Editor’s note: This article is an adaptation of the live webinar delivered by Roy Ramthun and Aaron Benway in 2017. Their comments have been edited for clarity and length.

You can read the summary article here as part of the 2nd Qtr 2017 Retirement InSight and Trends Newsletter, worth 1.0 CE when read in its entirety (after passing the online quiz.

You may also choose to take the full length course Boost Retirement Security with HSAs: Why Financial Planners and Advisors Should Add HSAs to Client Retirement Strategies – Roy Ramthun and Aaron Benway for 1.0 hour continuing education (CE) credit.

By Roy Ranthun, MPH, “Mr. HSA” and Aaron Benway, CFP®, MBA

Couples who are 65 years old and retiring today are projected by Fidelity to need $260,000 in retirement to cover all of their out-of-pocket costs for the rest of their life, after what Medicare pays. Medicare also does not include long-term care. For those 45-year-old couples today, the United Health Foundation suggests that at age 65 they will need almost $600,000 for out-of-pocket healthcare costs in retirement.

The Employee Benefits Research Institute found that for a 50/50 chance of having saved enough money to cover out-of-pocket expenses in retirement, a 65-year-old man will need over $72,000 set aside by age 65 and a woman will need $93,000. To raise the likelihood to a 90 percent chance that they will have sufficient funds to cover the out-of-pocket healthcare expenses in retirement, the numbers increase to $127,000 for men and $143,000 for women. The Employee Benefit Research Institute also suggests that Medicare will cover only about 65 percent of retirement healthcare expenses, though its ability to do so is at risk as Medicare’s trustees tell us we’re ten years away from insolvency for some portions of the program.

The remaining expenses that will not be covered by Medicare – your out-of-pocket expenses – include things like your premiums, your deductibles, copays, coinsurance, and supplemental costs such as Medicare Advantage plan premiums, or dental and vision care. In sum, Medicare is not going to cover a substantial portion of healthcare expenses in retirement.

With these dynamics at work, we think there’s a need for a health savings strategy. This naturally presents itself as another opportunity for financial advisors to assist and engage with their clients. This could mean such things as helping grow your clients’ healthcare savings balances, implementing more tax efficient strategies – and this includes withdrawals as well – assisting with allocation decisions, and suggesting strategies on how to address paying for retirement healthcare.

What is a Health Savings Account (HSA)?

An HSA plan couples a qualified high deductible health plan to an IRS-defined, tax managed savings vehicle. Under the guidelines, if the plan itself meets the definition of a qualified high deductible health insurance plan, then the insuree tax payer can open an HSA. The health insurance plan and HSA are meant to work in tandem. The HSA, like the more traditional or more familiar Flexible Spending Account (FSA), helps you pay deductibles, but it also features tax-deductible deposits and tax-deferred growth, which is what differentiates it from a FSA. It continues to offer tax-free funds for medical care, both now and in the future, which we’ll get into later.

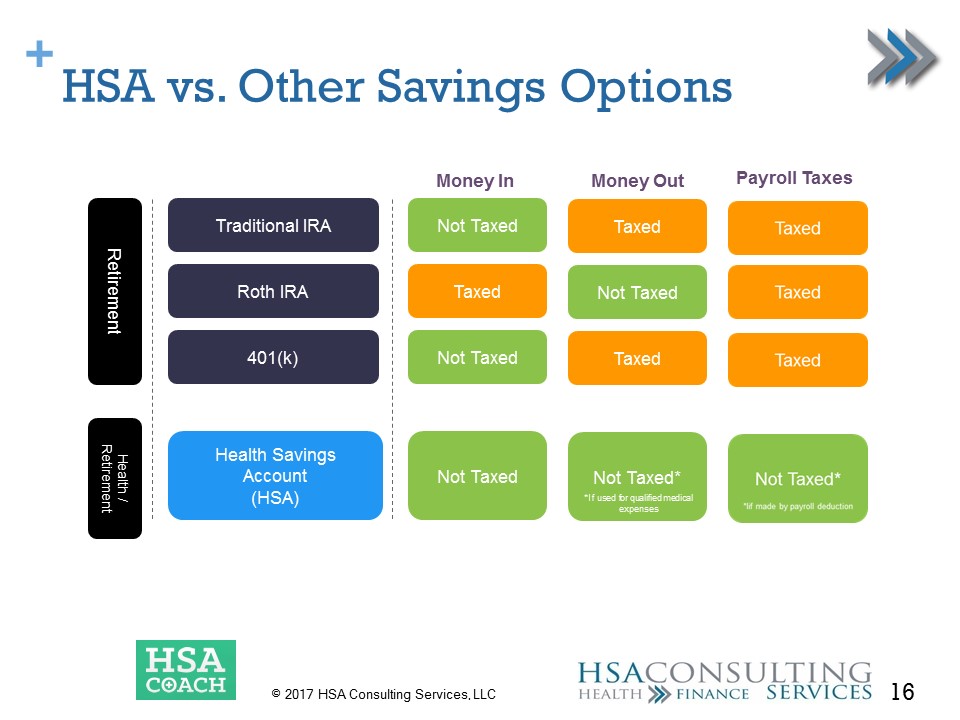

Here we want to compare a health savings account to other more traditional retirement plans such as an individual retirement arrangement (IRA), a Roth IRA, or a 401(k).

Typically, saving in tax-deferred accounts is just a strategy of paying me now or paying me later through the lens of the U.S. Treasury. We add a third column, payroll taxes, because since it doesn’t impact traditional retirement plans, it’s not often talked about. But lower payroll taxes for both the employer and the employee is an additional benefit of using the high deductible plan/HSA combination. You’ll notice that for qualified medical expenses, the health savings account, which is the bottom row, is the only plan not taxed when money is earned, money goes in, or money goes out.

Many HSA providers – not all of them – will restrict the funds available to invest in. You can certainly find a few that don’t. Unlike a FSA, which is a checking account whose funds expire at the end of each year, an HSA can be invested in assets that look very familiar to those who already own an IRA or 401(k) or both, such as stocks, bonds, mutual funds, ETFs, or real estate (via funds, that is).

If you haven’t been following HSAs, they are growing very rapidly. Over the last five years, the number of accounts has tripled to over 20 million as of the end of 2016, and that growth trend has been on a tear of about 20 percent per year. There were around $37 billion in HSAs as of the end of 2016. Based on these current growth trends it is expected there will be $53 billion dollars in HSAs by the end of 2018.

Employer Health Insurance Plans and Health Savings Plans (HSAs)

An HSA needs to be paired with a qualified high deductible health plan. Employers are increasingly offering this option, and in some cases, making this the only option that the employees have when choosing their health insurance. Mercer suggests that by the end of 2019 over 72 percent of employers will be offering health insurance plans that can be paired with an HSA. A third of all employees are enrolled in these types of plans as of the end of 2016.

These trends are largely driven by rising health insurance costs. Employers are struggling to keep annual rates of cost increases in the single digits. The main way they’re doing that is by raising deductibles to keep premium increases at more manageable levels. You have to wonder what premium increases would be if deductibles remained static.

Around 10 percent of employers offer high deductible plans as the only choice for their employees. This is clearly being driven by larger employers, with middle-sized employers and smaller employers increasingly looking to these options as a solution to their rising healthcare costs. So many employees are going to find themselves where they are now eligible to have an HSA. This trend is likely going to continue, so position yourself to take advantage of it.

Why are employers switching to these plans? Every September, the Kaiser Family Foundation and Human Resources Education Trust publishes an analysis of employer-sponsored health plans, and they have a whole chapter devoted to high deductible plans. They compare them to the more traditional plans with lower deductibles, and in the most recent survey found that the premium difference is on average about 13 percent less. This saves both the employer and the employee money that can then be available to deposit into HSAs rather than be paid to the insurance company in the form of premium. Average employee contributions to insurance premiums are $1,746 less and average employer contribution to HSA accounts is $1,208. The total “free” money available to then contribute to an HSA is approximately $3,000.

A more recent study from Fidelity suggests that employees saving in their HSAs are not cutting back on their 401(k) contributions, so their overall savings rates are higher compared to those who only save money in a 401(k). In addition, nearly 90 percent of the HSA participants either maintained or increased their 401(k) savings after they enrolled in the HSA. This is powerful evidence that an HSA is an additional retirement planning tool, and people are starting to understand and take advantage of it.

Why Are Health Savings Accounts (HSAs) such a Great Saving Opportunity?

A few years back the Employee Benefits Research Institute analyzed the potential accumulations in an HSA account given various time horizons up to 40 years, with different rates of return assumptions. Annual contributions to an HSA over 40 years at 7.5% returns can accumulate to over $1 million. The power of being able to invest additional funds tax free provides an opportunity to put aside significant funds to supplement retirement expenses.

There are many advantages to saving in an HSA:

- This is the single-most, tax-advantaged account. Somewhere along the way with most other retirement accounts you pay taxes. With HSAs, the money contributed is tax-deductible, money taken out for qualified expenses is tax-free, and earnings grow tax-free. 2017 contribution limits are $3,400 for individuals and $6,760 for families, plus another $,1000 for those over age 50.

- There are no required minimum distributions for HSAs.

- They are completely portable, like an IRA. Unlike a FSA, which you leave behind when you leave your employer, the HSA goes with you.

- There is no expiration to this account, even after you die. It can be transferred tax-free to your spouse who can continue to use it. If your spouse is no longer living, it becomes an asset in your estate and can go to other beneficiaries.

- Another huge advantage is that at age 65, you are no longer subject to penalties for taking your funds out of the HSA and using them for non-healthcare expenses. However, ordinary income taxes will apply. At this point, an HSA looks no different than having put money into an IRA, which is also taxable for these types of withdrawals.

Portability is a very strong feature of the HSA. Account holders can decide which financial institution holds their account; you don’t have to stick with the employer-chosen HSA account if you don’t like certain features, although I do recommend that you continue with that account if the employer is contributing money and paying fees. In other words, you will have to accept the provider the employer has chosen to accept payroll deduction deposits if you want the benefit of reduced payroll taxes. At any time, you can move money throughout the year to a different institution; there are no vesting restrictions.

You can continue to contribute to your HSA if you are enrolled in an HSA-qualified high-deductible plan until you enroll in Medicare at age 65. There are a growing number of individuals who may be able to delay their enrollment in Medicare because they work for a larger firm (20+ employees) that provides HSA-qualified coverage, so they could continue to make HSA contributions beyond age 65. A couple things to keep in mind before that is done: first make sure you have creditable coverage from your employer so you are not faced with any late enrollment penalties in Medicare Part B and Part D at a later date, and second, you must delay taking Social Security because of its linkage to Medicare Part A. The minute you take Social Security before your full retirement age, you are going to be automatically enrolled in Medicare Part A at age 65.

Depending on our level of income we may be forced to deal with “means testing” of Medicare Parts B and D premiums. The good news is that HSA withdrawals are not reported as income, so they aren’t included in the income that determines premium surcharges. There are tiered income brackets for those earning above $85k for singles and $170k for those married filing jointly that determine the surcharge. At higher incomes, Part B premiums (currently $150 a month) can double.

How Health Savings Accounts Can Be Used Tax-free to Pay Expenses

There are many ways out-of-pocket medical expenses can be paid for tax-free with HSA funds. If the HSA did not exist, expenses might have to be paid with dollars taxed upon withdrawal from a retirement plan.

- Medicare premium surcharges are an allowed expense.

- Medicare Advantage Plan premiums can be paid with HSA funds. A third of Medicare beneficiaries are enrolled in one of these private options to traditional Medicare. (Medigap supplemental plan premiums are excluded).

- Qualified out-of-pocket expenses not covered by Medicare are allowed expenses.

- Long-term care insurance premiums and long-term care expenses are eligible to be reimbursed tax-free with HSA funds.

- Allowed expenses include not only those incurred by yourself but also your spouse and any dependents you may have at that point in your life.

In addition, the HSA tax penalty for nonqualified withdrawals goes away at age 65 and essentially turns the HSA into a 401(k) or IRA where you simply pay ordinary income tax on withdrawals that are not for qualified medical expenses.

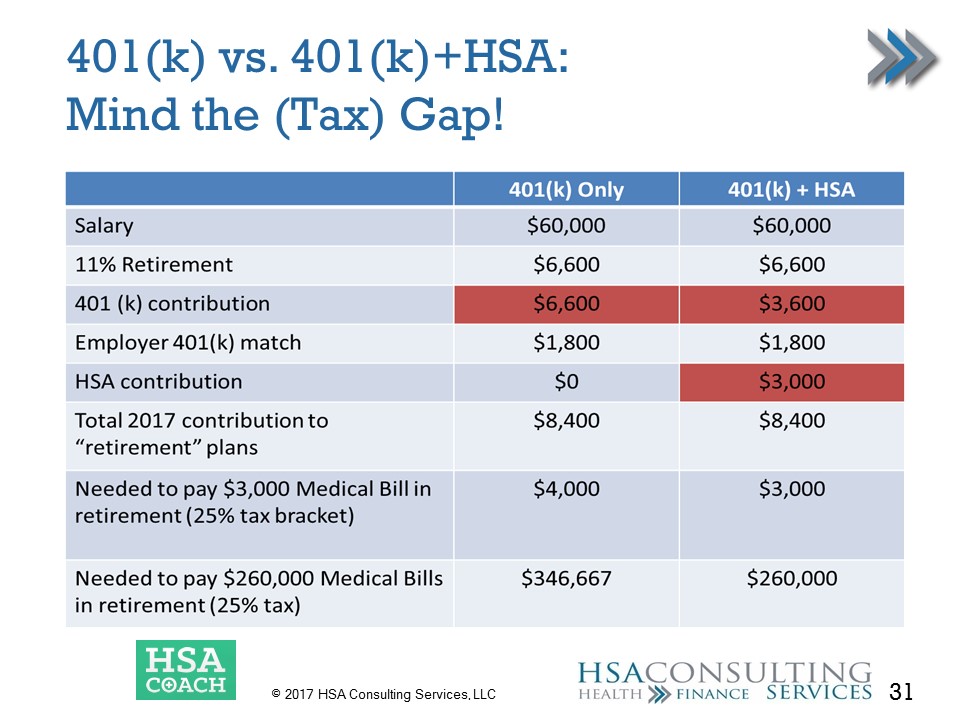

Here is a high-level example of the tax impact on someone using only a 401(k) to save for retirement versus a 401(k) and HSA combination. We assume a salary of $60,000, which is around the median income for a family of four, an 11 percent retirement contribution, and an $1,800 employer match. Highlighted in red is an HSA contribution of $3,000, which is roughly equivalent to the sum of what the average employer contributes to an HSA and the premium savings between a traditional PPO plan and a high deductible plan. We also assume an annual 401(k) contribution of $8,400 a year.

Assume there is a $3,000 medical bill in retirement. In a non-Roth 401(k)-type environment, you would pay taxes on funds withdrawn to pay the bill – $4,000 at a 25% bracket – versus only needing $3,000 from the HSA. Because funds can be withdrawn tax-free when needed, you need less saved to fund future retiree health expenses.

“Shoe boxing” is a strategy that recognizes there is no time limit on withdrawing funds for a qualified medical expense. Let’s say little Johnny, your tax dependent, falls out of a tree and breaks his arm. You end up with $1,000 medical bill as a result. You can choose to take the $1,000 out of your HSA today or instead allow that $1,000 to stay in the HSA until retirement. The IRS expects the taxpayer to maintain records so that in the event of an audit, you can demonstrate that you reimbursed yourself the qualified medical expenses from little Johnny’s fall. The IRS doesn’t require you to submit these expenses; just maintain them. For taxpayers with sufficient cash flow, paying today’s health expenses out-of-pocket can be a tax efficient savings strategy for your HSAs, because it allows you to use them as a future IOU.

An HSA is owned by the individual taxpayer. It may be sponsored by the employer, but the account owners themselves have the ability to do a trustee-to-trustee transfer at any time if they’re not happy with the HSA provider’s investment selection. In addition, FSAs cannot be used in combination with a health savings account. A limited purpose FSA, designed to cover medical and dental expenses, can be coupled with an HSA and works as a traditional FSA so the funds disappear at the end of the year if you don’t use them. Those who have this option have another way to maximize their use of the tax code to their advantage.

Some advisors recommend that after contributing enough to get the 401(k) match, put the next incremental marginal dollar into the HSA, maxing that contribution before returning to the 401(k) or IRA.

Key Takeaways

HSAs are here to stay and are likely to be improved on or expanded in the years to come. Growth in the high deductible healthcare plans coupled with an HSA is not going to go away. Your clients will increasingly be exposed to high deductible plans and HSAs, so there is a financial planning opportunity that will continue to grow in the future.

About the authors:

Roy Ramthun, MPH, “Mr. HSA”, is the President and Founder of “Ask Mr HSA”. Roy is a nationally-recognized expert on Health Savings Accounts and consumer-directed health care issues. He is an active advocate for consumerism in health care and is a frequent speaker at conferences and seminars around the country.

Mr. Ramthun has over twenty-five years of health care and public policy experience, both in government and in the private sector. He led the U.S. Treasury Department’s implementation of HSAs after they were enacted into law in 2003. President George W. Bush then tapped Mr. Ramthun to be his health care policy advisor at the White House, where he developed the President’s proposals to expand HSAs while overseeing the implementation of the Medicare prescription drug benefit (Part D). He has served on the staff of the U.S. Senate Committee on Finance and the U.S. Health Care Financing Administration (now known as the Centers for Medicare & Medicaid Services). He also spent eight years with Humana Inc. and led the West Health Policy Center for two years.

Aaron Benway, CFP®, MBA is Co-Founder of HSA Coach. Aaron is also Founder of AB Financial which offers financial planning and investment management guidance. Aaron is passionate about health, financial wellness and achieving one’s goals in life, whatever they are.

Prior to founding HSA Coach, Aaron was the CFO of HelloWallet, an online financial guidance application sold to employers as part of a financial wellness program. Morningstar (NASDAQ: MORN) purchased HelloWallet in 2014. Prior to joining HelloWallet, Aaron was the head of financial planning and Analysis (FP&A) at General Motors (NYSE: GM), and before coming to GM Aaron was an investor at the Carlyle Group (NASDAQ: CG).

Are you looking for a retirement speaker for your next conference, consumer event or internal professional development program? Visit the Retirement Speakers Bureau to find leading retirement industry speakers, authors, trainers and professional development experts who can address your audience’s needs and budget.

©2017, Roy Ranthun, MPH, “Mr. HSA” and Aaron Benway, CFP®, MBA. All rights reserved. Used with permission.