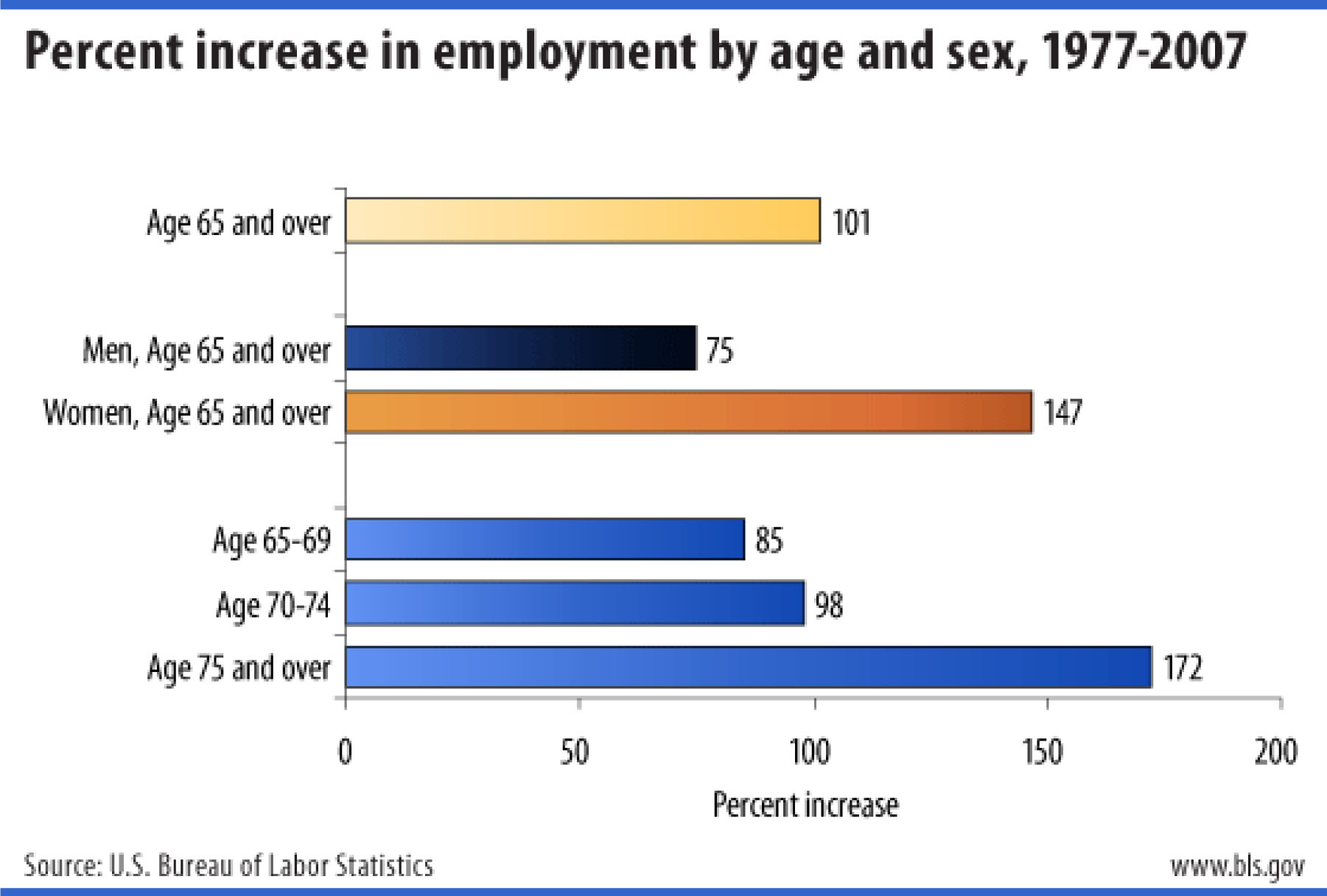

Historically, when you look at when people choose to retire – the age at which they retire – you find very significant spikes at the ages of 62 and 65. Because that’s what Social Security told us was retirement. This chart by the Bureau of Labor statistics for the 30-year period, ’77 to ’07 shows the percent increase in employment by age and sex, male-female.

The increase in employment of people 65 years of age and older is over 100 percent, which means employment has doubled over that 30-year period. Look at the number for age 75 and over. Before you say that was because of the Great Recession in 2008, folks, these numbers are before the markets went down.

This is a fascinating chart. This is the employment level – numbers of people in thousands – ages 55 years and over.

The shaded area, the grey bar – vertical – in the middle of this table is the Great Recession. If this chart hadn’t shaded that grey bar, you would have never thought the Great Recession occurred. If I showed this same chart at different age groups, you would see there was a recession. So some interesting things are happening. In fact, EBRI found in their 2013 survey that 69 percent of individuals expect to work for pay in retirement.

The whole concept of retirement is shifting. What’s interesting is when they dive into that a little further, what they realize is that people are working for pay in retirement for positive reasons. The rationale for solely doing it for financial gain or for money or income is actually a small percentage. However, 47 percent – by EBRI’s numbers – leave the workforce earlier than they planned. Sadly, only 7 percent for positive reasons. Why do people work longer?

The Stanford Center for Longevity, these are their top reasons.

- Working helps to avoid social isolation specifically if the individual is single when they’re older.

- It gives meaning to life. That kind of gets into the idea of purpose. Rush University Medical Center did a longevity study with individuals, almost 1,000 individuals, average age of 80, and found that people who had a sense of purpose in life were 57 percent less likely to die over any given five-year period. There’s something to this. A reason to get out of bed in the morning. Allows use of knowledge and experience. You took a lifetime to achieve what you know. Wouldn’t you want to apply it for a little bit longer?

- It is a source of pleasure. I know it sounds strange for some people when we talk about work, but it’s a source of pleasure for many. A recent study noted that 89 percent of older workers said they enjoyed their jobs. They enjoy it. Why would they want to stop?

- The last reason’s a real interesting one because it has implications for costs and expenses. Working longer helps to maintain health. Those who rank in the top 10 percent for muscle strength among older individuals were a 61 percent lower risk for developing Alzheimer’s disease than in the lowest 10 percent for muscle strength. Every single piece of medical research that comes out seems to indicate that a level of physical and mental activity keeps you healthy, or at least more healthy than if you weren’t doing those things.

In sum, one more year of work is another year of savings; one less year of spending. So you can think of each year of work as almost counting double to helping to maintain or preserve a nest egg.

2. Working Where You Spend

Why work where you spend?

Part time work? Target? Say you work 20 hours, $5 an hour: $100 bucks. If working longer counts double, that’s worth almost $200 a week because you don’t have to take it out of your nest egg. You may get an employee discount. Working where you spend may make your cost of living a little bit lower. I knew a lady whose hobby was knitting. She went into the store and she asked them once: who knits your display models? They said we don’t have anybody and it’s really not consistent, and it’s hard for us. She goes: how about I knit your display models for free yarn and tools? What about people who like to golf? Another person took a job cleaning the golf carts at a course, and it afforded them all the free golf they wanted when they could schedule it. So working where you spend, getting creative, can make a big difference.

3. Minimize or Payoff Debts

So now let’s get back into the planning side. Sing it to yourself right now: I owe, I owe, so it’s off to work I go. You retire debt; debt doesn’t retire on its own. Let’s think of it a different way. You may owe some debt – mortgage, car debt – do the investment markets owe you? Do they owe you a rate of return to help you make ends meet? So one of the first things I discuss with people when we get into these types of conversations, is specifically are you going to retire without a mortgage? Is your house paid off?

Or might you consider selling the big house, moving into something smaller so you can have the house paid off? This is going to make more sense as we advance in age. How many cars? My own parents retired a few years ago, and one of the first questions I asked them was: are you going to keep two cars? They looked at me like I was insane. If it works, obviously there’s savings there: insurance, car expenses, etc. If it doesn’t work, you can always go out and get another car. Well, that was ten years ago. They’ve had one car between the two of them for the last ten years and they’ve saved a lot of money as a result. Because retirement is about enjoying your life, right?

4. Not All Spending is the Same

Let’s talk about two different versions of the same dollar. In your budget – or your spending plan, which is a friendlier term – you have both fixed expenses and you have variable expenses.

Fixed expenses are the spendings that you do all the time, like a mortgage payment, a car payment, a heating bill. Variable expenses are those expenses that rise or fall based upon your choice of behavior. Going on vacation, going out to eat at a different restaurant versus cooking at home. So the first thing I talk about with people is to think about your spending in those two pieces: your fixed expenses and your variable expenses. As a goal, maybe think about working towards immunizing your needs. Your needs are fixed expenses. Those could be your debts, or simply could be your needs.

Every month – even if you have no debts – you’re going to have a heating bill, electricity bill, maybe a cable bill, maybe a phone bill. You’re going to have some bills for groceries, but there’s a difference between hamburger and steak. So you want to immunize your needs. What are our immunization tools? Social Security is an immunization tool. Pension plans are immunization tools. Or perhaps an annuity. These tools are things that give you a fixed monthly income for as long as you’re alive.

There’s another part of the needs here, which is expenses that aren’t usually a part of normal conversation: and that’s healthcare. It’s access to healthcare, it’s not just the ability to pay. We know the statistics that say that your out of pocket expenses during retirement for a couple could be a quarter of a million dollars, and that does not include long term care needs. If your pension and/or Social Security gives you $3,000 a month combined, and you found that your fixed expenses were $4,000 a month, then you might want to consider a $1,000 a month annuity contract.

You immunize your needs, and then you try to optimize for your wants. Optimization is a term that’s used for trying to get the most rate of return for the least amount of risk in an investment portfolio. The reality is we can try to optimize, but we can’t necessarily optimize. For all the software tools out there, they are attempts; they are not guarantees. You want to try to immunize your needs, and then you can have invested assets that have some volatility for your wants, because if the assets stumble, it doesn’t affect your ability to cover your needs.

5. Advanced Life Deferred Annuities

Thinking of it this way, your retirement becomes a lot more comfortable. There’s another phrase that people use in the industry: build a floor and then reach for more. Build a floor of income to cover your needs, and reach for more to try and obtain your wants.

Social Security and/or pensions may give you $3,000 a month, but your needs – not your wants – were $4,000 a month so maybe you want to buy an annuity for that thousand dollars? If advanced life delayed annuities are annuities that are purchased, for example, at the age of 65, but they don’t begin paying out the monthly income until, for example, age 83; or expected mortality for a 65-year-old. So you’re not going to get a payment at all for, in that case, 18 years. These policies cost roughly 15 cents on the dollar, compared to a regular annuity that would start day on one would cost.

Now we can start thinking about chunking out our retirement plan. You could think of this as longevity insurance that you won’t outlive your assets, but a cheap way of paying for it. Now you can start thinking about if you work until 65 or 70 – people are working longer, sometimes they need to – and you have those ten to 15 years before maybe this would kick in. You’re covering your own costs for living the way you want to live; and then you have this nice insurance on the back end.

6. Family Formation and Filial Issues

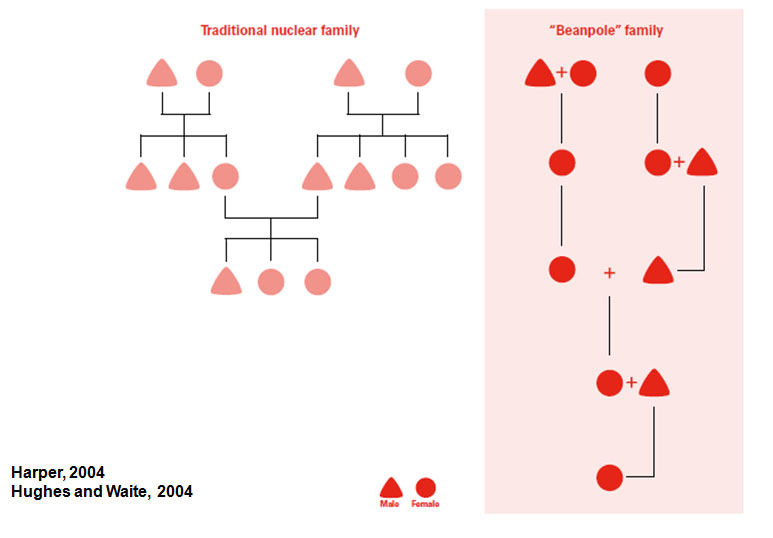

We started to see over the last couple of decades is that family structures are changing. We can look at the past and we can understand what a traditional nuclear family might look like: husband and wife married, three kids, kids go off and get married, and so forth and so on. In the last few years – and this is a global experience, not just US – even in emerging countries, with divorce or fewer children, we’re now having what’s being referred to as the beanpole family. Why does the beanpole family matter when it comes to retirement planning?

We talk about family support, right? Is there potential care in the household? If there are fewer kids, then you may have to pay for more care. I’m not talking about a hospital stay. We’re just talking about going to the doctor’s office. If you’re older and you don’t have the capability of driving to the doctor’s office, who’s going to take you? This also translates into greater pressures and needs on the fewer children that are being born. Who is going to be taking care of that parent? Which child?

I can tell you, if you want to see families torn apart, this is one of the most common situations in which you see that happen. Because typically, one of the children – for whatever reasons – takes the responsibility to be more of the caregiver to the aging parent or parents. Are they being rewarded for that? What I suggest to people is that the children basically make a contract with each other and with their parents, so that the individual who’s taking care of maybe receives some form of compensation. If it’s not a type of compensation like work pay, maybe it’s a little bit larger percentage of the inheritance.

If you want to keep peace in a family over generations, conversations like these need to happen. I show this graphic because filial issues have been longstanding issues in Asian economies. We talk about Japan and the agedness of that society; we talk about what’s happening in China with the one child policy from ’79 forward. But the reality is, in many Asian cultures filial piety is a legal obligation in which children are not just taught to respect their elders and appreciate their hard work of parenting over the years, but they are required to reciprocate that gratitude by looking after them in their old age.

Before you think that this is in the past, China made laws about this in 2013. India’s laws came online in 2007. Singapore has had it since 1999. If the state has to take care of elders because the child doesn’t, then a fine may cover some of those costs. This is a real topic for our culture.

7. Have a Policy for “Ending” Wants

This is not a happy topic, but it is critical. Over half of one’s lifetime worth of health expenses, on average, are experienced in the last six months of life, according to Medicare research. Hence ending wants: What do they look like? Keep me plugged in, or not?

We talk about the increase of dementia. The slippage in cognitive ability as many people get over the age of 75 and 80 is significant. Who is able to pay bills? Who has the right to help with decisions? Who has Power of Attorney?

Or, how will the elder get to the doctor, or even make the appointment? This goes back to the children talking, and maybe a contractual relationship so the family can continue going forward as a family instead of getting divided. This obviously is about many issues, not only expense management. This is also about what people wish, so that when they reach that last phase of their life they can do so not with overhanging questions, but with dignity because they were able to express their desires, and their family could take care of those desires.

8. Life Insurance

Folks, this is not just about assets. Going back to the title of this article, my question is, are you having discussions within your family? Are you having discussions with counselors or professionals in these various areas? What’s the plan?

I’d be neglectful if I didn’t talk about life insurance. Why? This is what life insurance is. Have you ever seen life insurance presented as pennies for dollars? Why does life insurance enter into this conversation? Because it’s a tool, and like any tool, it can be used properly or it can be misused. We all remember that if you have a hammer in your hand, everything looks like a nail. But why might we use life insurance?

What if somebody’s spending wants, not needs, is a bequest motive? For a library, for a school, or they want to leave behind an inheritance. But they’re worried about spending down all their assets. Well, maybe use a fraction of their assets – pennies for dollars – and buy some life insurance, and use the life insurance policies for their bequest motive. That way, they can maybe have more confidence in how they can spend down their nest egg.

How about for leveraging pension or annuity income to life only? For those of you who’ve ever had to make a decision about an annuity, if you retire from a pension system, the question is: Is it just your life or is it you and your spouse, joint and survivor?

As we know, once we get beyond life only annuities, the monthly income guarantees start to drop. What if you look at the difference, and you buy some life insurance that covers the difference so that you can go life only? Maybe we can maximize your pension income. This is a tool. Another aspect of life insurance is there are new products out on the market today that are hybrid products: life insurance and long term care. Historically, standalone long term care policies have been expensive, they have not been very durable, and sometimes the prices change. There are some issues with pure long term care policies.

But you can now, today, buy a life insurance policy with a long term care rider. For example, you might buy a policy that has a face value of a quarter of a million dollars, but that it allows up to $10,000 a month to be used for long term care needs. The life insurance is going to have to pay out a quarter of a million dollars at one point or another, assuming you pay your premiums. Do they care if they pay it out in forms of monthly to cover long term care, or at the end? Let’s say you go into a facility and you end up spending $100,000 for the period of time you were there. When you pass away, the life insurance would pay $150,000 – the difference – to your chosen beneficiaries. This is actually a much more efficient way of covering long term care.

9. Happiness and Control

When we’re younger, we’re a little happier. We feel we have control. When I say younger, I mean going up and until retirement time. As we start approaching retirement, we become a little less certain. Do we have enough money? Have we saved enough? By the way, I happen to find this concept of ‘have we saved enough’ quite disturbing. Why? Somebody’s lived a life, maybe they’ve raised family, they’ve worked, and they’ve maybe helped people and done some really good things during their lifetime.

Why would we want to make them feel like a failure as they go into that next phase of their life that’s labeled retirement because they haven’t saved enough? As if they’re not worthy? This strikes me as horrible. Again, this is why I care about the planning side of the equation; helping to put this in perspective. When people are around their retirement time, they’re not certain, right? They’re not certain. Is it the right time to retire? Do I have enough money? Maybe they’re part of that 47 percent of people retire early but only 7 percent for reasons they want?

Maybe they’re part of that 40 percent that are now retired but they didn’t make that an active choice, be it job access or health issues. Obviously, their happiness is going to be lower. Their sense of control over their life is going to be much less. What’s really fascinating is that the research found that as people get older – 70s and 80s – their sense of well being becomes a little bit more U-shaped. You become a little bit happier as you get older. I don’t know, but maybe this is due to the wisdom and perspective that we gain, and we don’t sweat the small things anymore.

It’s an interesting concept that the research seems to indicate. By the way, the Center for Retirement Research at Boston College has published on this issue that gradual retirement may not equal happier retirement. Before, I had mentioned that maybe you work part time; 20 hours a week instead of full time. If you retire at 65 or 67, or 70, and then maybe you work part time for a few years. The Center for Retirement Research says that you may not actually increase your happiness level. You have to read the fine print. What they say is that the key to happiness about a gradual retirement is your sense of control. If you make the decisions, and you’re making things happen; you’re going to be happier. That’s what the psychologists tell us.