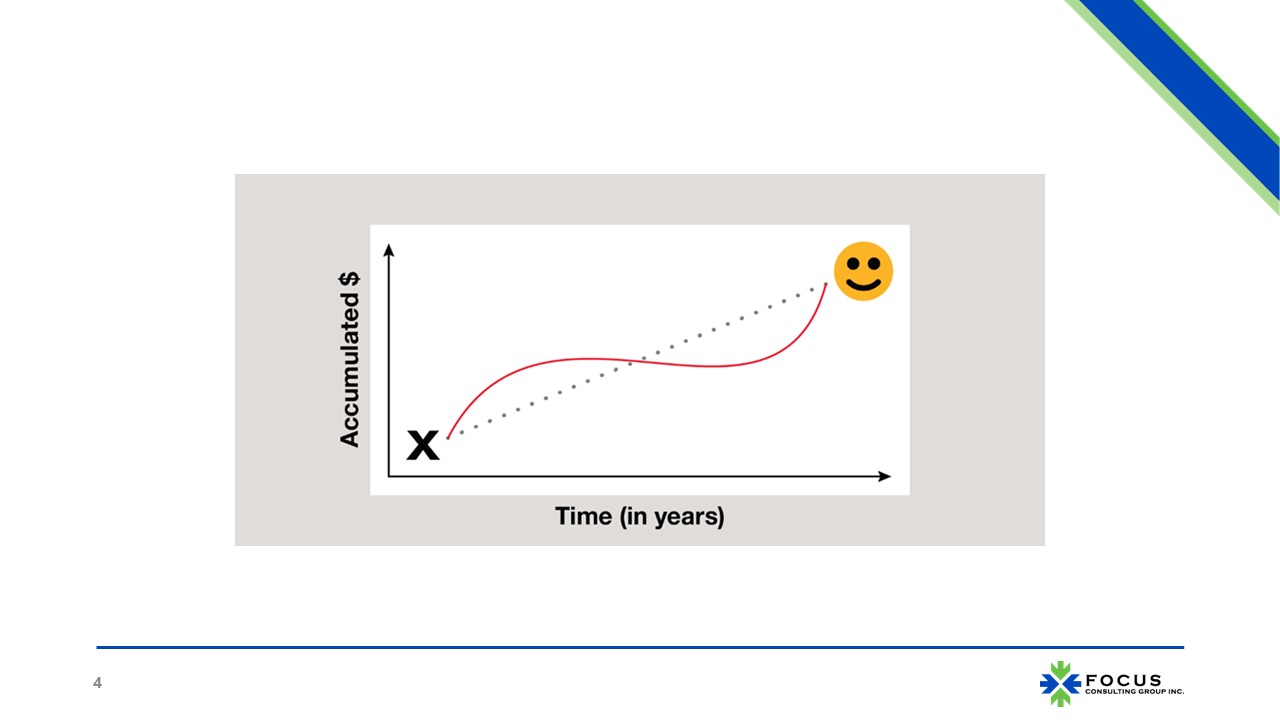

Now, there are four things in this picture. You have an X, you have a smiley face, you have a dotted straight line, and you have a red, curvy line. I want to focus on the smiley face because that smiley face is your goal. That’s your aspiration. That’s your ambition. We can label it any way we wish, but it’s the same thing universally. Where is it you want to go?

Not an easy question, whether this is a retirement of X level of comfort and spending ability, whether that is a bigger home in five years, whether it’s a bass boat in 10 years, college education for a young child in 15 years. You may have many smiley faces. Hopefully, your life has nothing but many smiley faces, but the point here is until you establish what it is that is your aspiration there is no reason to begin the investment or investing process.

Next, we go to the X. You are here at the X with a certain amount of savings, a certain amount of income, with a certain amount of spending.

The dotted line is purely math. Another way of saying it is its fiction. Math isn’t fiction, but this is math about the future, and math about the future is distinctly fiction. The dotted line from where you are today to get to your aspiration is easy to see because we can calculate this, but the reality is the red, curvy line. The red, curvy line is an illustration only of what can happen. Sometimes, you’re way ahead of the game, and you’re above the mathematical mapping line. Sometimes you fall below that line as you’re approaching your timeframe for your ambition.

If you could get an investment that guaranteed you exactly what the dotted line is, you would put all of your savings into your investment and walk away. You would never think about this again. Now, you know why I call that fiction. It doesn’t exist.

Choosing and Holding Investments

Two to five investments. I can name that tune in that few holdings, a couple of index funds, maybe something else. We do not need and should not overcomplicate this. Is it worthwhile the bother, to take the time to do the research on an investment? Watch it over time, and try and wrestle with, “Do I sell it now? Do I hold it? Do I fire a manager?”

There is a lot wrapped up in choosing and holding investments. I’m not saying it cannot be worthwhile, but it takes knowledge and investment of time to do it well. Well doesn’t mean guaranteed success. Well means a probability of success, or two to five index funds or cash, and maybe you’re done.

The only thing I can tell you about the future of how your investments are going to perform is how much they cost. That’s the only thing I know for certain about the future. Fees are guaranteed, performance is not. The simpler way of saying this is the lower the fees, specifically with index funds, the better. With active managers, also better, but understand fees aren’t the whole story if you’ve got a good manager. Then again, we get back to the question can you find a good manager in advance before they perform well, not just looking at what they did in the past?

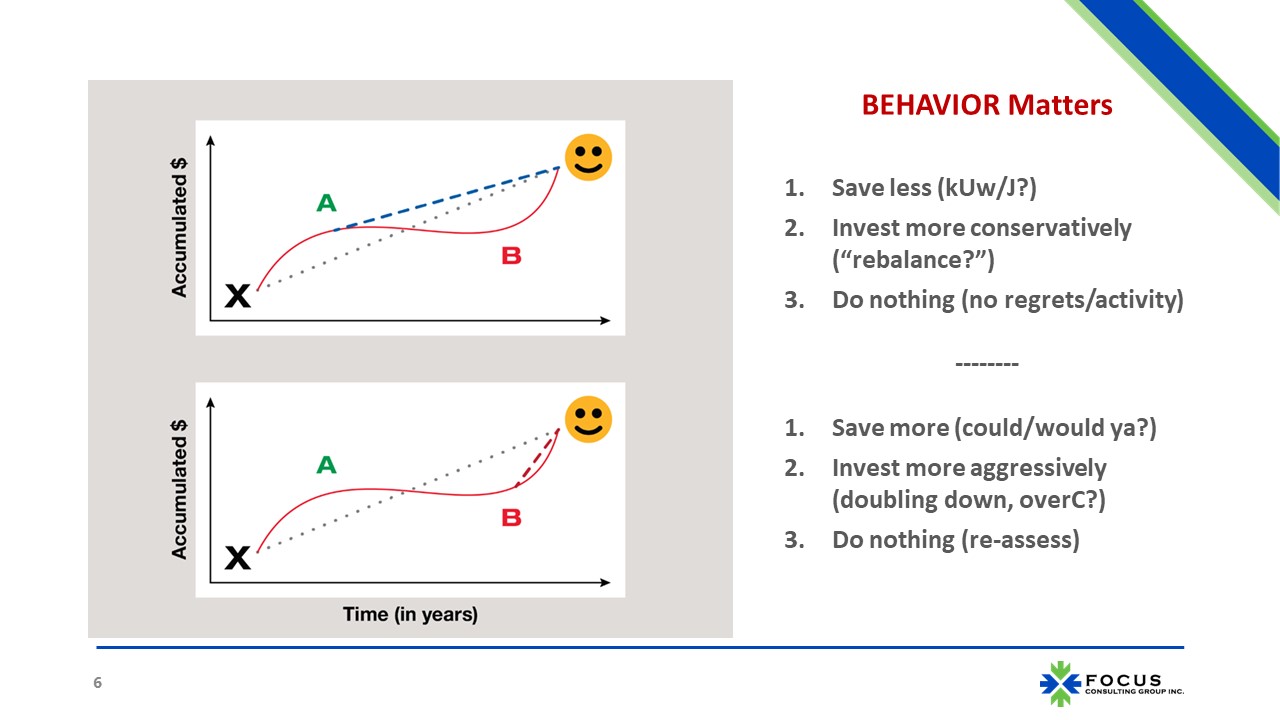

Behavior Matters

Now let’s cover situational choice architecture. In the picture below, I’ve labeled two points in time, A and B. At those points, I’ve redrawn a dotted line to get to your happy place.

In the top picture, we’re focusing on Point A. When you get to Point A, you’re feeling pretty good. We’re ahead, we’re outearning our mathematical estimate of need. You have three basic choices; this is choice architecture. This is 100% behavioral.

- Your first question when you’re ahead of the game is, do you want to save less? Our investments are performing so well maybe we can back off on saving.

See that very confusing set of letters in the parentheses? Keep up with the Joneses. The only reason to save less is that you want to spend more now. Spending more now is possibly tantamount to keeping up with the Joneses. Mr. Market doesn’t care about you, and you know what? The Joneses don’t care about you either.

- Maybe you don’t save less. Maybe you begin to invest more conservatively. We’ve had some investments that performed really well. Maybe we should rebalance, take some of the winning investments and bring them into the losing investments. It would also be investing back to what you originally put together in your portfolio. The challenge here, and why I put rebalance in a question mark, is sometimes certain things you invest in continue to outperform others in your portfolio. Rebalancing can take money out of your future pocket. Rebalancing is good behavior, but it’s not a perfect behavior. We don’t know when we should rebalance when things are different. However, it’s a wonderful and simple discipline.

We don’t know when is best, so you may want to do it annually. Why annually? Because if you’re not in a tax-sheltered account, you don’t trigger any short-term taxes, so maybe not a bad idea. Come to terms with the behavioral side of this. You’re selling something that made you feel good, and you’re buying something that you’re disappointed in. This is the opposite of what we, as human beings, find comfort in. Rebalancing is simple to say if you don’t automate it and use it as a discipline. Trying to do it ad hoc is really tough. It’s kind of against our human nature.

- Or you can do nothing.

What are Behavioral Tricks?

Regret bias and activity bias are nasty little twins in the bias world. Regret is the fear of co-mission, which is harsher than the fear of omission. Doing something and having it turn out badly hurts you more than doing nothing if it turns out badly. This is very powerful. This is why inertia is so powerful. People don’t want to make that choice. There are fewer regrets if you do nothing.

Activity bias – some people think when it comes to investing, I just need to do more, and I’ll make more money. There is not a single piece of literature, academic research that exists that says more trading, more performance. In fact, most of it points to less trading, more performance. Save less, invest more conservatively, or do nothing because at Point A you’re ahead of the game.

At Point B, Mr. Market has become depressed, and your aspiration is right around the corner, or it’s very near in time.

- If you’re possibly able, save more. Could you, would you? Can you suddenly start to save a lot more money to try and get to the same place? This is the challenge for most of the pension funds that exist in the U.S. these days. They’re severely underfunded. They could save more, but then they’d need to take money from taxpayers. Could you? Maybe. Would you? No, because then they’d get thrown out of office.

- You could choose to invest more aggressively. Sadly, this is what most of the pension funds are doing, but this is a real strategy. Invest more aggressively. Let’s move into investments that we think can earn a higher rate of return to help us dig out of this hole. This is what I refer to as doubling down. We all know what happens when we’re in a casino, and we do this. Let’s not talk about it because what happens in Vegas stays in Vegas.

Overconfident? When people start investing more aggressively, I ask about their level of overconfidence. Why do you think that bet will pay off such that it is worth the additional potential risk or variability that you’re exposing yourself to?

- Or you can do nothing. The difference here with doing nothing is not hoping for the best because hope is not a strategy.

What I mean by doing nothing is reassess. Say you wanted to accomplish that goal in five years. What if we pushed it up to seven years or eight years or ten years? First of all, is it possible? Usually, it is possible, but that doesn’t mean people like it. Don’t do nothing. Only reassess because if the market has become depressed, do you know what happens with the prices on a lot of things that we may want to buy that are part of our aspirations? Sometimes the prices adjust down as well, so you may not be in as big a hole as you think you are. You need to reassess.

In this entire concept, you should be reassessing your smiley face and your X, where you’re going, where you want to go, and where you are right now. You should be reassessing these things no less than annually. That doesn’t mean you’re going to be making changes with your investments all the time, but let’s find out where the X is related to your smiley face. All this information annually, once a year, can help you make better decisions.

When you have this simple choice architecture for situations when you’re at a Point A or a Point B, when you know these choices in advance, then it’s less about reacting to Mr. Market’s bipolar behavior. It’s more about understanding what will be the best decision for you at that point in time.

All You Need to Know About Understanding Risk

I have a real problem with almost every risk measure that investment professionals use, and as an investment professional, I have the prerogative to call them out and say stop! Enough with the fancy math.

Do you want to know what risk is? If investing is about reaching a goal, risk is falling short of your goal. Can we end the conversation now? Risk is simply falling short. That’s all that matters, but we need to know how far you’re short and when we need to get there to understand how great your risk is. Where’s the goal in time compared to where we are right now? Are we in a hole or not, really? Maybe we’re not in a hole.

When you look up the definition of risk in a dictionary, all it basically says is an unknown outcome. There are more possibilities in terms of what can happen than the one thing that will happen. Some of those outcomes are unhappy outcomes. Some of them are perfectly fine. What we really want is that we don’t want to fall short. The more predictable our investments are, the easier we can tolerate them, the easier we can simply hold onto them and not become a day trader or anything like a day trader.

What is the definition of predictability? The narrowness of the asset classes, distribution costs, different past calendar years. If I’m looking at stocks or bonds, how wide are the different performances historically over 5 or 15 years? I’m looking at five years or less as short-term, 15 years or longer, long-term, in-between, intermediate term. If your happy face is more than 15 years out, please do not stress about Mr. Market’s bipolar behavior until you get within five years.

If your goal is in five years, this matters. I want to label conservative investments only as investments that have narrower distributions and fewer outliers. For example, the calculation could be the 30th percentile minus the 70th percentile. If you line up all of the index funds or category of investment mutual funds and see the distribution from the best to the worst, I want to know the range of returns from basically the middle third. Not the top third, not the bottom third, but kind of the middle third; I want to know the range of the middle third.

Then, divide that range by the single number of calendar year results outside of that over the last 15 years, the number of outliers. The smaller the number, the narrower, the fewer the outliers as compared to the middle third. Smaller results are more conservative than larger results, which are more aggressive.

Calendar year results are available publicly, and it’s easy, but if possible, you’d be better to use monthly, rolling one-year results. It can help you, but you don’t have to go there.

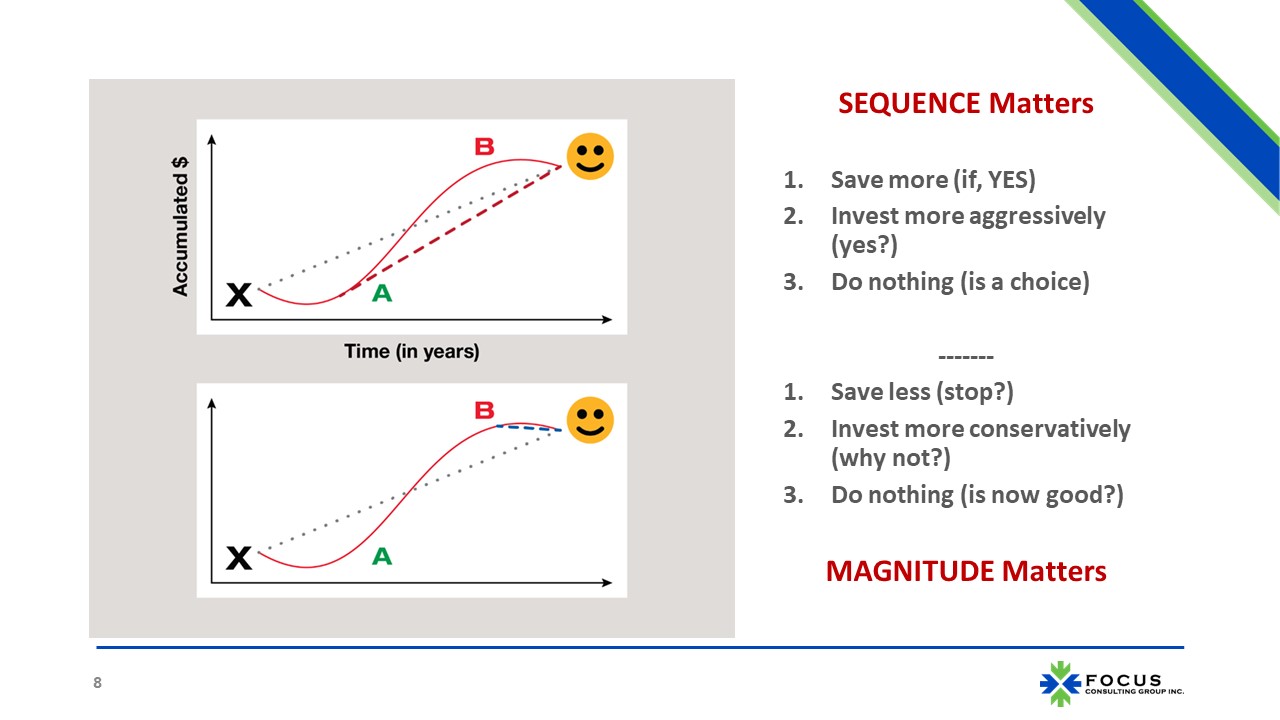

Sequence Matters

What if I flip the A and the B? The depressed period happens early in your investing career, and the manic period occurs late in your investing career.

The same choice architecture applies. If A happens, top graphic, save more. If you’ve got a long-time horizon and a little additional savings – you don’t have to make it all up in the next one or two years – you’ve got time. Saving more is brilliant if you’re able to do it.

Invest more aggressively is a smaller yes. Why? Because you could invest more aggressively because you’ve got so much time so that short periods, which are bouncing around and making you nervous and uncomfortable, matter less because over the longer term, it can be made up. The reason why I have a small yes instead of a big yes is because this makes sense. I don’t know how aggressively you were investing to begin with, so if you were invested really aggressively you may not be able to become more aggressive, not without starting to gamble. You have to have the stomach for it.

Of course, you could do nothing, which is a choice. Listen, if we know Mr. Market goes through fits of depression and manic behavior, let’s just wait for Mr. Market to become manic again. That’s a choice.

Bottom graphic; B, manic before your ambition, your aspiration, your happy face. Well, you can certainly save less. Maybe you stop where you look at where B is located on the accumulated dollar vertical axis compared to the smiley face. Congratulations; you’ve arrived. You might be able to accelerate your goal. Remember that reassess? When you reassess now, now you’ve got a really interesting question. Do I want to continue, or do I want to start embracing my happy face plans?

Before you jump ahead in time, maybe just invest more conservatively. Why not? Take your chips off the table. Invest more conservatively. Listen, you’ll still get a little growth, but you’ve taken away the risk because you’ve already arrived.

You might say, I’m enjoying work. I’m enjoying what I do. I’m not ready to stop just now. Or maybe your happy face is retirement. Then, I ask the question, why not? It doesn’t hurt you, and you can put off making that decision if you wish to do so. Of course, you can always do nothing, to which I ask people, is now good? Is now a good time to embrace that ambition and maybe start enjoying your life a little more? Let’s talk about that. That conversation is all about psychology and behavior. It has nothing to do with investing.

Investing is Not Investments

Investments are little things, index funds, active managers, stocks, bonds. Investing is your life; everything you need to know is about investing. Remember, I said risk sequence and magnitude? Magnitude matters. What if there was no space on these graphics, if a depressed Mr. Market, Point A, what if it dropped below the horizontal line? What if you now lost money? You’re in negative territory, not in terms of a decrease from a point you were at; I mean, now you’re underwater.

That’s difficult to have happen over 15 years or longer, but it can happen to investments in the short term. If Mr. Market is exceedingly manic at any point in time, it will affect your choice architecture because you will have made such incredible returns, but it makes your choices more difficult.

You know sequence matters. The way that magnitude matters is by making the depressed Mr. Market worse and the manic that much better by expanding the range. Remember, risk predictability; the narrowness is more conservative, the wider is more aggressive.

Magnitude makes things wider by making the results wider in terms of how much you have saved towards your goal. It puts more pressure on your choices, and it brings much more emotion into your choice making, your decision making. That’s how magnitude matters, so having these perspectives ahead of time, when you’re not surprised when you are in more of a peaceful, understanding decision-making moment versus an emotional, reactionary moment, you will make better decisions.

This is why I say behavior is more significant than investments. It’s not about what the investment is doing. It’s about what you’re doing. How predictable is what you’re doing? When you set forth a goal, is it a reasonable goal? Is your smiley face within reach? That dotted line, that mathematical line that’s a fiction, if that mathematical is too steep, it’s pointing up, it is the Southeast to the Northeast, then markets may not be able to do this for you. Maybe you need to reassess your goals.

Time has predictability needs no matter how hard it is or easy it is to meet your goal. As humans, predictability helps. Time needs you to update. Instead of an annual reassessment of your goals, manage your expectations. See what is possible.

Key Takeaways

You’ve been shown a process, an approach, that you can use.

First, know thyself. Understand your tradeoffs. Choices, said another way, are tradeoffs. If I save more today, I can’t consume as much today. That’s a tradeoff. If I save less today, I can consume more. You always have that situation of how does your future self, if you could meet your future self today, how do they look at you? Does your future self appreciate what you did, or does your future self look back with a whole lot of regret? Understand your tradeoffs.

Goals, not markets, are what matter; your goals, your behavior, your decisions. This is not about investments. There is no easy button. Know these things. If you know these things well, you are ahead of the game.

Assess and reassess over time. Assess your smiley faces. What is it that is going to make you happy? It is that simple. Reassess them over time and make decisions that are tradeoffs. Those are your choices, the choice architecture, and the situational. Learn whether you tend to make better decisions, or maybe they could have been better decisions because that can inform your future behavior. If your decisions are often not as right as they could have been, maybe the next time that situation pops up, you don’t make that same decision. Learn.

See. To learn, you have to see. See the did’s. What did you choose? Those are your did’s. See those choices as opportunity. Don’t see them as a laboring effort (ugh, I hate it when I have to do this!). No. See them as opportunity. See Mr. Market as he is. He needs help. He’s bipolar, and he doesn’t care about you. When you acknowledge that the market doesn’t owe you anything because it can’t, then you have to control what you can. You can control your choices. You can control where you want to go. You can control your savings, how you invest. These are the things you can control. You can’t control the outcome of your investments. Mr. Market does that. Avoid Mr. Market when he’s acting up. When he’s being really depressed or really manic, do nothing. That’s what I mean by avoid.

Don’t make choices when Mr. Market is having a mood. Some of you have been on a road trip with young children at some point in your life. You know this question is coming from the back seat of that car. Are we there yet? No. When you assess and reassess over time, that’s it. Avoid in-between assessments ever asking that question. You’ll thank me for it if you can.

Get help. Professionals in almost every walk of life have coaches, athletes, musicians, actors. Why is it that professions like lawyers and doctors and investment pros on average do not have coaches? That’s ego. You don’t know one artist, one athlete who doesn’t want to get better and better. They have coaches. Yet, the professions don’t, so get help. Get a coach. For investors, that may look like a financial planner who can help be your independent, objective observer, help you build and understand the math of the dotted line, help you assess your goals.

Are they reasonable? They can help you understand what the market may or may not be able to provide. That coaching can be invaluable and much more valuable than your investments.