What Does It Really Cost To Retire?

So when thinking about the assets, we’re talking about things like your portfolio, your 401(k), your IRA, your taxable accounts, the monies that you have saved to fund retirement.

Now when we do projections about assets, the past is usually our guide. I’ve done a lot of research on this topic with Wade Pfau and Michael Kitces. The U.S. stock market historically has been a phenomenal wealth creation engine for investors. It has been one of the best places to invest historically. So I think if we start from this place of, well the past is a guide, we have to ask ourselves how valid is it for the future?

This is really important for investors today because this radically affects the definition of what is a safe strategy for retirement. What is the key perspective on what is a safe withdrawal rate? Well, we’ve all heard of the 4 percent rule. I think that sometimes people get this wrong a little bit because the 4 percent rule only tells you about the withdrawal rate in the first year of retirement; in the first year of retirement, you can take out 4 percent of your initial account balance, and you increase that amount by inflation every year for 30 years.

In reality, it’s not the 4 percent rule. It’s really a 25 times rule, where you need 25 times your initial income goal when you first retire. This approach has been backed up by a variety of different research.

The Replacement Rate

There are some common assumptions we use when it comes to estimating that retirement liability.

The idea behind a replacement rate is to say, “Hey, what changes when I retire? If I’m making $50,000 today and then I retire tomorrow, what do I need to replace in retirement from an income perspective?”

The idea of saving for retirement is based upon what’s called consumption smoothing. An individual works for say 40 years and they save for retirement so that when they retire, they don’t all of a sudden have to have this radical shock to their lifestyle. They can keep enjoying the same things they had before they retired. It’s also called the life cycle model.

Another thing is that expenses change at and during retirement. I mentioned the idea that once you retire, you’re no longer obviously saving for retirement. You aren’t paying certain taxes on your income. There are other things that make your tax situation more advantageous when you retire.

There is also this idea of income differences. What I mean here is that for different people who make different levels of income, they can have radically different tax situations before and after retirement. So one example of this is Social Security; how much of your pre-retirement income is replaced from Social Security based upon different income levels? If you know about the way the formula works, the more you make, the less you have replaced. So if you only make $25,000 per year when you are working, you’ll get about a 60 percent replacement rate from Social Security.

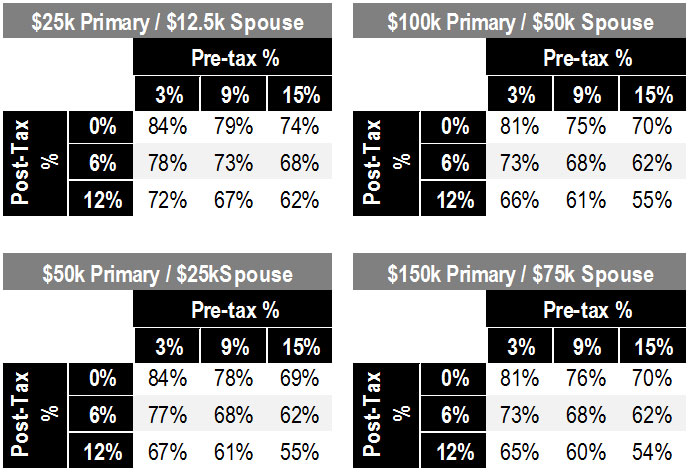

As your individual income surpasses $100,000 or even up to $200,000, the replacement income you get from Social Security decreases significantly. What changes too is these benefits become taxed at different levels. So that kind begs the question, what is the right replacement right for different individuals? Here are four different household examples.

Replacement Rates for Various Households

In the upper left you see a household where the primary worker makes $25,000 per year, and the spouse makes $12,500 per year.

If you move to the bottom left, the combined income for household is $75,000, upper right its $150,000, and bottom right is $225,000. What I’m showing you here is how the replacement rate varies based upon different levels of pre-tax and post-tax savings. Think of it as saving pre-tax in the traditional 401(k), post-tax in a ROTH 401(k). What you see here is that there really isn’t one number for everyone. 80 percent gives a reasonably average across the scenarios, but if there are extremes.

For a relatively low-income household that isn’t saving much for retirement, 84 percent is their replacement. A higher-income household, because they don’t receive much from Social Security, has to save a lot more for retirement. A 54 percent replacement rate actually makes sense. But it needs to be even more complex if you factor in, “When are you going to pay off your mortgage? What expenses may also go away in retirement that you are paying during accumulation?” The moral here is it really makes sense to figure out what is the desired amount of income for a particular situation.

Retirement Consumption

There’s been this noted effect in research called the retirement consumption puzzle. Either at retirement or during retirement, people don’t tend to increase their consumption by inflation. This takes place to some effect at retirement; mostly because people that retire tend to make more meals at home versus eating out.

But a more important effect is how consumption changes during retirement. On average, as people age, they tend to slow down. So they transition from the go-go years, to the slow-go years and the no-go years. They tend to spend less, they tend to be less mobile, so that obviously affects their overall consumption.

But they’re spending on different things. A research database called the Health and Retirement Study (HRS), tracks households over time. For the same exact household, it ask, “What did you spend this year? What did you spend in the prior years?”

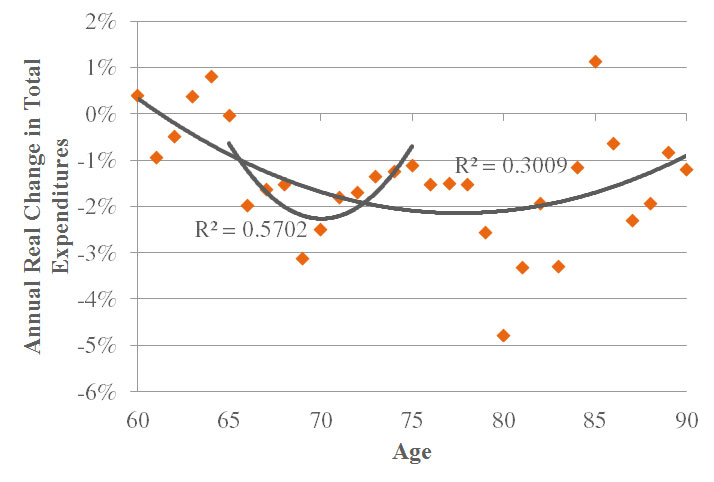

So how do these levels of consumption actually change when you look at the same households over time? We would expect that the real change in expenditures should be 0 percent. If it’s 0 percent, it means that they are increasing their consumption by inflation every single year. What I found was that the actual change tends to be negative. A negative change means that if inflation goes up say 3 percent in the year, they’ll only spend maybe 2 percent more the following year.

In the graph below, you’ll see two things I call the “retirement spending smile”. It suggests is that younger retirees tend to actually increase their consumption a little bit more, or it tends to go down less, than middle-aged retirees.

Real Change in Expenditures for Retirees

So between the ages of say 70 and 80, it tends to bottom out. Expenses tend to tick back up after age 80 because of healthcare costs.

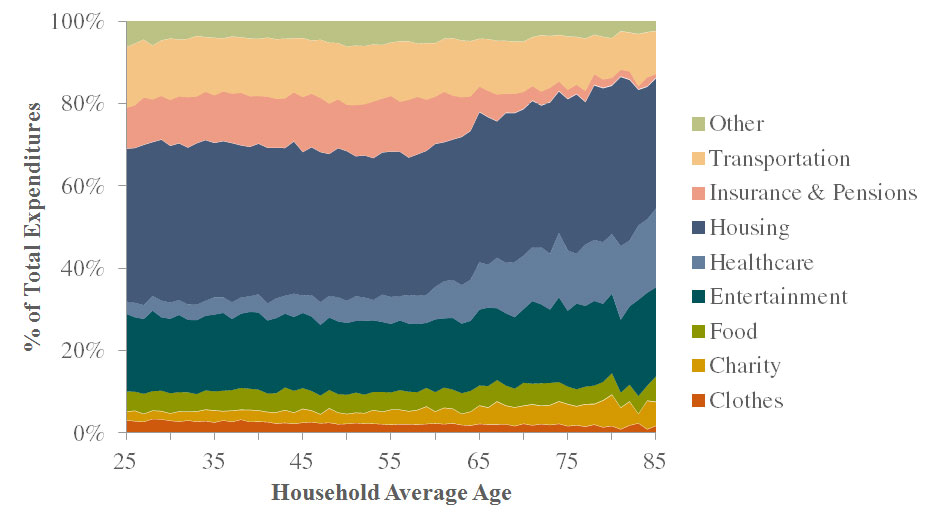

There are nine major consumption baskets that vary over the average household’s lifetime, and are relatively static, except for two things. The first is insurance and pensions. Up until retirement, it’s a relatively constant percentage. After retirement, it drops significantly. Healthcare tends to increase significantly during retirement.

Expenditures as a Percentage of Total Consumption by Age

For the average household at age 65, regardless if they are high income, middle income or low income, they spend about 10 percent at age 65 of their total consumption on healthcare. That same household who is age 85 will devote 20 percent on average of their total consumption to total healthcare. What’s interesting though is that there isn’t a big difference in low income, middle income and high income groups to how much they actually spend on healthcare on average.

Why do households tend to spend less as they age? There are two obvious answers here. One reason is they are choosing to spend less because they just don’t need to buy a new car as often, new clothes, etc. The other possibility is necessity. If you read the news, we’ve all heard about a “retirement crisis”; but I don’t think it’s a crisis. So I ran some additional tests. What happens if I change this test route, and group households into the following four buckets?

- Matched spending and wealth

- Low spend, low net worth

- High spend, high net worth

- Unmatched spending and wealth

- High spend, low net worth

- Low spend, high net worth

Matched Spending and Wealth

Matched Spending and Wealth

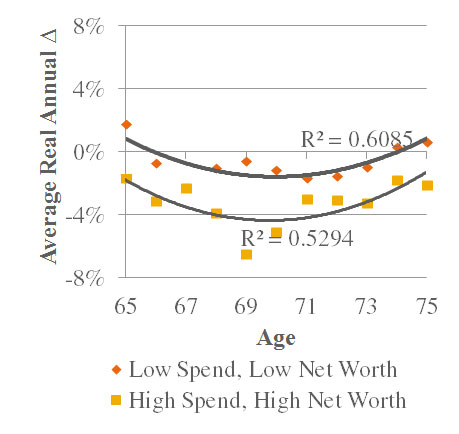

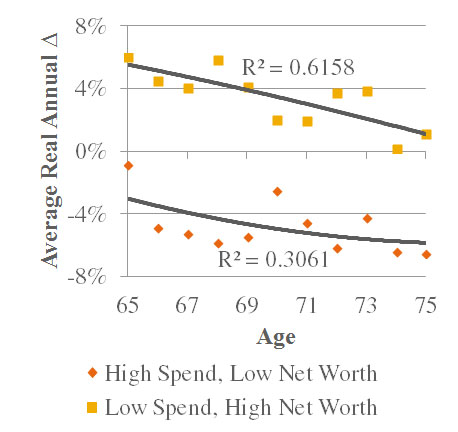

One bucket is matched spending and wealth. What that means is, for example, you have a lot of wealth, and you’re also spending a lot of money. Another example is you’re not spending much, but you have a relatively low net worth. You see the same effect for the matched spending; you see the same smile.

The other example is what I call mismatched spending. These individuals have a low spend and high net worth. You actually see this effect of decreased consumption for the mismatched more than the matched.

Using this somewhat simple perspective on how different households could choose to consume, it still suggests that some of this is by choice. This begs the question, what does this do to portfolio success rates? Think about the spending curves (smiles). If you’re doing a Monte Carlo simulation for a client, you’re probably going to assume that if they spend $1 today, they’re going to spend that same $1 thirty years from now, adjusted for inflation. What does it do to a retirement income projection if instead of assuming they spend that same $1 increased by inflation, if they spent based upon these curves? How does that change in assumption affect success rates?

What you see is a very large difference in what would be considered a safe withdrawal rate from a portfolio. If you were to use this assumption that people tend to increase their consumption every year by inflation, you might say that a 4 percent withdrawal rate hypothetically is safe. If you model actual inflation, in terms of how the consumption changes for retirees, what you’d see is that 5 percent is the right number because in reality, if you do decrease your consumption over time, you don’t have to have as much saved for retirement. So changing this model, I think, can radically affect what you do for retirees.

Length of Retirement

When we’re thinking about retirement, there’s this idea of longevity risk, which is living a long time. Of all the risks in retirement – return risk, inflation risk, sequence risk, health risk – longevity risk is the biggest danger that retirees face. Funding a retirement that lasts 5 years versus 40 years leads to two very, very different perspectives about how much you have to have saved for retirement. The model we use today for retirement is incredibly inefficient from an income perspective.

In the past, one of the key means that individuals used to fund their retirements were through defined benefit plans. Defined benefit plans are incredibly efficient from the retirement income perspective. Within a defined benefit plan, that risk of living too long is pooled. For every person who lived to say age 95 or age 100, someone else would die at age 65, age 70, age 73, age 78, etc. Now though, as we’ve moved towards defined contribution plans, there is no more risk pooling. Every single person has to plan to live to age 100 or age 95. That’s very inefficient because as we know, most people won’t live that long.

Now for better or for worse, the only way to guarantee income for the length of retirement is through some type of annuity or some type of guaranteed income. How that works is called mortality credits, where if you survive up to age 95, as part of buying that annuity, you’re not only receiving some interest and return of premium, but you’re also receiving benefits based upon those who have passed away before you.

I don’t work for an insurance company. I don’t sell annuities. Annuities are a very contentious issue. I completely understand that. They’re often missold. There’s no fiduciary standard by and large. But the only way you can guarantee income for life is with guaranteed income. Social Security is the best annuity around. Anyone who is realistically thinking about wanting more guaranteed income, the absolute first place you have to look is Social Security. It is impossible to buy an annuity with this same type of rate of return.

Annuities should not be purchased for their returns; they are a risk management tool. An annuity is priced based upon two main factors. The first factor is how long you’re going to live, and the second factor is what the insurance companies earn on the funds they’ve invested. Social Security is only based upon one factor. It’s based upon how long they think you’re going to live.

More Efficient Retirement Portfolios

For those of us who build portfolios, too often we take what I call an “island perspective” when it comes to asset allocations. You have your inputs, you have your expected returns, your standard deviations, your correlations, etc. If you put those in, out pops this beautiful portfolio with the efficient frontier, and it says you should allocate 12 percent to small value, 15 percent to small growth, etc.

The problem though with that perspective is that you’re ignoring everything else. Because in reality, the portfolio is only one piece of someone’s total economic worth. A question then becomes, what is the risk of a portfolio that exists to fund a liability such as the goal to have $40,000 per year of income for 30 years? If you do a traditional mean variance optimization, you would define the risk of standard deviation because from a client’s perspective the risk is volatility. But it’s not the only risk. Risk for retirees is also not funding the goal. For a retiree, if they want income for life, adjusted for inflation, inflation is a very important risk characteristic that should be thought about in the optimization process.

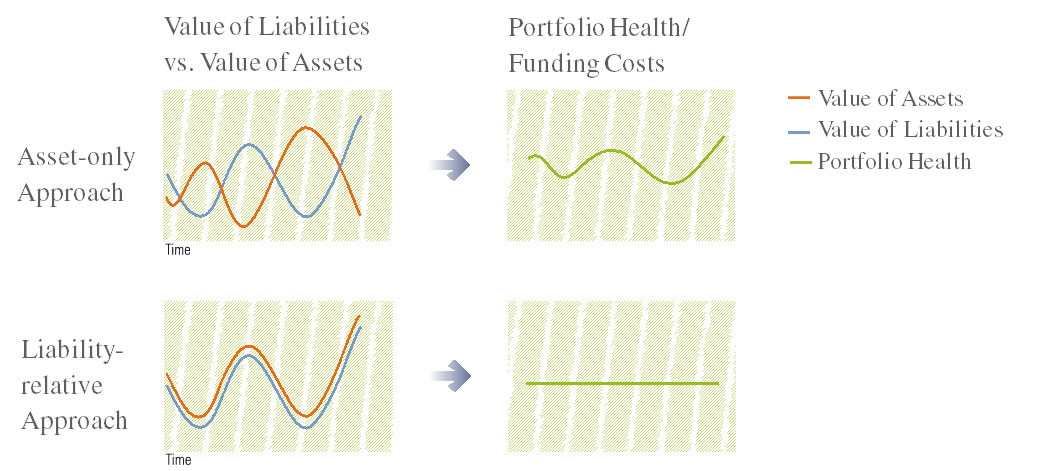

All this leads to this idea of what’s called liability-driven investing or LDI, or “liability relative investing”. The goal for this portfolio for a retiree should be to track that liability over time.

Look at the upper left hand panel (assets only). You see an orange line and a blue line. The orange line is the value of your assets. We’ll call that your 401(k) balance. The blue line is the guide to liability. So we’ll call that the net present value of the cost of retirement over time. What you’ll see in that upper left panel is this zig and zag, where as the orange line goes up, the blue line goes down, etc.

Were the market to go down one year by 10 percent, and inflation was a positive 5 percent, your realized return as an investor in this instance is negative 15 percent. Because your assets went down in value, but your liability increased in value, so the assets are mismatched to funding retirement costs (liability) over time. In sum, for a retiree, the goal is not wealth maximization. The goal is to make sure that they’re going to have their retirement income need paid for when they retire.

With a liability relative approach, if the fundamental goal of the portfolio is to have income for life adjusted for inflation, you want a portfolio that when inflation is low, the portfolio doesn’t have to do as well. But if inflation is higher, the portfolio will need to outperform. That’s what you see in that lower left hand panel, where you’ve smoothed those funding costs over time.

What this leads to is this idea of different efficient frontiers. What are the risks of the goal you’re trying to fund? How do those risks affect the optimal portfolio allocation? For example, you can have two portfolios that are both efficient, but they’re efficient using two different definitions of inflation. One example is that if inflation is a risk to protect against, it has correlations that vary by asset classes. TIPS have a higher correlation to inflation than most bonds do, so TIPS are going to be more efficient at hedging inflation risk than the average nominal bond. There’s other assets like real estate as well.

At Morningstar, we have accumulation portfolios and we have retirement portfolios. For someone who is under the age of 50 or 55, they get an accumulation-focused portfolio. Asset-only portfolios, focused on accumulation, look very different than liability portfolios. Asset-only portfolios are really better geared towards younger investors because younger investors have an excellent inflation hedge through their human capital. But older investors need this inflation hedge via their portfolios, so it really makes a lot of sense to have two different sets of models, one model that is geared towards investors who are in accumulation, and another model geared towards investors who are in retirement.

Key Conclusions

Takeaways for advisors:

- You need to use expected returns and simulations. You really shouldn’t use historical returns for modeling future projections. I’ve gotten into quite a few debates with advisors about this. If you change your model from long-term averages to one based upon expectations, you get an incredibly different perspective on what is a safe withdrawal rate.

- Think about increasing the length of retirement in your models. Your clients are not the average American. The average American, they smoke, they may have some disease or cancer. Your clients, if they’re healthy, and they’re going to live a long time, and most likely they’re wealthier than most. So what this means is that if you’ve got a couple who are both age 65, you should at least use 30 years as the period. Potentially even 35 years.

- Think about modeling different spending levels in retirement, where inflation-adjusted consumption decreases with the retiree’s age. This really does do a better job reflecting the actual consumption of retirees.

- Creating different portfolios for accumulation is not the same thing as efficient portfolios for retirement. There’s different risk factors, things like inflation, which really can lead to different outcomes. One way to easily do this for clients is to have two different sets of models. Have your efficient accumulation portfolios and your efficient retirement portfolios, and allocate them based upon where they are in their overall life cycle.

Takeaways for clients:

- First and most importantly, retirement is the most expensive purchase you’re ever going to make, so you have to know what it costs. If you buy a new phone or a new car, you do all this due diligence on where you can buy it the cheapest. Do the same for retirement, and know it is obviously incredibly complex.

- True failure is not just having any money over a fixed period. It’s not having any money over 30 years. It’s having nothing left when you’re still alive.

- Retirement is far more complex than accumulation, and it really makes sense to bring in a professional when you are thinking about retirement and figuring out what these things cost.