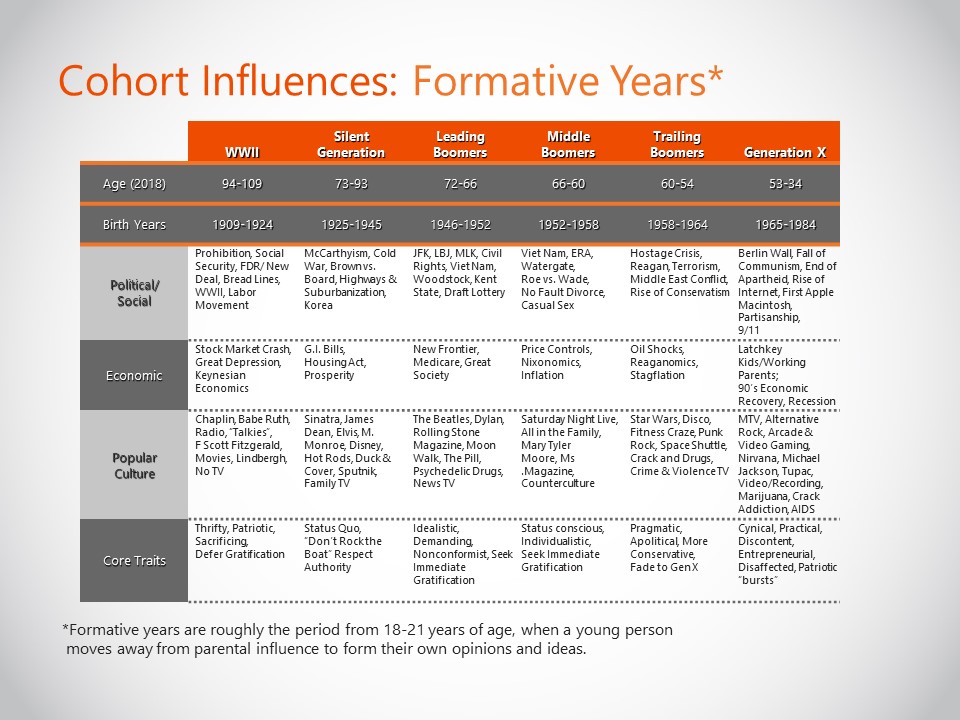

Cohort Influences – the Formative Years

We look at generational cohorts as our first cut at understanding how older consumers behave, because everyone’s formative years are different, depending on what generation they’re born. Your formative years are roughly that period from ages 18 to 21 when, as a young person, you’re separating yourself from your family. You may or may not be going through advanced education, and you’re sorting through what it means to be you and to be forming your own opinions and ideas.

When we look at the older generations, we look at least four generational cohorts. We divided the Baby Boomer cohort, because it’s such a large group of people, into three separate buckets – the leading boomers, the middle boomers, and the trailing boomers. The chart below shows their ages in 2018.

As you probably know better than anyone, the World War II cohort is passing away at unprecedented numbers. Our new “senior” population is the Silent Generation. This year they are 74 to 94 years old.

The chart also gives you an idea of what all the influences were politically, economically, in the popular culture that created those core traits that begin the generational differences.

The World War II cohort was a thrifty, patriotic and sacrificing cohort because they dealt with the stock market crash and the Great Depression. Then you fast-forward to the trailing boomers, who have dealt with things like the rise of terrorism, the oil shocks, Reaganomics. They are more apolitical and slightly more conservative, and they behave much more like Generation X in the marketplace. So, there are key differences based on when you were born.

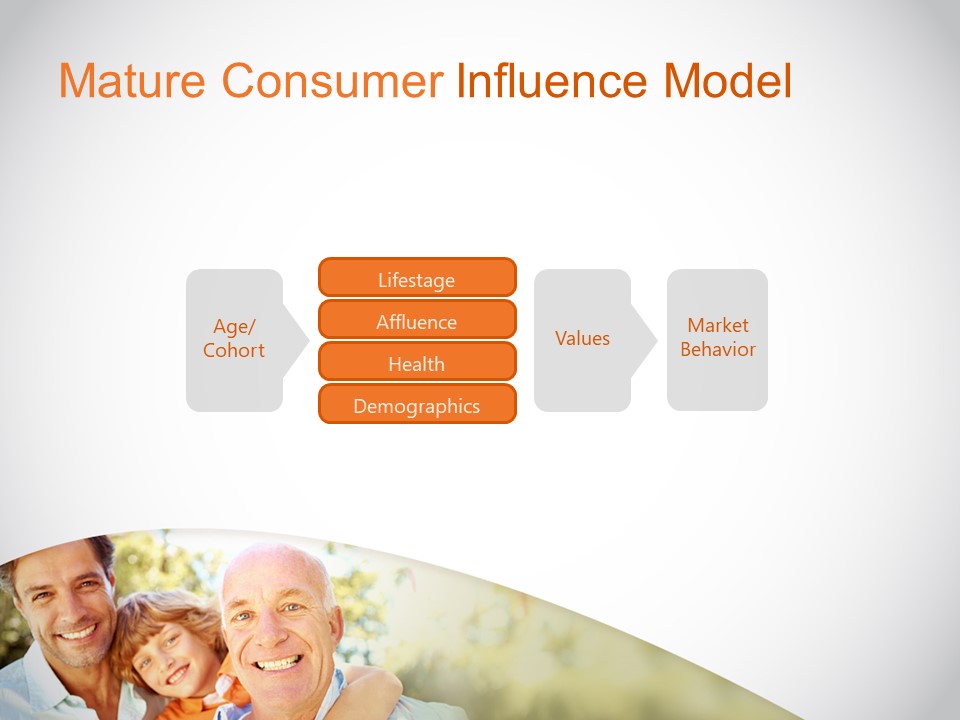

The Mature Consumer Influence Model

This is a model that we created to help show everything we’ve learned about this consumer in the last 25 years. The age cohort chart and how the generations break down is at the beginning of this funnel to understanding market behavior. Where all the really good stuff happens is in the middle block, the lifestages, and understanding those inflection points around lifestage.

When we look at affluence, we’re not just talking about income. We’re talking about both income and assets, and things like their home, or for younger people, their ability to get money from their parents. We look at their health, and we also look at those observable traits, those demographic traits – simple things like gender, race, and ethnicity. All this information, in addition to their generation, gets funneled through their value system, and that’s what shapes market behavior.

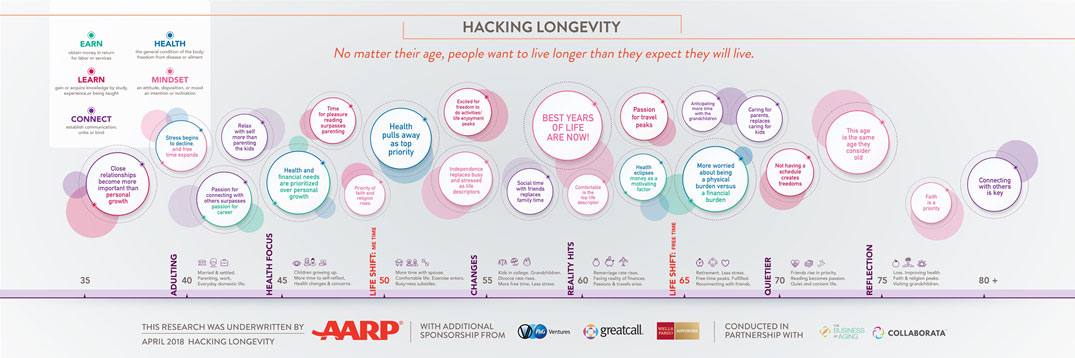

Below is an infographic that we created with the team at AARP for their Living 100 event last April. It is available on AARP’s website.

A first cut of the analysis was to look for key inflection points, where things were changing, where that life map was changing and why, and beginning to understand why things were happening the way they were. We found out a couple of really interesting observations.

Not surprisingly, in the mid-40s, which we call the adulting years, health and finances become prioritized over personal growth. People are still stressed out about work. They’re still raising children. They’re beginning to wind down their passion for their career and beginning to think about connecting with the other people in their lives. We start to see a shift in the 40s toward a sort of more “actualized” life.

In the early 50s, we see a key shift. Around 52, finances became less important as a concern to people, and good health became their priority. That seemed amazingly young and early to us, given what we know about someone at age 52 and what their lifespan could be. Also, in their late 50s, people began to talk about independence. The nest becomes empty around this time. Independence was replacing the terms like “busy” and “stressed” as life descriptors. Around the late 50s, social time with friends begins to replace family time. This coincides with grandchildren becoming older, families becoming busier with their own lives, and not as much interaction with the older adults in their lives.

We saw ten years between ages 55 and 65 that people described lovingly as the “golden years.” They say those are their best years. People had not had severe health decline yet. They were still working, so money worries were top of mind. By the mid-60s, people are beginning to think about becoming a burden to their children. They’re most worried about being a physical burden, as opposed to a financial burden, which is also really interesting, considering the number of them that aren’t in great shape for retirement.

Into ages 70s and 80s, we found that connecting with others was much more important. Whereas the family connection started to fade in the late 50s and early 60s ages, it amps up again in a big way in their 70s and 80s. Those people want family and friends around them and to surround themselves with close relationships. We know that’s important, because social isolation, as you’ve probably heard in some of the studies that have come out, is just as deadly for older people as smoking or lack of exercise.

So “How Old is Old?” and Other Consumer Opinions of Aging

One of the first questions we asked people in the study was, “How old is old?” We wanted to think about how we begin to communicate with people about the issues they’re having and how their perception of old age might shape how they received information. Gen Xers said 67 was old. Boomers said 76 was old. Also, the Silent Generation told us that 81 was old. Then we turned that around and asked, “How long do you think you’ll live?” Our ever-optimistic Baby Boomers said around 92. However, the Gen Xers and the Silent Generation, who tend to sort of be more pragmatic about these things, said about 88-and-a-half.

We discovered that “old” is not a number for people. They answered the question, but they had caveats. They told us that it’s about observable traits and state of mind. You’re old when your mobility is poor. You’re old when you’re afraid of falling, and you worry about your ability to get in and out a chair, or up and in and out of a car. Your joints hurt. You’re in pain all the time. You have health problems. You see a doctor frequently. You’re losing your independence. You’re forgetful. You refuse to learn new things, or you watch television all day. So those were the things that were driving what is considered “old.”

When we talked to people about how long they think they will live, they don’t tend to equate it to their health and their habits. They still equate this to genetics. They look to their oldest relative. “Well, my grandfather lived until he was 92, or my grandmother’s still alive, and she’s 98, so I guess I’ll probably live to 98.” The interesting thing about that is though they told us that they had relatives living longer and longer, they couldn’t identify the financial gap there. They weren’t connecting with the idea that that longer life meant they were going to be able to retire at 65 and live until 95 on the money that they’d saved. There was no connection to that. It was still very theoretical in the minds of these consumers.

We generationally asked about health and asked them to assess their health. Our seniors who are our Silent Generation, 63 percent of them say they’re in better health than other people their age. When we probed this question, they meant “I’m still here. I’m still able to go to the grocery store, go to the bank, and get out and see my friends, play bridge, and visit my grandchildren.” People with three to four chronic conditions who are managing many healthcare issues will tell you they are “in better health” than other people their age, which we found fascinating.

The problem with 63 percent of the Silent Generation believing that they’re in better health is that they are putting off decisions that would help them age more successfully. They’re putting off things like decisions to move to a home that would be more suitable to their needs – level entry doorways into homes, single-story homes. Many who are managing many health conditions and need monitoring regularly are putting off moves to assisted living because they think they’re literally in better health than other people their age. Those are the people that the industry, especially the senior housing industry, tends to worry about the most because they’re most prone to overdoing it. They’re prone to falls. They’re prone to accidents.

Health status was highly correlated with use of technology too, specifically things like fitness apps on phones and watches. We saw a number of people who said they were in better health than their peers using social apps to stay in touch with people. These can be things like LinkedIn and Facebook, or they could be things like chat apps. Just a few, and I mean a relative few, have made any accommodations for aging in place.

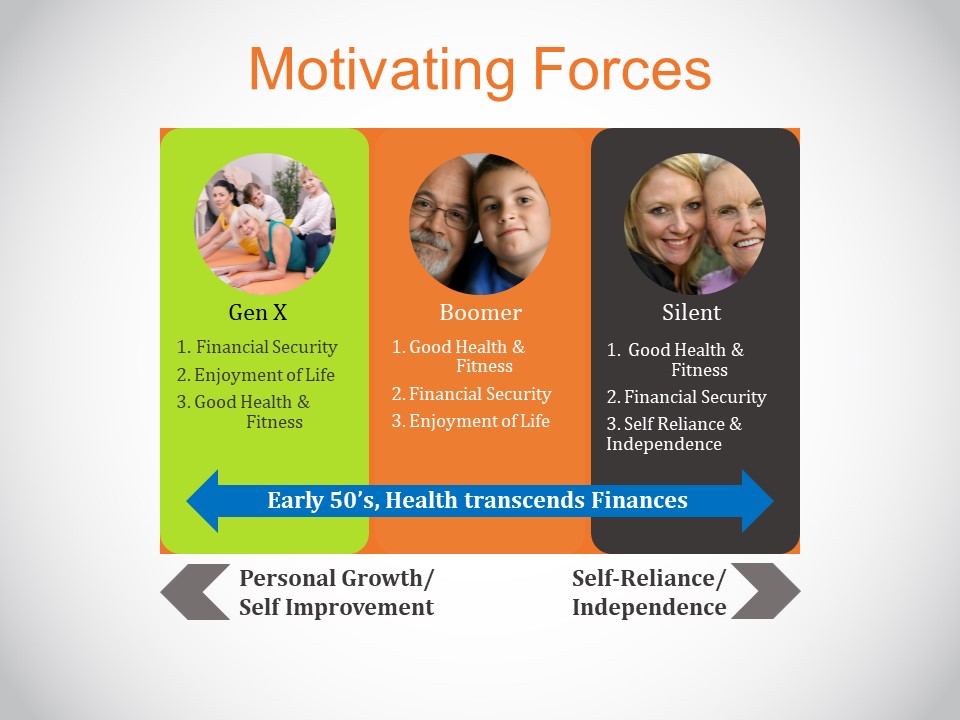

Motivating Forces

Generation X is our new sandwich generation. Their key motivator is financial security. They are perhaps the most likely to receive the message that they’re going to retire later and need more money in their old age. They seem much more receptive and practical about hearing that message. Enjoyment of life was number two, and they equate that to their family because many of them are still raising young children. They prioritize health and fitness as last.

Baby Boomers, on the other hand, had health and fitness as number one. The switch flips around 52, 53 years old, and health and fitness become more important to them than their financial security, which is a little bit crazy, because as you know, at 50, they still have years that they could be saving for their retirement. Enjoyment of life is number three.

Our Silent Generation, who are our seniors today, have prioritized good health and fitness. They want to stay on earth as long as possible, and they will tell you that in research. Financial security is number two. Self-reliance and independence is number three.

We also talked to them about fulfillment and what was fulfilling to them at different times in their lives. Not surprisingly, the oldest adults in the study told us that their lives remarkably fulfilled them, and our youngest oldest adults told us they were least fulfilled by what was going on in their lives.

In the field study, we asked people what actions they were taking to increase their lifespan. In focus groups, we caveated the question by saying, “Let’s say you’re going to live to be 100. What kinds of things would you do? What changes would you make?”

Baby Boomers reported certain things were very important to them to do and that they were trying to do them. When we probed on this, we found out that basically they don’t do what they say they’re going to do, which I think to anyone in the financial services industry that’s not a big surprise. I mean, they say that they know saving for retirement is extremely important, but they don’t do it. They’ll tell you, “Well, I have a gym membership. I went in January a couple of times. I’m trying to get back there, but I’ve been really busy.” So, we found a huge disconnect in the Boomer generation, across all ages in the Boomer generation, about intent versus reality. That’s a story we’ve seen for the last 20 years of researching this cohort.

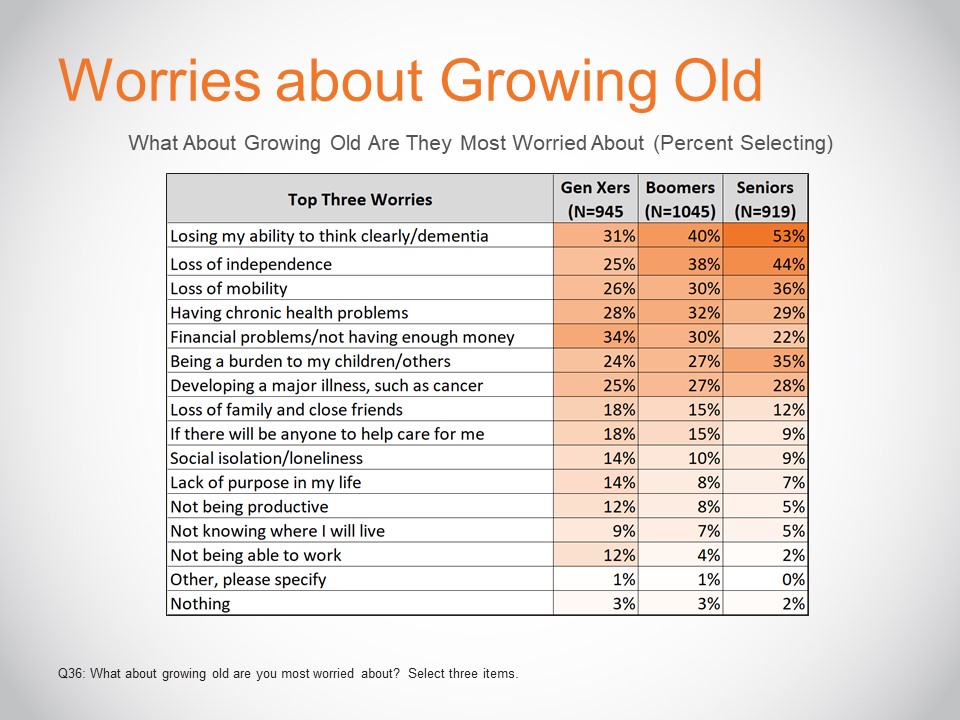

Worries About Growing Old

For our oldest seniors, our Silent Generation, only 22 percent are anxious about financial problems and not having money. However, 35 percent are worried about becoming a burden. I thought that was a provocative number. Only 30 percent of boomers are concerned about not having enough money. This is a place where Gen Xers start to pop. We saw a little more pragmatic behavior, a little bit more practical approach to thinking about their older age.

Then there were things like developing an illness. People tend to shove that to the back of their mind. That hasn’t really changed over time. Isolation and loneliness, we thought would pop more than it did here, especially for older adults. Not being productive, we thought would pop more for older adults. However, our hypothesis here was because the older adults in our study were able to be online and participate in the study.

So, here’s that question. If they could live to 100, what things would you change? What changes would people make if they knew they were going to live to 100? Also, this was a survey question, not just a focus group question. Fifty-two percent of Gen Xers said fitness. Forty-four percent of boomers said fitness. Thirty-three percent of seniors said fitness. We thought that was really, really interesting.

Let’s look at financial planning. Fifty-seven percent of Gen Xers said they would change their financial plans or their investment portfolio. Again, we see a much more practical, much more “eyes open” point of view. Only 41 percent of boomers would change their investment plan.

The Generation X Caregiver

If you had Baby Boomer caregivers caring for their World War II generation or older parents in your past, and you talked to them about how they felt about their parents or why they were providing care, they would say things to you like, “These are my parents. They did so much for me. I feel obligated. I feel a sense of obligation.” The language around caregiving for that Baby Boomer caregiver was loving and nurturing and giving back to their parent. That part of the conversation is missing with Gen X caregivers. It’s not that they don’t love their parents, but their approach to the work of caregiving is just different.

They describe it as hard and tiring, boring and monotonous and isolating. Gen X has no free time, they’re not appreciated, and they can’t get their siblings to cooperate. While all of these things might have been true for the Baby Boomer caregiver, you rarely find a study where they would describe the experience this way. So this a very, very different approach and a very different way of thinking about it. Again, that really practical, pragmatic approach to looking at aging.

Not ironically, seniors nor their children look forward to the prospect of being cared for or providing care. In this study, they told us overwhelmingly that they preferred having their parents live in a separate home from them. There was a real disconnect there, and practicality to this construct for Generation X of being a caregiver, and it’s much less emotionally charged than in previous generations.

When we talked to the adult children about what caregiving looks like, they told us they’re concerned that their parents won’t have the funds to take care of themselves. They’re worried about high maintenance parents. Several people said, “I had helicopter parents as a kid, and I don’t even want to know what that’s going to look like when they’re old people.” They’re concerned about dementia and the need for and expense for residential care. By the way, very few of them in our Silent, our Boomers, and our Gen Xers – with a couple of exceptions of the Silent Generation folks who have actually looked into CCRCs, continuing care retirement communities, or an assisted living facility – understand how the finances of living in an assisted living facility, in skilled nursing care, or a CCRC works.

Most young people think that somehow Medicare covers all this, that it’s this magical fund that is going to pay for everything. Even when you talk to boomers about skilled nursing care, they don’t understand. In spite of all the commercials on TV that say the high cost of skilled nursing care is X, people aren’t internalizing that information, and they don’t get it. Nobody understands how much long-term care costs and who pays for it. They’re not getting the message.

Adult children are apprehensive about the change to their lifestyle. They’re very aware that they’re juggling young kids and older adults. They don’t like the prospect of the parent living with them. They feel guilty about a parent who lives far away. Most say they would hire someone to take care of their parent. Most cannot get siblings to cooperate. In the study and our focus groups, many of them talked about technology and the use of technology to monitor their parents and to control the caregiving situation, which is something we have not heard a lot about before in studies where we’ve drilled down on caregiving.

Key Takeaways

All of our generations realize that longer lives are happening, but they’re doing very little to prepare to it, which was what we were trying to discover with this study, what are people doing.

There are barriers to planning. The barrier that we heard over and over again was that – and I’m going to say this in the way that consumers say it – financial planning is hard. We don’t understand it. We’re not sure whom to trust. We’re not sure if we should be talking to people who don’t sell products to us or people who do sell products to us. These were all things that came out when we asked them about why this is such a hard bridge for them to cross.

Regardless of financial situation, Baby Boomers are switching their focus from their finances to their health relatively early. They aren’t making that connection between health and wealth. By wealth, I mean a better life; not just a better financial life, but a better life overall. I believe that financial professionals can help make that connection stronger. As you look at the segments and see all the things that are of high importance to each who feel like they’re in the best years of their lives, it’s all about the health-wealth connection.

Generation X is a whole new breed of caregivers. They’re going to be relying on technology and other people to take care of their parents, and they’re going to want to receive communication through technology. They are so unlikely to want to do things live or even through email. They’re texters. They want to be able to get quotes online. They want to be able to get information online. It’s almost impossible to get them to realize that the device in their hand is also a telephone. I mean, they’ll use it for nearly anything other than talking to someone live. It was really an interesting takeaway from the study. They want to engage with retirement planners about their parents. They want to understand the money situation. However, they’re going to want to do it using technology and not necessarily face-to-face with you, or even on the phone with you.

Women at the younger end of the 50+ population are struggling. We’re going to see more and more people aging singly by choice, people who choose not to get married, or who had early marriages and divorced and are going to stay single. They’re worried about their finances. This is a consumer that needs professionals who can empower them to plan. Even though they may have very few resources to start with, they need to be encouraged and empowered. They use those words when they describe the situation.

*Sponsored by AARP, Wells Fargo, Great Call, P&G Ventures and Collaborata,

About Lori Bitter, The Business of Aging

Lori K. Bitter provides strategic consulting, research and development for companies seeking to engage with mature consumers at The Business of Aging. Her recent research, Hacking Longevity, was sponsored by AARP, P&G Ventures, GreatCall, and Wells Fargo Advisors. Lori was named one of Next Avenue’s Influencers in Aging for 2017. Her book, The Grandparent Economy is a National Mature Media Award winner. She serves as Co-Producer of What’s Next Boomer Business Summit and The Silicon Valley Boomer Venture Summit.

Lori is the former president of Continuum Crew and Crew Media, owner of Eons.com. She was president of J. Walter Thompson’s Boomer division, JWT BOOM. Prior to that she led client service for Age Wave Impact. Lori has more than 30 years of advertising, public relations and strategic planning experience. She serves on the advisory board of several start-ups and nonprofits.

A sought‐after speaker, Lori has presented research, trends and analysis about mature consumers and the longevity marketplace to more than 200 conferences and events in the United States, the United Kingdom and Europe.

Are you looking for a retirement speaker for your next conference, consumer event or internal professional development program? Visit the Retirement Speakers Bureau to find leading retirement industry speakers, authors, trainers and professional development experts who can address your audience’s needs and budget.

©2019, Lori Bitter, The Business of Aging. All rights reserved. Used with permission.