Blaine Aikin, AIFA®, CFA, CFP® – Fiduciary Responsibility Expert

Editor’s note: This article is an adaptation of the live webinar delivered by Blaine Aikin, AIFA®, CFA, CFP® in 2017. His comments have been edited for clarity and length.

You can read the summary article here as part of the 4th Qtr 2017 Retirement InSight and Trends Newsletter, worth 1.0 CE when read in its entirety (after passing the online quiz.

You may also choose to take the full length course The DOL Fiduciary Rule and Your Duty of Care for 1.0 hour continuing education (CE) credit.

By Blaine Aikin, AIFA®, CFA, CFP®, Fi36

There is a famous quote from Supreme Court Justice Benjamin Cardozo where he talks about the difference between fiduciary standards versus rules of the marketplace. He begins with “a trustee” – and whenever he talks about trustee, that is the classic way of thinking about a fiduciary. It is someone who holds assets on behalf of another.

So, “A trustee is held to something stricter than the morals of the marketplace. Uncompromising rigidity has been the attitude of courts of equity whenever they are petitioned to undermine this undivided duty of loyalty by the ‘disintegrating erosion’ of particular exceptions. Only thus has the level of conduct for fiduciaries been kept at a level higher than that trodden by the crowd.” By avoiding those exceptions, we can keep the standards for fiduciaries higher than the standard or the morals of the marketplace.

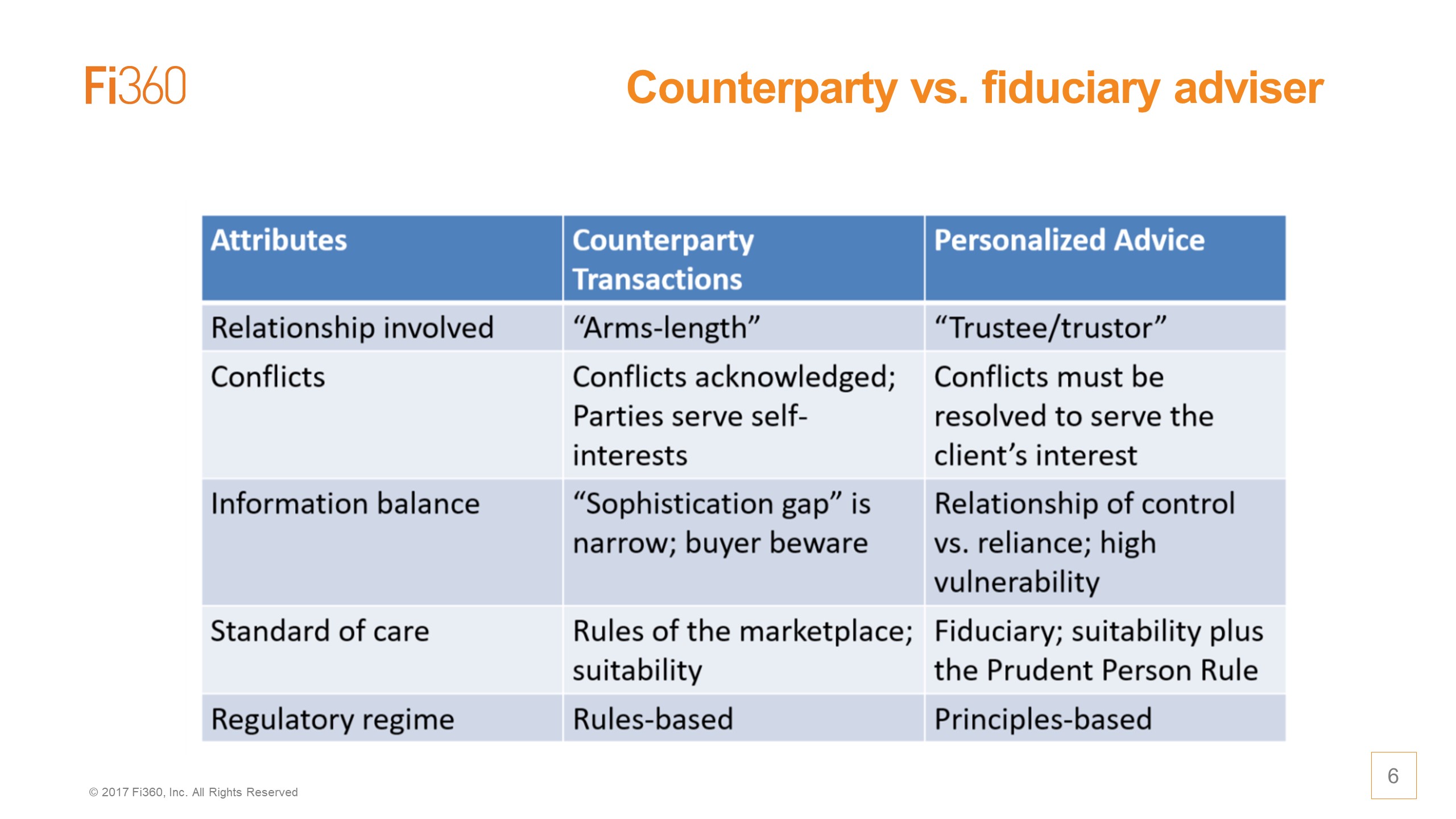

What are the Morals of the Marketplace Versus the Fiduciary Standard?

When we are talking about the rules of the marketplace, we are talking about counterparty transactions; the relationship involved is one that we classically think about in a transaction, where it is very much arms-length. If you are going into a transaction with someone else, you typically know that there are conflicts involved. Both parties are trying to serve their self-interests. Moreover, usually, the sophistication gap is relatively narrow.

The buyer can beware here. Imagine shopping for a car; it is not that complicated to research cars, and whenever you go into the showroom, you know that there’s somebody on the other side of the transaction that you are dealing with. The standard of care is the rules of the marketplace. It is suitability-based. It is quite a product-protection type of regulation as opposed to something more significant. It is often very rules-based, where it is highly specific: “thou shalt do this, or thou shall not do that.”

When we are talking about personalized advice in that column on the right-hand side, this is the fiduciary relationship that Cardozo was talking about. We have a trustee: someone who is responsible for taking effective control of the assets of an individual, who in this case would be the trustor, the one who is giving up some measure of control to the trusted advisor. In that circumstance, conflicts must be resolved in the client’s interest because of the sophistication gap—the information balance—is very disproportionate. You have a relationship of control and reliance with high vulnerability on the part of the client, as opposed to a regular counterparty transaction.

That is why we have a fiduciary requirement. It is not only suitability; it also requires the Prudent Person Rule to come into play. It is not just duty of loyalty, it is also the duty of care, and the Prudent Person Rule is something we are going to be talking a good bit about. The Rule is highly principles-based. It encompasses the idea that you are held to two core standards: the duty of loyalty, and the duty of care.

Three Levels of Regulation

What are the duties of loyalty and care? They are straightforward, and from these, many other duties flow.

For the duty of loyalty, the obligation is to serve the best interests of the client and avoid conflicts of interest. I like this definition: a conflict of interest is best thought of as a circumstance that makes fulfillment of the duty of loyalty less reliable. Essentially, we have temptation involved, if you will.

The duty of care, which is going to primarily be the focus of this article, is to act with the skill, the diligence, and the sound judgment that is reasonably expected of someone serving in a similar capacity. The obligation is to be able to produce the state-of-the-art. The proof is in the process applied, rather than the outcome. You can almost think of this like “despite the doctor’s best efforts, the patient died.” That is the sort of standard applied here.

If you do all the right things, there could still be a crash in the stock market or something where, at least on an interim basis, things did not go as planned, but you did everything right in the process as an advisor. That is what the obligation of a fiduciary is.

Now this provides an interesting basis for thinking about regulation as well. When you think about who the ideal advisor for most clients would be, most investors would say it is someone who is both trustworthy and competent, and those characteristics directly relate to the duty of loyalty and the duty of care.

In the current financial services environment, we have three levels of regulation. There is a non-fiduciary standard that’s at the Exchange Act level. This is for broker-dealers; this is for the counterparty transaction. There is no fiduciary obligation. It is order-taking; it is highly transactional.

When we move into the realm of advice, it is like going to an attorney or a doctor. When you go to your financial advisor, you expect that they are going to act in your best interest because of that information gap mentioned earlier. The Investment Advisers Act of 1940 is very much a fiduciary act that requires investment advisers to act in the best interest of clients.

However, because you are dealing with a client, that act is not quite as high a standard as what you find in the retirement marketplace. In the retirement marketplace, the adviser is acting once removed from the end-investor (participant). There are other fiduciaries – for example, the plan sponsor in a retirement plan – who need to select their fiduciaries – those that they are sharing fiduciary obligations with, like an adviser or an investment manager. All fiduciaries need to choose very wisely because they are one step removed from the investor.

The highest standard is really under the ERISA fiduciary standard, and that is what the DOL Fiduciary Rule is all about because it is obviously in the retirement space.

Why then, did the DOL act? What they said right at the beginning of the rule-making was that they observed that instead of ensuring that trusted advisers were giving prudent and unbiased advice (due care type) and adhering to that duty of loyalty in accordance with fiduciary norms, there were a multi-part series of technical impediments to fiduciary responsibility in the Rule. In much simpler terms, there were loopholes within the definition of who a fiduciary was.

What the DOL Rule does is change the definition to make it apply more broadly. The DOL felt that contrary to legislative intent under ERISA, advice was being given without fiduciary accountability. The solution that they determined was important was to tighten the definition of fiduciary conduct. Now whenever you provide investment advice that is personalized, you will be held to a fiduciary standard as an investment adviser.

However, they also did one other thing: they made specific refinements to the rules. They added some exceptions and exemptions to accommodate the business practices of broker-dealers. This is somewhat controversial because ERISA is the highest fiduciary standard, and the rule has been that you cannot have a conflict of interest unless there is a specific, prohibited transaction exemption that allows that conflict to exist. That is an important thing to keep in mind as we talk further about the DOL Rule.

How Does the DOL Fiduciary Rule Work?

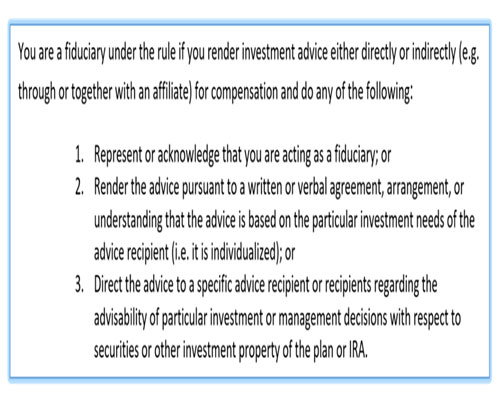

It all starts with answering the question, “Are you, in fact, a fiduciary?” The original definition out of ERISA had a five-part test to it. Two of the parts said you had to be giving advice on a regular basis, and that advice had to be the primary source for decision-making. It was based on that advice being used by an investor to make a decision.

Under the new definition, you are a fiduciary under the Rule if you render investment advice either directly or indirectly. In other words, an affiliate of yours could be giving the advice as well. You are doing it for compensation, so this rules out those cocktail conversations. However, then if you are giving virtually any type of investment advice, you will be held to the fiduciary standard under the revised definition, as shown next.

Now, this is a significant change. The loopholes have been closed. As you may be aware, the DOL Rule that came out was accompanied by a great deal of explanatory information, so much explanatory information that it spans about 1,000 pages. It starts with the definition of fiduciary, so you want to remember, “You are an investment fiduciary if you provide advice.”

The DOL could have just said that and moved on to describing the Rule, but it went a step further. It did elaborate in the Rule about certain things that are not fiduciary communications that you can provide – for example, education that is not accompanied by personalized, specific advice. That is not a fiduciary communication. Alternatively, when someone explains how a retirement plan works or generally how asset allocation works, that is not considered a fiduciary activity. Rather, that is education, a non-fiduciary form of communication.

However, you have to be careful that you do not slide from one activity to the next. For example, you might be giving a presentation as an investment person in the front of a room to a group of employees. You are providing education, and then somebody walks up to you afterward, a plan participant, and says, “Yeah, I think I get what you are saying from what you described so far, but let me tell you about me, and what should I then do?” As soon as you answer that question—what the individual should do—you’re giving personalized advice, and you have slipped into that definition of fiduciary.

Another exception to the Rule is if you are only placing an order; that is similar to a counterparty transaction and not a fiduciary activity. Similarly, there’s a platform providers exception. For example, assume a retirement plan puts out a request for proposals and says, “We want to implement a retirement plan. Here are the specific types of requirements we have for a platform provider.” A provider comes in that offers retirement plans and says, “I have such a plan. Here’s how it matches up against what you need. Would you like me to do this for you?” This example is tantamount to a counterparty transaction, where you are order-taking regarding what they are looking for.

There is a critical exception to the definition to be aware of: support services provided by plan sponsor employees. If a plan employee provides basic support to the participants, they are not considered a fiduciary if they are not registered investment advisers who may have another job on the side.

There are exceptions for general communications, such as someone who is a radio talk show host generally talking about financial topics. They are not an adviser if they are not giving personalized investment advice. Those are all called the “non-fiduciary communications.”

What was the DOL Trying to Address?

A fiduciary investment adviser is someone who meets the definition that we just covered. For ERISA, then, the definition applies. The fiduciary duties of loyalty and care apply, and all the subsidiary type duties that are associated with those standards.

An essential concept under the DOL Rule is that impartial conduct standards must be followed. These standards are how someone goes about giving advice in a way that protects the duty of loyalty and makes sure that duty of care and subsequent competence standards are being followed.

There are other aspects of the Rule that are important. How the adviser is compensated comes into play, and this goes back to those “disintegrating exceptions” that Judge Cardozo talked about. Someone who has non-level compensation can still be a fiduciary if they do certain things under this Rule. This is a lightening up of the Rule to accommodate commission-type income on the part of someone providing advice. Moreover, here there is a prohibited transaction exemption known as BICE – it is the Best Interest Contract Exemption – that would be required under most circumstances for non-level compensation.

That exemption adds a few more hoops for an adviser to jump through to make sure that those fiduciary duties are protected. If the adviser is a level-fee adviser – where someone does not have the conflict associated with what can be paid varying by what the advisor recommends – then he or she avoids a conflict of interest situation and have no conflict associated with variability in compensation. Either they do not need a prohibited transaction exemption, or there’s a streamlined version that could come into play, such as with an IRA rollover.

Assume a plan participant goes to an adviser and says, “Hey, I’m thinking about retiring. Should I take a rollover or not?” Well, there’s an inherent conflict there, even for a level-fee adviser. If they were not doing business with the individual before, but they would be afterward if they accept this IRA rollover, then the adviser is going to make more money. Now they are conflicted if they give advice such as “Oh yes, you should roll that IRA over.” In that circumstance, they do need to make sure that they have disclosed that conflict, they have applied impartial conduct standards, and they have gone through the steps necessary to make sure that the duties of loyalty and care are preserved.

Where Does the DOL Rule Stand Now?

The DOL Rule has been on has been on a long and arduous road. The DOL first came up with the original fiduciary definition starting in 1975 and all the way through 1978. It was not until 2010 that the DOL proposed to tighten the definition in the way that I have described. Since then, there has been a whole lot of back and forth.

As of June 9th of this year (2017), the main Rule provisions became applicable. Some people do talk about the Rule not being implemented or delayed, and that there are specific provisions of it that are delayed that haven’t yet taken effect. However, the primary requirements of the Rule, including the definition and the obligation to conduct these impartial conduct standards, are in effect now. The time between June 9th and January 1st, 2018 is known as the “transition period.” Some of the more onerous provisions of those prohibited transaction exemptions were to come into play by that January 1, 2018, date.

Now there is a proposal by the new administration to push that final applicability date out 18 more months until July 1st of 2019. That delay has not been made final yet, but it looks like that is about to happen. There is the possibility of a lawsuit by consumer groups to try and roll back that delay, but it is vital that you understand where we are. So essentially, we are in the ninth inning and headed for extra innings, I guess you could say, under the Rule. The most important thing is to recognize that the fundamental Rule is in effect now.

During the transition period, there are certain things that don’t apply, and these are what are considered to be the more controversial and more onerous elements of the Rule. Under the prohibited transaction exemption known as BICE – or the Best Interest Contract Exemption – by the time that the Rule is to be finally implemented, there would need to be a designated compliance person in the financial services firm who’s providing the advice, and there would have to be a written acknowledgment of fiduciary status by those who are providing advice. Material conflicts of interest would have to be disclosed, and any limitations of what products they could offer would also have to be disclosed.

Due diligence would have to be documented. In other words, that duty of care – those impartial conduct standards – would have to be documented so that there would be a record of how prudence was applied and demonstrated. Certain other records would also have to be maintained.

There are a couple of other prohibited transaction exemptions that are also impacted during this transition period. These relate to such things as annuities and principal transactions. The delay does address these most controversial elements of the Rule, but it also protects investors’ interests. Because the main body of the Rule went into effect, it preserves the fiduciary principles while making certain practical concessions to make sure that advice is more broadly available.

During the transition period, some people have mistakenly latched onto the idea that this transition period is one of nonenforcement. They may have good reason to believe that because the DOL said that they would be lax in enforcement and heavy on education and assistance during the transition period. However, that is conditioned upon the adviser and the adviser’s firm working diligently and in good faith to comply. Accordingly, the DOL issued a field assistance bulletin that makes it quite clear that you have to diligently and in good faith seek to comply.

Also note that there is already a private right of action under ERISA, so assets that are held directly in ERISA plans are already subject to lawsuits for breaches of fiduciary responsibility, for example. Also, the DOL has direct regulatory oversight and can have regulatory actions taken against those who violate the fiduciary obligation. Concerning individual retirement accounts, which are also covered under the Rule, the avenues for investors to have recourse are much more limited because they are not ERISA accounts.

FINRA, however, does oversee brokerage accounts, including IRAs, and the Number 1 complaint in a FINRA arbitration case is a breach of fiduciary responsibility, even though broker-dealers do not traditionally have that fiduciary obligation. A plaintiff will typically argue that “Advice was being given. This was not a counterparty transaction,” and they will seek to hold the adviser accountable as a result of that.

Now that we have a Rule in effect that describes precisely what an adviser is, I think those FINRA arbitration cases will probably step up for those who to try to argue that they were not acting in a fiduciary capacity.

What Do You Need to Do to Comply?

If you are investment advisor or a plan sponsor, this will give you some idea of what the obligations under the Rule are and what to look for with respect to the advisers that are working with you to help you comply with the Rule, with your obligations.

“Impartial Conduct Standards” are the key to compliance with the Rule. Under the DOL Rule, the DOL said that impartial conduct standards under this Best Interest Contract Exemption require financial institutions and their advisers to do three things.

- The first is to comply with the Best Interest standard. As you look at the three components of this, you must act with prudence. That then points directly to the fiduciary duty of care, and the duty of care is right there next to loyalty regarding the core obligation that every fiduciary has.

- The advice must be individualized; in other words, you must know what it is that the end-investors are seeking to accomplish. The conduct must conform with the fiduciary duty of loyalty; in other words, conflicts must be managed. The next one is to charge only reasonable compensation. Your compensation as an adviser must not be excessive – some might even say unconscionable. That is why you get to a reasonable concept in the standard; if the compensation is too unreasonable, it is pretty apparent that this was not serving the client’s best interest.

That presents a problem under ERISA generally because there is a requirement under impartial conduct standards to ensure that only reasonable compensation is being taken for the services that are being rendered. The judgment of reasonableness is a matter of facts and circumstances.

- Finally, the obligation is not to make misleading statements about the investment transactions or your compensation or the existence of material conflicts of interest or any other matters that are relevant to decision-making. Notice the word “material” in here. Material is information that someone would want to know before deciding as to whether to accept that advice. They would want to know, “What are the compensation ramifications of the advice that’s being rendered? What conflicts might exist? What are other matters that could influence whether I’m going to take your advice or not?” Those are the significant three requirements of impartial conduct standards.

Note that while this is specifically talking about prohibited transaction exemption requirements, and this phrase, “Impartial Conduct Standards,” was mainly assigned as it relates to that, Impartial Conduct Standards are virtually always required under a fiduciary standard. It really is the processes that need to be in place to protect the duties of loyalty and care.

Whenever we talk about that first obligation under the impartial conduct standards, that is merely the obligation to conform to the Best Interests standard. Moreover, here we have three parts involved in this as well.

- The advice has to be prudent, it has to be individualized, and it must adhere to the duty of loyalty. How do we demonstrate this prudence or duty of care? It should signify the application of generally accepted investment theories and practices.

Just like when you go to the doctor, you would expect that they would be up-to-date on the state-of-the-art in medicine, that is what’s required here for an investment advisor. They need to be current on what is considered state-of-the-art.That begins with due diligence. This is the obligation to research the alternatives that are available to the decision-maker, whether that is a plan sponsor or the plan participant. Add to that the assurance of reasonable cost and compensation. That is a standard fiduciary obligation, to match up compensation for the services that are rendered.

- Next, advice must be individualized. It is the obligation to consider the client’s objectives, risk-capacity, tolerance, and their needs in retirement. One also needs to consider the prevailing circumstances, such as the plan and account options. How much money should be deposited into the account over the course of time, and what would be prudent under those conditions? Market and economic conditions can influence the composition of the available investment options as well and specifically to the individual plan or the individual participant.

- Lastly, there is adherence to the duty of loyalty. We have talked a good bit about that. Avoid conflicts of interest when possible. We mitigate those conflicts that might not be avoidable by using something like the prohibited transaction exemptions. You must disclose costs, conflicts, and any other material information, and there is a monitoring obligation that it must be consistent with the law and governing documents. Monitoring is typically expected of a fiduciary unless it is specifically excluded with the client’s understanding. There is an obligation to document all of this so that if you are ever called into question, you would be able to establish your record of procedural prudence as an investment adviser.

True Retirement Professionals are Trustworthy and Competent

The two key attributes that professional advisers must have are to be trustworthy and competent, adhering to the duties of loyalty and care. When it comes to financial advice, all clients expect that the advice will be objective and competent. This is where I think we are looking to place our focus here – in that service component of all true professions.

The DOL Fiduciary Rule is in effect right now. While there is a part that is delayed, this is not something that can be set aside – that is, there are obligations that I described earlier that are important for you to follow now if you are an investment advisor. For those who are plan sponsors, be aware that these obligations are now in effect and that you can have a reasonable expectation to believe that they will be fulfilled.

Many people think the transition to a broader application of the fiduciary duty as something that is burdensome and something that means just more work. The reality is that whenever someone is seeking a doctor or an attorney, they look for those who are most expert in the area of need. To the extent that an adviser can model these fiduciary principles in processes – for example, with particular expertise in the retirement space – that can be very differentiating in the marketplace. It also starts to put the onus on those that are in the field of investment advice to elevate their game, if you will. When the bar has been leveled to where fiduciary obligations are required widely, think about which credentials might differentiate you in the marketplace that signify levels of competence and ethical obligations associated with being a professional adviser.

About Blaine Aikin, AIFA®, CFA, CFP® – Fiduciary Responsibility Expert:

Blaine Aikin, AIFA®, CFA, CFP® is the Chief Executive Officer of fi360. Fi360 is a national and international leader in the field of investment fiduciary responsibility, providing training, Web-based analytical tools, and resources for those who manage money on behalf of others.

Blaine’s specialties include fiduciary responsibility, investment management, financial planning, public policy and management. His goal as Executive Chairman of fi360 is to assure that fi360 provides exceptional professional development programs, investment and business management tools, and business and industry thought leadership to improve the decision making of those who manage money on behalf of others. fi360 seeks to promote a culture of fiduciary responsibility to align the interests of investors and investment professionals.

Blaine is the author of numerous articles on the subjects of fiduciary responsibility and investment management, and the author of the monthly Fiduciary Corner column in InvestmentNews magazine.

Are you looking for a retirement speaker for your next conference, consumer event or internal professional development program? Visit the Retirement Speakers Bureau to find leading retirement industry speakers, authors, trainers and professional development experts who can address your audience’s needs and budget.

©2018, Blaine Aikin, AIFA®, CFA, CFP®. All rights reserved. Used with permission.