What is the Primary Insurance Amount (PIA) Formula?

Many of you may already know from your studies or reading that the PIA is the benefit that someone would receive at their full retirement age. On the Social Security statement are three different projected benefit estimates. One is at age 62 because that is the earliest age to claim a retirement benefit. The full retirement age benefit, which can differ depending upon the year of birth, can be anywhere between ages 66 and 67. It is the primary insurance amount and is 100 percent of the earned benefit. The benefit is based on a formula, and it is based on a process of steps.

First, Social Security looks at all years up to the age of 59 with Social Security covered earnings, and they index those earnings to today’s dollars. (Note: A client might have earnings that are not Social Security covered. Think about teacher, police, or fire retirement systems; in particular states that do not pay into Social Security. They have an equivalent system outside of Social Security that they pay into for retirement.) Why do they do that? Earnings from 1977 will not look nearly as wonderful as today’s earnings, so they index those through age 59. The earnings that someone earns at age 60 or beyond are taken at face value.

Step number two is to calculate your primary insurance amount based on your highest 35 years of index-adjusted earnings. If someone has less than 35 years of earnings, Social Security does not say, “Well, you have 20 years. Okay, that is what we will base the formula on.” They take those 20 years of indexed earnings and add 15 big fat zeros to the calculation. Suppose you talk to a client who wants to boost their primary insurance amount, and they don’t have 35 years of covered earnings. In that case, any additional year that they can earn something – even part-time work – and replace a zero will positively impact their PIA more than someone who has 35 years already and continues to work.

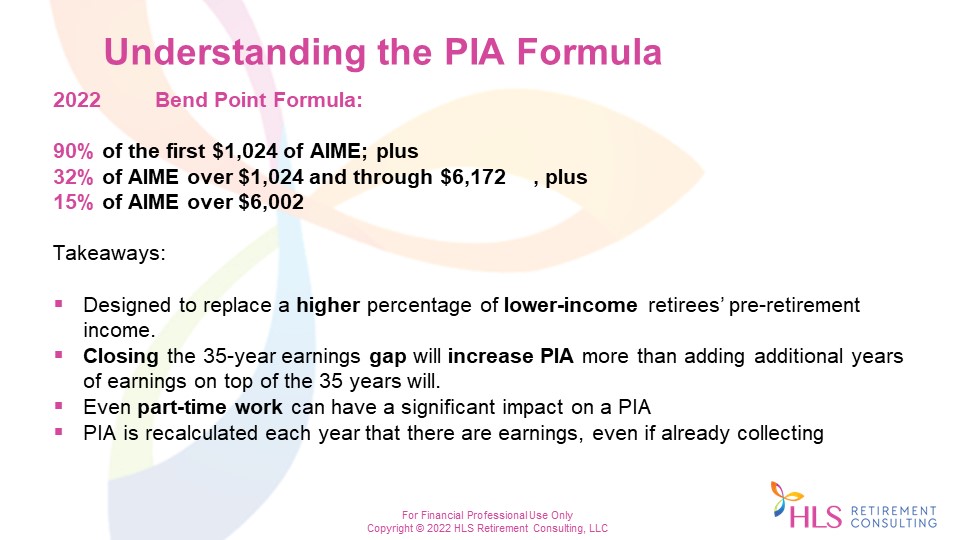

Step number three is after we have identified those 35 highest indexed years, you need to add that together, divide by 240, which is the number of months in 35 years. That is called the “average indexed monthly earnings” or AIME. Once we have done that, you apply that to the three-part bend point formula to calculate one’s Social Security benefit. The point of this example is to show you how that benefit formula is calculated with higher AIMEs.

You will see that 90% of the first $1,024 of AIME is replaced for someone turning 62 this year. The income replacement goes down to 32 percent for the second tier and is reduced to 15 percent in the third tier, or bend point. Why is this important to know? You have heard that Social Security is not designed to replace all our pre-retirement income; it is designed to replace, on average, 40 percent. You will see that the lower someone’s AIME is, the higher their replacement ratio is. Social Security is designed to replace a higher amount percentage-wise of a lower-earning person’s income. This is important to understanding the bend point formula.

Closing the 35-year earnings gap will increase PIA more than adding additional years of earnings on top of the 35-years that someone already has. Some conversations need to be had about continuing to work. I do not care if someone already has 40 years of earnings. Anytime someone can report earnings, PIA is automatically recalculated, even if they already receive their benefit. Suppose someone filed for benefits at age 64 and continued to work in a second career. Social Security will recalculate that PIA formula if that most recent year of earnings replaces an earlier year in the 35, which had lower earnings. Then they could see an uptick in their benefit amount going forward the following January, along with the cost-of-living adjustment.

Going back to the bend point formula, be aware of dealing with someone who has non-covered earnings. Say you have a teacher, a civil service retirement system employee, or a federal employee. There Social Security statement will show zeros in the Social Security earnings column, but it will have income in the Medicare column. That tells you that they have non-covered income. When Social Security calculates their PIA, it will appear as though they are a low-wage earner because they have a bunch of zeros in that 35-year formula.

We have something called the Windfall Elimination Provision (WEP) that offsets or adjusts their PIA, or the amount they can collect from Social Security, to reflect that they are not lower-wage earners, but they worked in an alternate system. I am sure you have worked with teachers that say, “Wait a minute. I worked enough under Social Security to collect a benefit. My benefit estimate says I will get $1,000 a month from that work. I am getting this pension of $3,000 based on earnings. Why am I not getting my full $1,000 from Social Security?” They appear in the PIA formula to be a low-wage earner with 35 years in the alternate system reflecting zeros in earnings. Their AIME is going to be small. Their Social Security statement will show their income being replaced at 90 percent in that first tier, and it really should not.

The WEP reduces that first tier to as low as 40 percent, depending upon how many years of substantial earnings they have under Social Security. These workers are not being cheated per se; it is an equalization of benefits for working in an alternate system.

It is important to understand this if someone says, “Gosh. Is it worth it for me to work part-time?” especially if they have less than 35 years. Again, even part-time work replaces zeros, and it will increase their primary insurance amount. Again, the PIA is recalculated each year there are earnings, even if someone is already collecting. We tend to have our highest years later in our careers. Even though our earlier career earnings will be indexed, our most recent years could increase the PIA. The claimant could experience an increase, in addition to the cost-of-living adjustment, the following January.

Deemed Filing

Anyone born after January 1st, 1954, cannot select which benefit to take between a spouse, ex-spousal, or retirement benefit. They are going to get the highest benefit to which they are entitled. If we have a low or non-earning spouse, they are still entitled to a spousal benefit once the wage earner files. They will get the higher of the two.

If there is any retirement benefit that this person has earned, that will always be paid first. Always. If there is a residual amount to be had by way of the spousal benefit, it is added on top of the earner’s benefit to make up the difference for that higher benefit. What is the downside? I will only collect a spousal or ex-spousal benefit if it is greater than my own if I fall into this deemed filing category.

For example, suppose my benefit is roughly $1,600 a month based on my earnings at full retirement age. In that case, the chances are unlikely that I will get a spousal benefit because the maximum benefit at full retirement age for a worker who worked at the highest taxable wage base every year right now is $3,345 in 2022. Half of that for a spousal benefit is $1,650 and some change. If you are working with someone who says, “Well, my benefit is $1,700, $1,800, or $2,000,” they will not get a spousal benefit or ex-spousal benefit.

What if their benefit is $1,000 at full retirement age and their spouse has a $3,000 PIA? When they file at full retirement age, they will collect the $1,000 under their record, and they are going to get a step up to the higher $1,500 (one-half of the spouse’s benefit) by getting an additional $500 of that spousal benefit. Remember that the wage earner must file for their benefit for the benefit to be paid as a spouse. That means that entitlement may not always be simultaneous. For example, if I want to file now, but my higher wage-earning spouse does not want to file until later, I can file for mine, but I will not get the spousal benefit until he files. It is not always simultaneous.

Let’s suppose I file for my benefit at age 62. Fast forward five years from now, and my spouse has filed. I will not get the full 50 percent spousal benefit because I initially filed for my benefit at age 62. It is a bit more complex than that, but many advisors think, “Well, now they are at full retirement age, so they should step up to the full 50 percent.” They would not get the entire 50 percent if they filed for their benefit early.

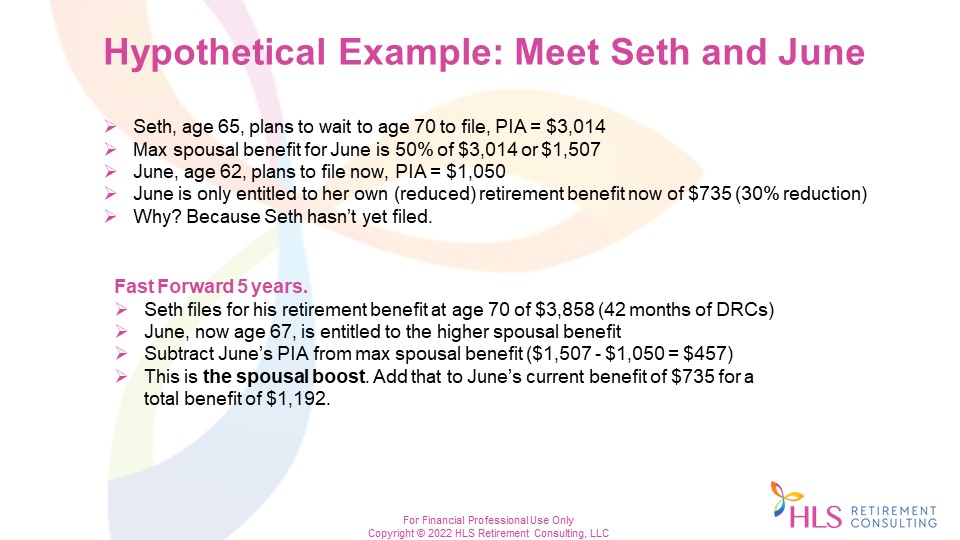

Let’s look at Seth, who is age 65. He plans to wait until age 70 to file, which is a wise decision because, as you can see, his primary insurance amount is high at $3,014. We know that the max spousal benefit for his wife, June, is $1,507 a month (50 percent of $3,104) if she waits until her full retirement age to collect it. June is age 62. She plans to file now, and her PIA is $1,050 at full retirement age so she will be claiming her benefit early. Remember that Seth has not filed yet, so she is only entitled to her benefit right now. So, she says, “Okay, I will take mine now with a 30 percent reduction because my full retirement age is 67.” Instead of June getting $1,050 a month, she will get $735. Remember, she is not entitled to Seth’s yet because he has not yet filed.

Fast forward five years. Seth is now 70. He has decided to file for his benefit. It was a very good choice for him because by waiting, he earned 42 months of delayed retirement credits, and his benefit is now $3,858 (this was with no COLAs). Now June is age 67. She is now entitled to the higher spousal benefit because the moment he files, she contacts Social Security. She should say, “I need my benefit reexamined because I am entitled to a higher benefit.” To figure out how much of the maximum $1,507 spousal benefit (one-half of Seth’s benefit at his full retirement age) she will collect, you first have to figure out the difference between the maximum spousal benefit and her benefit at full retirement age. So, the $1,507 maximum spousal benefit minus her maximum worker benefit of $1,050 at her full retirement age is $457. This is called the spousal excess amount or the spousal boost. That is the amount added to her current monthly benefit of $735. She can receive $1,192 in benefits per month by adding these two together.

This is one thing that I get more questions about and more flubs in what people tell their clients. It’s not, “Well, you are age 67 now, and you will automatically step up to the full 50 percent.” The critical thing they miss is that her spousal benefit will not equal half her spouse’s benefits because she claimed her benefit early. That spousal boost will be added to her already reduced retirement benefit. This is important to know when you are talking to clients.

What is My Breakeven?

It is the age-old question: what is my breakeven age? It is understandable why people want to know, “How long do I have to live to make sense for me to hold out for a bigger benefit?” This becomes an issue in particular for married couples.

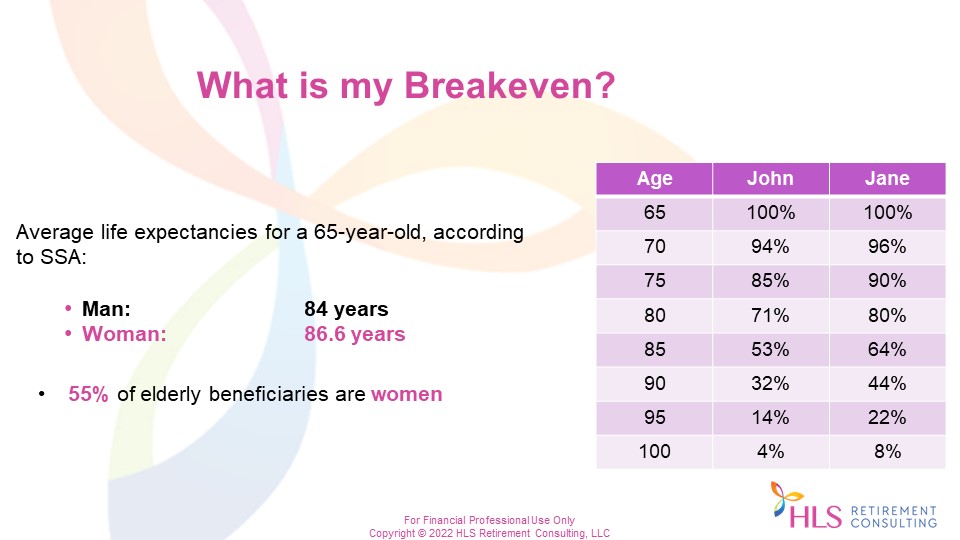

According to Social Security, the average life expectancy for a 65-year-old male is age 84, and for women, it’s almost age 87. We have brand new life expectancy tables for required minimum distributions (RMDs) that start this year that reflect we have had increasing longevity for a while. Fifty-five percent of elderly beneficiaries are women and no surprise that three out of four women are widowed by the time they are 75.

Breakeven is an easier conversation to have when dealing with a single person because the only person they are trying to make income last for is themselves. But when you are dealing with a couple, particularly when you have a marked disparity in their income benefits, it is a question that needs a little bit more consideration.

The information above is from a website called longevityillustrator.org. The example shows life expectancies for John and Jane, both born on the same day, in average health, and both are non-smokers. The chart shows the likelihood of them living to an advanced age. There is a 44 percent chance that Jane will live to age 90, and John has a 32 percent chance. It is important to look beyond average longevity when dealing with the couple as a unit. It changes the conversation. You must make sure that the decision they make for claiming is the best decision for both of them.

We all tend to underestimate how long we will live, and the amount of time we will spend in retirement, proven by numerous studies. The reality is that longevity is increasing, and life expectancy is increasing. Women tend to suffer financially after their spouse dies. And they rely more heavily on Social Security for a variety of reasons. They are less likely to have access to a pension. They may have left the workplace or never worked outside the home to help raise a family. They might be helping take care of a parent. We tend to take those roles on more than our male counterparts. We have less in savings and retirements savings. We have a lower primary insurance amount.

This is why it is important to think about the breakeven analysis in terms of the couple, particularly if we are dealing with a couple with a lower benefit than the other. When one spouse is the high-wage earner, when that person files, it is the gift that can keep on giving or not. When I am looking at a case and seeing a marked disparity in benefits, I home in on that. I am saying, “Okay, higher wage earner, we need to focus on when you file because when you file, it will affect not only lifetime income while you are both living and enjoying life, but it will affect the survivor. Whether that is you, or whether that is your spouse.”

Consumers do not fully understand what happens when one of the spouses dies concerning Social Security. They do not understand that the lower of the two benefits disappear. We are dealing with a reduction in income. The difference between the higher wage earner filing at age 62 versus even full retirement age can significantly impact that surviving spouse’s income. People ask me all the time for a rule of thumb. I run from the rule of thumbs, particularly with respect to this, because so much goes into what is the right decision for individuals and couples. However, when working with a couple with an income disparity, I do not mind allowing that person to file early because they are the lower-wage earner. If I can talk to the higher wage earner and ask, “Is there any way that we could have you hold out a little bit longer so that we can secure a higher replacement income from Social Security, so we put less of a burden on your other assets while you are both living? This is then some insurance for the surviving spouse to have a higher replacement ratio of income when one of the two of you passes.”

This is really my only rule of thumb. I disagree that everyone should file at age 62 because it will all go defunct or that everyone should file at age 70, and that is just not reality. You are there to have thoughtful conversations about how much they have saved for retirement, their goals, and what they want to do in retirement. Those are all things that do go into this claiming decision.

Working and Claiming a Benefit

What if someone wants to claim their benefit early and still work? Social Security limits how much someone can earn while collecting benefits. I get questions like, “Does my IRA distribution count?” No. It is not earned income. If you are working with someone who plans to file early for Social Security and they are working, then there is a chance that their benefits could be withheld, or they may not even be able to file for benefits. Suppose someone is between age 62 and the year before they hit their full retirement age in 2022, and they earn more than $19,560 while receiving Social Security benefits. In that case, excess income over that amount will cause their benefits to be withheld by 50 percent of that excess. The earnings limit only applies until a claimant reaches FRA. I believe in getting people to their full retirement age so they do not have to worry about having benefits withheld and possibly not paying taxes on their benefits.

What does not count as earnings? Unemployment compensation does not count. Pension income does not count. These are all passive sources. Rental property income. IRA distributions. Alimony for settlements entered into after 2018. Or a spouse’s earnings. If they say, “Well, I am retiring, but my spouse is still working. I am the one that wants to claim early.” Technically, they can claim early. Should they? That is another conversation because they are likely to pay taxes on a portion of their benefit because of their spouse’s earnings.

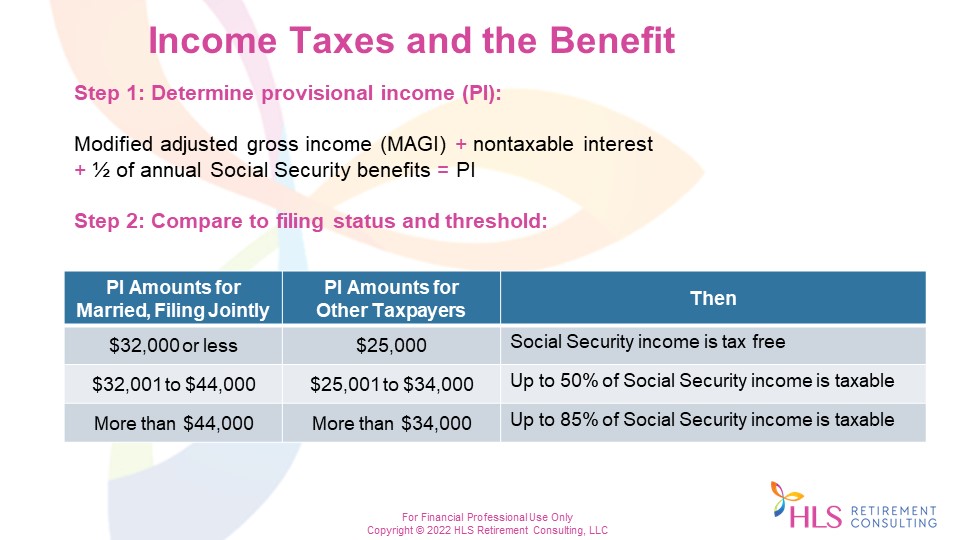

Let’s look at income taxes and the benefit. There is a two-step process to determine whether any benefits are subject to tax. The first step is determining provisional income (PI), sometimes called combined income. It is a function of three things:

- Modified adjusted gross income (modified just simply means we are not including Social Security in the income because we are not going to include it twice), plus

- Non-taxable interest, such as municipal bond interest that we know is federally income tax-free, plus

- Half of the annual Social Security benefits received.

Unlike the earnings limits that only look at the filer’s earnings, potential taxation of Social Security benefits also looks at the earnings and the benefits of the household. Say two spouses are collecting benefits.

- Total their annual benefits and divide by two to determine their provisional income.

- Compare that number to their filing status and threshold. (These taxes were added in the 1983 Act for Social Security, and they have never changed.)

They might pay taxes on up to 85 percent of their Social Security benefits.

If a married couple has a provisional income of $32,000 or less, they do not have to worry. These folks are living probably squarely on Social Security and not much more. If they are anywhere between $32,000 to $44,000, 50 percent of their benefits must be pulled in as a line item to be federally taxed. If their provisional income is over $44,000, then as much as 85 percent can be taxed.

Pensions are considered taxable income. Which sources of income could they have that would not hit the bottom line? Qualified Roth distributions are a good one. We should be talking about Roth conversions before we claim Social Security. Income from permanent life insurance is not included in this calculation.

What are some common points of confusion concerning taxes? The earnings limit and taxation of benefits are two separate sets of rules. I get many questions about the earnings limit and taxes, and they seem to get interchanged. The earnings of a spouse and all other sources of income are included in determining whether the benefit or a portion of it is subject to taxes, whereas, if we compare this to the earnings test, it is only earned income and only that of the early filer. For taxes, everything is fair game. All sources of taxable income are included, not just earned income. The potential for taxes to apply to a benefit does not disappear at full retirement age as the earnings limit does. You must be aware of municipal bond interest if you work with folks with this in their portfolio, as it has to be included in calculating taxation on Social Security benefits.

Survivor Benefits

Age 62 is a critical age. It is the earliest age at which someone can collect a Social Security retirement benefit. That is also the earliest age when someone, a spouse or ex-spouse, can collect a spousal benefit. For survivor benefits, it is a little bit different. The earliest age that a widow or widower can claim a survivor benefit is generally age 60 or older. It could be as early as age 50 if the survivor were disabled within seven years of the death of their spouse. Another way a survivor might receive benefits before age 60 is for a child-in-care benefit. If the survivor has a child-in-care of the deceased under age 16, they might get a child-in-care benefit until the oldest child turns 16. Or they might get a child-in-care benefit if they are caring for a child of the deceased that was disabled before the age of 22.

You must be married for at least nine months to collect an aged widow or widower benefit at age 60. You will need to be married for one year to file for spousal benefits for someone still living. Ex-spousal survivors can also collect a benefit if they were married for at least ten years. If you remarry while your former spouse is living while collecting ex-spousal benefits, those benefits stop. But in the case of ex-spousal survivor benefits or even aged widow or widower benefits, an ex-spouse survivor can remarry at age 60 or later and still collect a survivor benefit as long as they were married for more than ten years. A widow married for at least nine months when their spouse dies can remarry at age 60 or later and still collect a survivor benefit. What? People miss this. By not remarrying until age 60 or later, that (ex-)spouse down the road will still be able to collect that widow or widower’s benefit.

How much can they collect? With spousal and ex-spousal benefits while that other spouse is living, it is a maximum of 50 percent of the worker’s primary insurance amount. When we are dealing with survivor benefits, it goes up to a maximum of 100 percent of what the deceased spouse was collecting at the time of their death or entitled to collect at their death. Let’s suppose we have a person aged 60 or even age 62 that passes before they ever collect it. That means their survivor base amount is calculated as if they had reached their full retirement age when they died. That is a common question. In other words, the widow or widower is not penalized because the deceased had not yet collected; that survivor benefit is calculated as if the deceased had reached full retirement age.

What if they plan to file at age 70 and die early at age 68? This also benefits the survivor. The base amount is calculated as if they died and claimed on the day of death. The two-year delayed retirement credits are passed on to the survivor’s base amount. Note that there is a maximum of 100 percent of the deceased’s benefit. Like any other Social Security benefit collected early, the aged widow or widower benefits are reduced based upon the number of months they file early. They can file at age 60, but they will not get 100 percent of the benefit.

The child-in-care benefit could be at any age for a surviving spouse taking care of the dependents of the deceased. That benefit maximum is 75 percent and not reduced unless the family maximum reduces it. Only the aged widow or widower benefits are reduced. There is also a whopping $255 lump-sum death benefit paid to the surviving spouse. It would be paid automatically only if the spouse was already collecting spousal benefits under that person. If they were not, the surviving spouse would have to file form SSA-8 to get those benefits. I know it is not a lot, but people miss it because they don’t file for it.

What is an effective technique that everyone misses? I call it the survivor switch technique. If someone is entitled to both a survivor benefit and their own retirement benefit, they can restrict their filing to one or the other. Now, restricted filing where both spouses are alive or the ex-spouse is alive can only be used for people born before January 1st, 1954. This does not apply to survivor benefits, and people miss it every day. If you are entitled to both a survivor benefit and your own retirement benefit, you need to figure out which benefit will be the higher of the two in the long run. First, file for the smaller benefit and later switch to the higher benefit to give me the highest lifelong income benefit for the rest of my life.

In terms of restricting from one to the other, survivor benefits are not subject to that same January 1st, 1954, birthdate requirement. That only applies to living spouses and ex-spouses. This is singly one of the most often overlooked opportunities that I help people with every day. Be aware. Social Security might assume that because the survivor benefit will be higher, you will file for all of them simultaneously. You will lose the opportunity to file for the smaller one first and hold out of the higher one later because they are not told you can do so.

Let’s look at an example. Janet turned 66 last July, and her husband passed recently. He was collecting $2,100 a month at the time of his death. This is the survivor base amount. Susan has not yet filed for her benefits. Her estimated benefit at her full retirement age is $1,800. What are her options? If she contacts Social Security, they might say, “The $2,100 is higher, so just go ahead and file for that.” Technically, this is a deemed filing. They assume, “Let us just put all of your tickets in the hat for both retirement and survivor income. We will pay the $1,800 for your benefit, and then we will pay you that survivor boost of $300 to bring you to the higher total of $2,100.” That makes sense, and Janet probably would not question that, would she?

The second option would be, “Okay, wait a minute. I know that there is something I can do here. I am going to restrict my filing to survivor benefits now. And I will wait until age 70 to file for my own.” Why would I do that? Janet could collect $2,100 now as she is now at full retirement age for 100 percent of that survivor base amount. She will hold out to file for her own benefit because, at that point, that $1,800 has become $2,352 because she has earned 46 months of delayed retirement credits by waiting. This is the difference and what people are not told when they contact Social Security. Social Security is expressly prohibited from giving anything that looks like advice, so they will not be told this. This is where you can look like a hero and help them leverage income. It works both ways.

What if survivor benefit is going to be higher forever? There is no way that at age 70, her own retirement benefit will be higher. In this case, she would take the $2,100 and go for the rest of her life because her own benefit would not be higher. However, let us suppose she is 62, and her own reduced benefit is $1,000 a month. She might then want to file for her reduced retirement benefit and hold out until full retirement age, so she gets 100 percent of that survivor benefit. This strategy can work either way. Advisors need to be very mindful of this when working with widows and widowers.

Here are some things to remember. Survivor benefits, just like any other benefit claimed before full retirement age, are subject to the annual earnings test. There might be situations where Social Security says you make too much money, come back when you do not or when you hit full retirement age, whichever occurs first. Suppose the survivor benefit is collected before the survivor’s full retirement age. In that case, it will be reduced based upon the number of months before FRA it is claimed, just like any other benefit. Social Security will generally not tell you this. I find, and there are some wonderful people at the Administration, that the old-timers are starting to retire. The new ones have come on during COVID, and they are challenged to even know that these techniques exist. Your clients have to file for benefits empowered with information to know that they can even do this.

How do you figure out which one to file for first? You want to compare the survivor benefit at the survivor’s full retirement age to the maximum of their own retirement benefit at age 70. Whichever one is higher, you file for the lower one first. Do not miss this. This is a tremendous opportunity for you to bring value to your clients.

Key Takeaways

- The decision on when to claim Social Security cannot be made without looking at a near retiree’s entire retirement income picture. This is where you have such value because for them to say, “When should I file?” Well, you know what, Mr. and Mrs. Smith, I need to know more about you. What other sources of income do you have? What type of income is that? How is it going to be taxed in retirement? Because we do need to think about the tax part of it. Who is going to work and until when? How much? Is there a chance you could go back and have an encore career? All these things come into it.

- The other things that come into it are very much the emotional part. “I have worked hard for this; I should be able to file. Is there a way we can do that?” Hopefully, we can get some of the Social Security income into the household by the lower wage earner and hold out for the higher one later. There is no one size fits all approach. We also deal with people, emotions, needs, and income needs. Using rules of thumb such as everyone should start at age 62 or wait until age 70 does not apply and takes away the value you provide.

- Be proactive by asking many questions to uncover opportunities to leverage more significant benefits. If there is a survivor situation or a wide disparity in ages, ask if they have any kids and how old are they. If the kids are under the age of 18 or still in high school and not older than age 19, the 65-year-old spouse filing can now open the opportunity to collect dependent benefits for those children.

- When working with married couples, special attention should always be given to the higher wage earners filing age when dealing with a marked disparity in income benefits. We want to focus on getting that higher wage earner to hopefully wait until full retirement age or longer if they have other sources of income or continue to work. This will build more income from Social Security while they live and leave the surviving spouse with more replacement income from Social Security survivor income.